If you run a limited company and you’re trying to figure out how to reduce corporation tax legally in 2026, you’re asking exactly the right question at exactly the right time. Corporation tax sits at 25% for companies earning above £250,000 — a significant jump from the flat 19% most directors had grown quietly used to over the previous decade. That’s a quarter of your profits handed over before you pay yourself, reinvest, or do anything remotely interesting with the money your business has earned.

The distinction that matters here is between tax avoidance (aggressive, legally questionable, and frequently front-page news) and tax planning — which is entirely legitimate, widely practised by well-advised businesses, and very much what this article is about. There are proper, HMRC-sanctioned ways to legally reduce corporation tax, and most UK limited companies aren’t using all of them.

This guide covers the most effective strategies available in 2026. Some will apply to you right now. Others depend on your structure, your sector, or whether your accountant has ever actually sat down with you before your year-end to discuss options.

Understanding Your Rate Before You Try to Reduce Corporation Tax

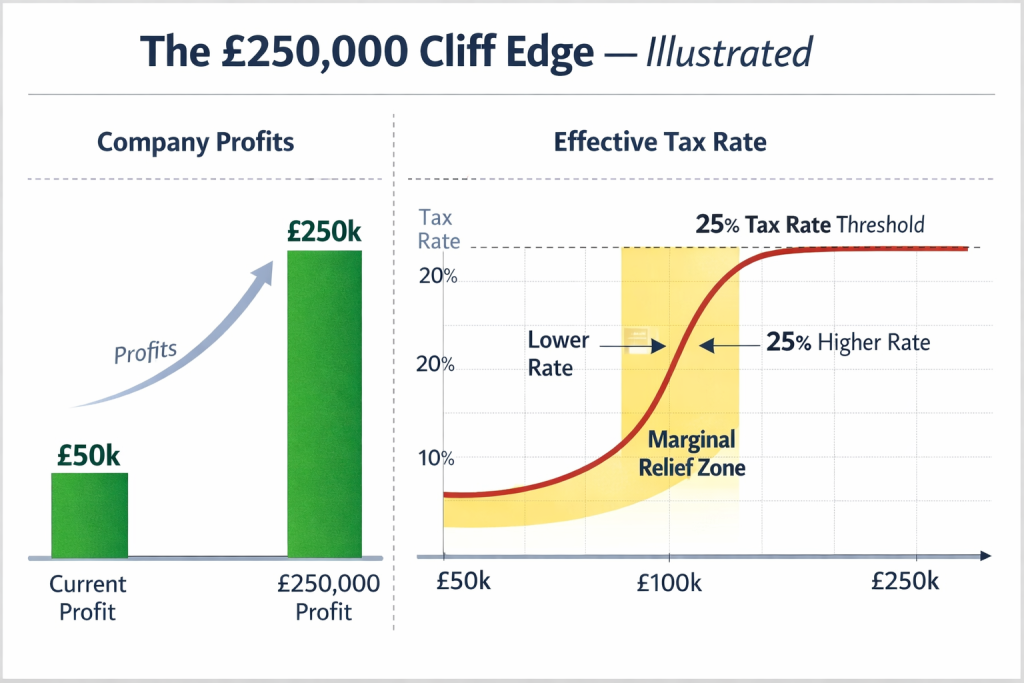

Before working out how to reduce corporation tax legally, it helps to know exactly which rate you’re on — because a surprisingly large number of directors don’t.

| Profit Level | Corporation Tax Rate (2026) | Notes |

|---|---|---|

| Up to £50,000 | 19% | Small profits rate |

| £50,001 – £250,000 | 19%–25% (marginal) | Marginal Relief applies — effective rate sits somewhere between the two |

| Above £250,000 | 25% | Main rate — applies to all profits |

| Ring fence profits (oil & gas) | 30% | Separate rules apply entirely |

Note: These thresholds are divided equally between associated companies. Own two companies? Each threshold is halved. Worth checking with a specialist if that applies to you.

One thing many directors miss: marginal relief is a sliding scale, not a cliff edge. A few thousand pounds in extra deductions can meaningfully shift your effective rate. That’s precisely why year-round planning delivers far more than a last-minute scramble.

R&D Tax Credits — A Legal Way to Reduce Corporation Tax Many Companies Overlook

Let’s start with the one that genuinely surprises people. Research and Development tax relief rewards companies doing something innovative — and HMRC’s definition of “innovative” is considerably broader than most directors realise.

You don’t need to be inventing fusion reactors. If your business has spent time and money developing new software, improving a manufacturing process, solving a technical problem that wasn’t readily solvable, or creating something that simply didn’t exist before — there’s a reasonable chance you qualify.

Under the current merged R&D scheme (reformed April 2024), most companies can claim a 20% RDEC credit on qualifying expenditure, applied against their tax liability. Loss-making companies and R&D-intensive SMEs may qualify for a higher rate under the Enhanced Support rules.

⚠️ One important caveat: HMRC has significantly tightened R&D compliance. Claims need to be detailed, technically justified, and properly documented. Submitting a vague or inflated claim is no longer something you can quietly hope goes unnoticed. If you’ve never explored this, or you’ve been using a claims company charging chunky commission fees, getting a second opinion is sensible. The team at Ask Accountants UK Ltd has handled R&D claims across multiple sectors and can assess whether your activity genuinely qualifies.

Capital Allowances: Legally Reduce Corporation Tax Through Smart Asset Purchasing

Here’s where a lot of smaller companies leave money on the table. When your business buys physical assets — computers, vehicles, machinery, office fit-outs — you can’t always deduct the full cost through your profit and loss account immediately. But through the Annual Investment Allowance (AIA), you can often write off 100% of qualifying expenditure in the year of purchase.

The AIA limit is currently £1 million per year — covering the vast majority of SME capital spending. That’s a substantial deduction available before you’ve even looked at other reliefs.

Beyond the AIA:

- Full Expensing — made permanent from November 2023, allowing 100% first-year deductions for most new plant and machinery

- 50% First Year Allowance for special rate assets (long-life assets, certain fixtures)

- Enhanced Capital Allowances for qualifying energy-efficient and water-efficient technology

Timing matters considerably. Buying £40,000 of equipment just before your accounting year-end rather than just after can bring forward a £10,000 tax saving by a full twelve months. Multiply that across several assets over several years, and it compounds into something meaningful.

External reference: HMRC Capital Allowances guidance covers categories and current rules in full.

Salary vs Dividends — How Director Remuneration Helps Legally Reduce Corporation Tax

This is probably the most discussed aspect of tax planning for owner-managed businesses, and it’s still widely misunderstood.

Directors of limited companies typically pay themselves a combination of salary and dividends. Salary attracts Income Tax and National Insurance (both employee and employer). Dividends attract only Dividend Tax — at lower rates than income tax. The gap between these two rates is precisely where directors can reduce their overall tax burden.

The standard structure in 2026:

- Salary set at the NI Secondary Threshold (£9,100 per year) — keeping NICs to zero whilst preserving state pension entitlement

- Additional pay via dividends — taxed at 8.75% (basic rate), 33.75% (higher rate), or 39.35% (additional rate)

💡 Worth knowing: The dividend allowance dropped to just £500 from April 2024. The days of drawing £2,000 tax-free in dividends are behind us. But the combined burden of salary plus dividends still runs lower than salary alone for most director-shareholders.

If you have multiple shareholders or family members holding shares, this gets more complex quickly. The settlements legislation rules around dividend-sprinkling are genuinely nuanced — this is an area where proper personal tax planning advice pays for itself fairly quickly.

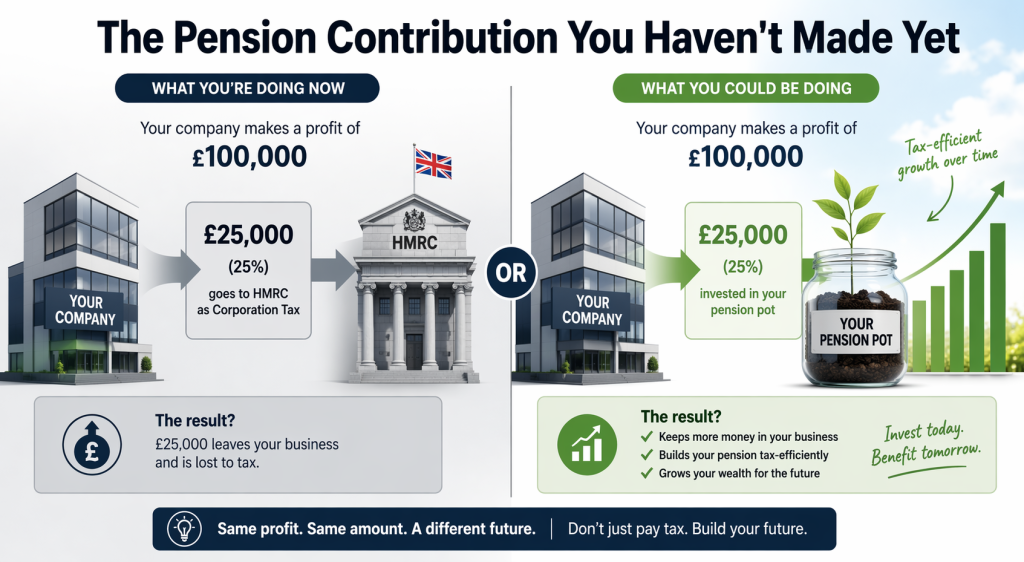

Pension Contributions: The Cleanest Method to Reduce Corporation Tax Legally

If there’s one strategy that delivers a clean, HMRC-approved reduction in corporation tax with no complicated structuring required, it’s employer pension contributions.

When your company pays directly into a director’s or employee’s pension:

- The contribution is a fully deductible business expense for corporation tax purposes

- No National Insurance is payable on the contribution

- The individual pays no income tax on it as a benefit in kind

- The money grows largely tax-free inside the pension

At a 25% corporation tax rate, a £20,000 company pension contribution saves £5,000 in tax. That’s money going to the director’s future rather than to HMRC.

The annual allowance is £60,000 per year (or 100% of earnings if lower), and unused allowances from the previous three years can often be carried forward. If you’ve been underfunding your pension while the company has been profitable, there may be a genuine opportunity to catch up — and bring down this year’s bill in the process.

For businesses managing contributions for multiple staff, making sure your payroll is structured correctly from the outset matters. Automatic enrolment services cover this if you haven’t reviewed your setup recently.

Allowable Business Expenses That Legally Cut Your Corporation Tax Bill

The core rule: expenses wholly and exclusively incurred for business purposes are deductible against profits. The practice is where it gets interesting.

Commonly missed legitimate deductions:

- Home office costs (where the director genuinely works from home — calculated properly)

- Professional subscriptions and training directly relevant to the business

- Business mileage at HMRC-approved rates

- Marketing, website development, and digital advertising spend

- Accountancy, legal, and professional fees

- Bank charges and certain loan interest

- Staff entertaining — up to £150 per head annually

Where people get tripped up:

Client entertaining. This is probably the most common misconception in UK business tax. Entertainment of clients and customers is not deductible for corporation tax — full stop — even when it’s a completely legitimate commercial expense. Staff parties are different, with the £150 per head exemption, but client hospitality simply doesn’t qualify.

Dual-purpose expenses. A laptop used 80% for business and 20% personally lives in a grey area. HMRC expects consistency and, if challenged, evidence.

Cloud accounting software makes it significantly easier to categorise expenses correctly throughout the year rather than reconstructing everything come January. Clean records also make it far easier to defend deductions if HMRC ever asks questions.

Using Loss Relief to Reduce Corporation Tax Legally Across Multiple Years

If your company makes a loss in any accounting period, that loss doesn’t simply disappear. You can:

- Carry the loss forward against future profits of the same trade (indefinitely, subject to the £5 million deductions allowance)

- Carry back trading losses against profits from the previous 12 months — potentially generating a repayment from HMRC

- Group relief — if you have connected companies, losses in one entity can offset profits in another

The one-year carry-back remains available, and in a year of unexpected losses, it can produce a genuine tax repayment. Terminal loss relief (when ceasing to trade) allows losses from the final twelve months to be carried back three years — worth bearing in mind if a business closure is on the horizon.

Timing Your Income and Expenditure to Reduce Corporation Tax Legally

Corporation tax is charged on the profits of your accounting period. That creates a legitimate planning opportunity around transaction timing — particularly near your year-end.

If profits are running high this year:

- Bring forward planned capital expenditure to capture full expensing in this period

- Make employer pension contributions before year-end

- Pre-pay recurring costs (insurance, subscriptions) that cover the next period

- Defer income recognition where contractually justifiable

On the other side: if it’s been a difficult trading year, making large pension contributions might not be sensible if the funds are needed for working capital. Tax planning and cash flow planning need to work together. This is where business advice and financial consulting from someone who understands your full financial picture genuinely adds value — well beyond just completing returns.

Charitable Donations: A Straightforward Way to Reduce Corporation Tax Legally

Companies can deduct qualifying donations to registered charities from profits before calculating corporation tax. Unlike individuals using Gift Aid, companies don’t add tax to the donation — they simply deduct the gross amount from taxable profits.

A £5,000 donation to a registered charity reduces your corporation tax bill by £1,250 at the 25% rate. The charity receives the full amount. It’s a genuinely clean intersection of social purpose and sound financial management.

Note: donations that come with something in return — advertising, goods, services — may not qualify as straightforward charitable donations. Worth checking if substantial sums are involved.

Marginal Relief and Associated Companies — What Can Push Your Corporation Tax Rate Higher

| Scenario | Adjusted Threshold (each company) | Why It Matters |

|---|---|---|

| 1 company, no associates | £50k / £250k (standard) | Standard rates apply as expected |

| 2 associated companies | £25k / £125k per company | Both hit 25% rate earlier than anticipated |

| 4 associated companies | £12.5k / £62.5k per company | Main rate kicks in at very low profit levels |

| Short accounting period (e.g. 6 months) | Thresholds reduced proportionally | Companies incorporated mid-year often pay more than expected |

The associated companies rules mean holding companies, investment vehicles, or dormant companies you’d almost forgotten about can push your active trading company into a higher tax bracket. Reviewing which entities are truly associated under HMRC’s definition — and whether restructuring makes sense — is often worth the conversation. See HMRC’s guidance on associated companies for the technical definition.

HMRC Investigations: Why Proper Tax Planning Protects You as Well as Saves You Money

One aspect rarely covered in guides on how to reduce corporation tax legally is the protection that proper planning provides. HMRC’s Connect system cross-references data from Companies House, Land Registry, VAT returns, bank data, and more. Inconsistencies — even accidental ones — can trigger an enquiry. And a tax investigation is expensive and stressful regardless of whether you’ve done anything wrong.

The best protection is straightforward: clean, well-documented books, corporation tax returns filed accurately and on time, and relief claims backed by evidence. It’s not just about staying out of trouble — it’s about having the confidence to claim everything you’re genuinely entitled to, because your records can support it.

The team at Ask Accountants UK Ltd — based at 178 Merton High St, London SW19 1AY — work with businesses across a wide range of sectors on everything from tax compliance and bookkeeping through to HMRC investigation support. If you’re not currently getting proactive advice — rather than reactive compliance — it might be worth a conversation. Call them on 020 8543 1991.

Frequently Asked Questions: How to Reduce Corporation Tax Legally in 2026

Q: What is the most effective legal way to reduce corporation tax in 2026? There’s no single answer — it depends on your profit level, structure, and expenditure patterns. That said, employer pension contributions, capital allowances (full expensing on new equipment), and R&D tax credits consistently deliver the highest value for eligible businesses.

Q: Can I pay my spouse or family members to reduce corporation tax legally? Yes — provided they genuinely work in the business and receive a market rate for their role. HMRC will challenge wages that appear inflated or paid to someone doing little or no actual work.

Q: How do I reduce corporation tax legally if my company has associated companies? The thresholds for both the small profits rate and marginal relief are divided between associated companies, so you can hit the 25% main rate at a much lower profit level than a standalone company. Reviewing your corporate structure — particularly whether all listed entities are truly “associated” under the rules — is often worthwhile. Related: how to simplify accounting for a corporation.

Q: Is salary sacrifice a viable strategy for reducing corporation tax? Salary sacrifice arrangements — where employees reduce salary in exchange for pension contributions, electric vehicles, or cycle-to-work schemes — can cut both employee and employer NICs, with the NIC saving potentially benefiting the company. These need to be properly documented and HMRC-compliant. See HMRC’s guidance on salary sacrifice.

Q: Does investing in the business reduce corporation tax? Yes — capital investment in qualifying plant and machinery can often be fully deducted in the year of purchase via full expensing or the AIA. It’s one of the most direct ways to reduce taxable profits while simultaneously growing business capacity.

Q: What happens if I claim a relief I’m not entitled to? HMRC can raise an assessment, charge interest on underpaid tax, and levy penalties. Genuine mistakes attract lower penalties than deliberate errors — but the process is stressful regardless. Having a qualified accountant review your return before filing is the simplest protection. If you’ve already received a notice, the corporate tax return penalties guide is a useful starting point.

The Bottom Line on How to Reduce Corporation Tax Legally in 2026

There’s a version of this conversation that slides into increasingly territory — offshore structures, artificial loss schemes, contrived arrangements. That’s not what this article covers, and it’s genuinely not what most UK businesses need.

The methods outlined above to reduce corporation tax legally — pension contributions, capital allowances, R&D credits, proper expense deduction, smart director remuneration — are not loopholes. They are deliberate, Parliament-sanctioned features of the UK tax system, designed to reward investment, encourage innovation, and allow owner-managed businesses to operate efficiently. Using them is not aggressive planning. It’s just good financial management.

What it does require is proactive advice rather than annual box-ticking. If your accountant only contacts you once a year when your return is due, you’re probably missing something valuable. More on this: business advice every small business needs in 2026.

For businesses in London looking for genuinely proactive corporate tax planning support, Ask Accountants UK Ltd offers everything from cloud accounting and bookkeeping to company secretarial work and HMRC investigation support. Worth a call: 020 8543 1991.