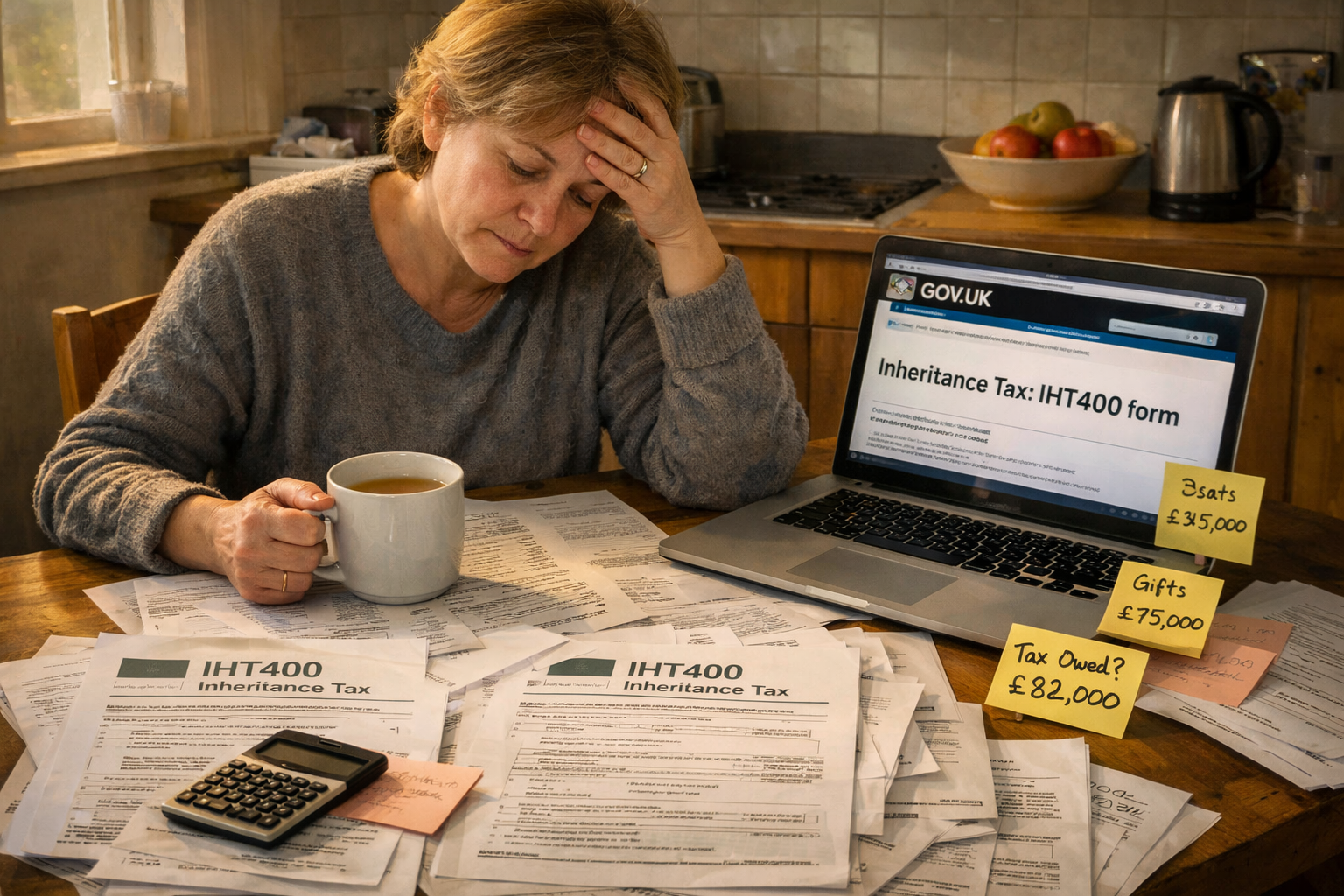

There’s a particular type of grief-tinged admin that nobody prepares you for. You’ve just lost someone — a parent, a spouse, a sibling — and within weeks you’re expected to navigate one of HMRC’s most demanding tax forms. The IHT400. Forty pages of questions about assets, debts, gifts made seven years ago, jointly owned property, and overseas holdings. And at some point, in the middle of all that, you find yourself asking a very reasonable question: can you submit IHT400 online?

It seems like it should have a simple answer. After all, we file self-assessment returns online. VAT submissions go through the Government Gateway. Even probate applications have moved partially digital. So why is the IHT400 still largely a paper exercise in 2026?

The answer is complicated — and it matters quite a lot if you’re an executor trying to get probate granted, or a family attempting to settle an estate without unnecessary delay.

What HMRC Actually Says About IHT400 Online Submission

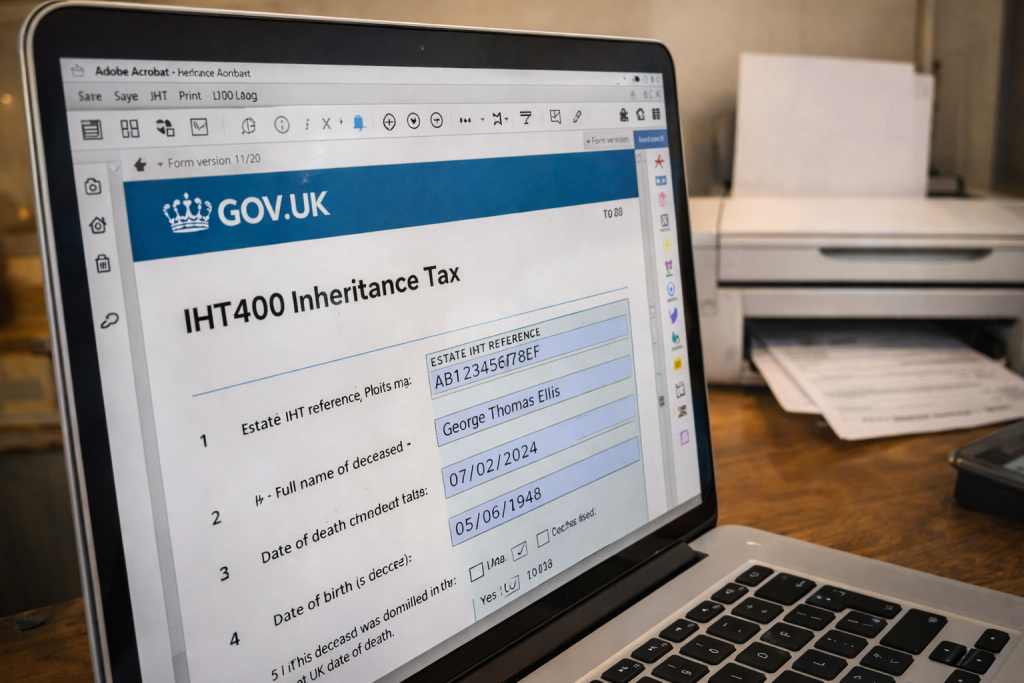

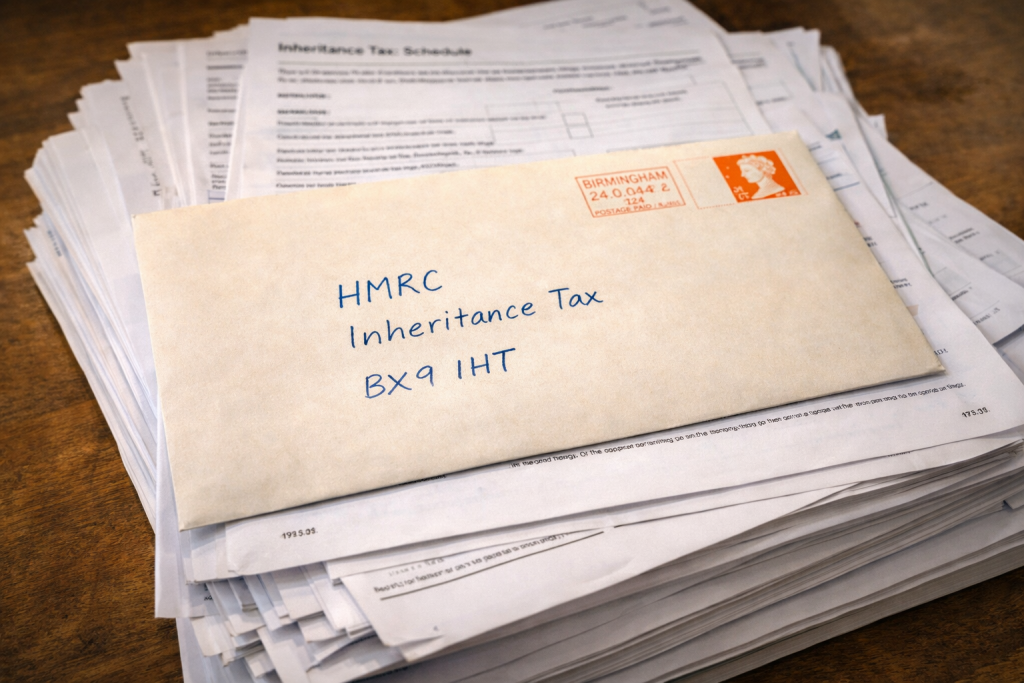

Let’s be direct: as of 2026, you cannot submit the IHT400 form fully online through HMRC’s standard portal. The form itself can be downloaded as a PDF from GOV.UK, and in some cases it can be completed digitally before printing — but the submission process still requires a physical, signed paper copy to be posted to HMRC’s Inheritance Tax office in Nottingham.

This is not a glitch. It is not an oversight that’s about to be patched in the next software update. HMRC has been deliberately cautious about moving the IHT400 to a fully digital process, partly because of the legal weight the form carries (it triggers formal IHT assessments), and partly because of the range of supplementary schedules — IHT401 through IHT430 — that must accompany the main form depending on the estate’s composition.

Can you submit IHT400 online in part? Technically, yes. If you’re instructing a solicitor or tax adviser who is registered with HMRC as an agent, they may have access to certain digital processes — but even then, the IHT400 itself is not submitted through HMRC Online Services in the way that, say, a corporation tax return would be.

⚠️ A note for anyone in a hurry: Don’t conflate the probate application (which can now be done online through HMCTS) with the IHT400 submission (which goes to a completely different government department). They are separate processes, submitted separately, to separate offices. Mixing them up causes delays that can run to months.

The Digital Workaround That Actually Helps

Just because you can’t submit IHT400 online doesn’t mean technology plays no role. Here’s where digital tools do genuinely help:

HMRC’s IHT400 PDF is what they call an “interactive PDF” — meaning you can type directly into the fields before printing. This is far preferable to handwriting, both for legibility and for your own sanity when you’re working out figures. You can save your progress, return to it, amend figures as valuations come in.

There’s also the matter of IHT online reference numbers. Before you can send a cheque or make a payment for any inheritance tax owed, you need to request a reference number — and that you can do online via GOV.UK. This part of the process has been digital for a while and works reasonably well.

Additionally, if the estate qualifies as “excepted” — meaning it falls below the threshold or meets specific criteria — executors may be able to use the IHT205 process instead (though note that IHT205 was replaced by IHT207/IHT217 changes in recent years; always check current GOV.UK guidance). Excepted estates have a simpler reporting process entirely.

For a full breakdown of the IHT400 form itself — what each section covers, what the supplementary schedules are for, and what information you’ll need to gather — the team at Ask Accountant has put together a complete IHT400 guide worth bookmarking.

Why Is This Form So Complicated, Anyway?

Honestly? Because estates are complicated.

The IHT400 isn’t asking needlessly nosy questions. It’s trying to capture the full taxable value of everything the deceased owned — which might include property held in trust, gifts made years before death, business assets qualifying for Business Relief, agricultural land, pension arrangements, foreign assets… the list goes on.

The inheritance tax rules in the UK layer multiple thresholds and reliefs on top of each other. There’s the nil rate band (£325,000 as of 2026), the residence nil rate band (up to £175,000 if a family home is passed to direct descendants), transferable allowances from a deceased spouse, and various exemptions for business and agricultural property. Getting these wrong — or simply failing to claim them — can cost a family tens of thousands of pounds.

The IHT400 forces executors to work through all of this methodically. It’s painful, but it’s thorough for a reason.

What the IHT400 Submission Process Actually Looks Like in 2026

For those going through this for the first time, here’s a realistic picture of the current process:

Step 1 – Value the estate. This means gathering figures for property (you’ll need a formal valuation), bank accounts, investments, business interests, and any gifts made in the seven years before death. This stage alone can take weeks.

Step 2 – Complete the IHT400. Work through the form carefully, including any relevant supplementary pages. The form asks for a lot of supporting documentation.

Step 3 – Calculate any IHT owed. If tax is due, you’ll need to arrange payment before probate is granted — which creates a chicken-and-egg problem, since you often need probate to access the estate’s assets. Banks and some investment platforms have processes to release funds specifically for this purpose.

Step 4 – Send the form. By post. To HMRC’s Inheritance Tax office. With supporting documents. Keep a copy of everything.

Step 5 – Wait. HMRC’s IHT400 processing times have been a source of genuine frustration for executors and their advisers. In normal circumstances, expect several weeks at minimum; during busy periods it can stretch considerably longer.

Step 6 – Apply for probate. Once HMRC has confirmed receipt and issued the relevant reference, you can proceed with the probate application. Again — this is separate from the IHT400 submission itself.

The Table You Actually Need: IHT400 vs Other IHT Forms

| Form | When to Use | Can Submit Online? | Notes |

|---|---|---|---|

| IHT400 | Estate above nil rate band or with complex assets | No — paper only | Main form; accompanied by relevant schedules |

| IHT205 | Excepted estates (older process — check current rules) | No — paper only | Largely superseded; confirm with GOV.UK |

| IHT400 Online Reference | To obtain reference number before paying IHT | Yes — via GOV.UK | Reference needed before making any payment |

| Probate Application | After IHT400 submitted and reference confirmed | Yes — HMCTS portal | Separate to IHT400; goes to HMCTS not HMRC |

| IHT100 | Reporting chargeable events on trusts | No | Different context — trust-related IHT reporting |

Common IHT400 Mistakes That Cause Rejections and Delays

Because this is paper-based and manually reviewed, errors have real consequences. HMRC will return incomplete or inconsistent forms — and that can add weeks to the probate timeline.

The most frequently seen problems (in no particular order of frustration):

- Missing supplementary schedules. If the estate includes stocks and shares, you need IHT411. Foreign assets? IHT417. Business interests? IHT413. Each schedule must accompany the main form.

- Unsigned declarations. The form requires signatures from all executors. If there are three executors and one hasn’t signed, back it comes.

- Inconsistent asset values. Figures on the main IHT400 should tally with the totals on relevant schedules. Discrepancies flag the form for review.

- Gifts omitted or undervalued. The seven-year rule means gifts made before death must be declared. Executors sometimes don’t know about all of them — which is exactly why understanding inheritance tax gifts rules in advance matters so much.

- Claiming the residence nil rate band incorrectly. The conditions for this additional threshold are specific — the property must pass to a direct descendant, and the estate value must fall below the taper threshold. It’s one of the key IHT allowances people underuse and occasionally misapply.

Will IHT400 Ever Move Online? What’s Actually Happening

There has been genuine movement in this direction. HMRC has been working — slowly — on digitising more of the inheritance tax process. The shift in excepted estate reporting (which moved away from requiring a full IHT205 in many cases) was part of broader reform. And there are periodic mentions in HMRC’s roadmap documents of a more digital IHT process coming.

But “coming” is doing a lot of heavy lifting in that sentence.

The complexity of the IHT400 — with its twenty-odd potential supplementary schedules, each covering different asset types — makes a clean digital solution genuinely difficult to build. Self-assessment is relatively formulaic by comparison. The IHT400 deals with valuations, legal ownership structures, trust arrangements, and international assets in ways that resist simple digitisation.

For now, the honest answer to “can you submit IHT400 online” remains: not fully. Not in the way you’re probably hoping for.

When It’s Worth Getting Professional Help

There’s a threshold of complexity with IHT400 submissions where DIY stops being a sensible choice. Not because the form is impenetrable — it isn’t — but because the stakes are high enough that mistakes are expensive, and the process is time-consuming enough that professional help genuinely saves more than it costs.

Broadly speaking, you should consider professional support when:

- The estate includes business or agricultural assets (reliefs are available but conditions are strict)

- Property was jointly owned with someone who isn’t the sole beneficiary

- The deceased made significant gifts in the seven years before death

- There are overseas assets of any meaningful value

- The estate is subject to a trust

- There’s any uncertainty about which assets fall within the estate for IHT purposes

Ask Accountant, based at 178 Merton High St, London SW19 1AY, handles inheritance tax submissions as part of their broader tax advisory work — including the full IHT400 process, supplementary schedules, and ongoing estate planning support. They also cover the kind of proactive tax planning that can reduce IHT exposure while there’s still time to act. Reachable at +44(0)20 8543 1991, they’re the kind of firm worth speaking to before you’re knee-deep in probate rather than after.

A Rough Timeline Comparison: DIY vs Professional IHT400

| Stage | DIY Estimate | With Professional Support |

|---|---|---|

| Gather estate valuations | 4–8 weeks | 3–6 weeks (adviser coordinates) |

| Complete IHT400 + schedules | 2–4 weeks (unfamiliar) | 3–7 days (experienced) |

| HMRC processing | 6–20 weeks | 6–20 weeks (same — out of everyone’s hands) |

| Risk of rejection/resubmission | Higher — adds 4–8 weeks | Lower — rare with experienced adviser |

| IHT relief claims maximised | Possibly missed | Systematically checked |

(Note: HMRC processing times fluctuate significantly — the above is indicative only)

Understanding the IHT400 Threshold Question

One thing that trips people up: not every estate that exceeds the nil rate band automatically requires an IHT400. The decision tree is slightly more nuanced.

You generally need to complete the IHT400 when:

- The gross estate value exceeds the applicable nil rate band threshold (including any transferred threshold from a deceased spouse)

- The deceased made chargeable gifts in excess of £250,000 in the seven years before death

- The estate includes assets that qualify for conditional relief (business property, agricultural property, heritage assets)

- You’re applying for probate and the estate is not an excepted estate under current HMRC rules

Understanding inheritance tax thresholds properly — including how the residence nil rate band interacts with larger estates (it tapers above £2 million) — is genuinely worth doing before you decide which process applies.

The Bigger Picture: Planning Before the IHT400 Becomes Necessary

Here’s something worth saying plainly: the IHT400 is a form you complete after someone has died. By that point, the tax liability is largely fixed. The time to reduce it was earlier — through lifetime gifts, trusts, insurance arrangements, and careful planning around business assets.

The seven-year rule on gifts, for instance, means that assets transferred more than seven years before death fall outside the estate entirely. Pension funds (under current rules, subject to proposed changes) have historically sat outside the estate. Charitable gifts are exempt. Business Property Relief can shelter trading business interests entirely.

None of this is secret. It’s not aggressive avoidance. But it requires thinking ahead — and that’s where working with advisers who provide proactive inheritance tax planning makes the most tangible difference.

By the time you’re filling in the IHT400, the planning window has closed. Which is a slightly uncomfortable thing to read if you’re currently filling in an IHT400 — but it’s worth knowing for the next generation, and for any estate planning conversations you’re having right now.

Frequently Asked Questions

Can you submit IHT400 online in 2026? No — not as a full digital submission. The IHT400 must be completed and posted to HMRC’s Inheritance Tax office. The interactive PDF can be filled in digitally before printing, and you can request an IHT payment reference online, but the form itself requires physical submission with original signatures.

How long does HMRC take to process an IHT400? Processing times vary significantly. In straightforward cases you might receive confirmation within a few weeks; in busier periods or where HMRC has queries, it can take considerably longer. See HMRC IHT400 processing times for a more detailed breakdown.

Do I need to complete the IHT400 before applying for probate? Yes. You must send the IHT400 to HMRC and receive confirmation before you can obtain the grant of probate. The two processes are related but go to different government bodies — HMRC for the IHT form, HMCTS for the probate application.

What happens if I make a mistake on the IHT400? HMRC will return the form if there are errors, missing signatures, or missing schedules — which delays the whole process. If an error is discovered after submission, you’ll need to contact HMRC directly to amend the return. Significant undervaluations can attract penalties.

Is there a way to submit IHT400 digitally if I use a tax adviser? Not in the same way that agents can submit self-assessment or company tax returns online. Agents can assist with the completion and may handle postal submission on your behalf, but there is no dedicated agent portal for IHT400 digital submission as of 2026.

What is the IHT400 deadline? The IHT400 must be submitted within 12 months of the end of the month in which the person died. However, any inheritance tax owed is due within 6 months — meaning you may need to pay before the full form is submitted, using the estimated values. Late payment attracts interest.