Nobody warns you about the paperwork. You hear about the grief, the funeral arrangements, and the difficult family conversations. But the administrative maze that follows death? That blindsides most people completely. One of the most common questions professionals encounter when handling estates is: do I need to complete IHT400 before applying for probate? The answer — sometimes yes, sometimes no — depends entirely on the estate’s size and complexity. Getting it wrong could delay probate by months or trigger an HMRC investigation. This article unpacks the whole thing clearly, without burying you in legal jargon.

Why Probate and IHT400 Get Tangled Together

Probate — formally known as a Grant of Representation — gives an executor legal authority to deal with a deceased person’s estate. Banks won’t release funds, property can’t be sold, and assets sit frozen until the grant arrives. Understandably, most executors want to move quickly.

But HMRC has its own interest in estates that exceed certain thresholds. Before the Probate Registry issues a grant in certain circumstances, it needs confirmation that inheritance tax has been addressed. That confirmation, in complex or high-value estates, comes through the IHT400 — the main inheritance tax account form.

So if your estate requires an IHT400, you must submit it — and receive a receipt code from HMRC — before probate can proceed. The two processes are sequential, not parallel.

Not Every Estate Triggers IHT400

Many estates don’t require IHT400 at all. If HMRC classifies the estate as “excepted” — meaning it falls within certain parameters — a simpler process applies.

An estate is typically excepted if:

- The total value sits below the inheritance tax threshold (currently £325,000, or up to £500,000 where the residence nil-rate band applies)

- The estate passes entirely to a spouse, civil partner, or charity

- The estate meets the definition in the Inheritance Tax (Delivery of Accounts) (Excepted Estates) Regulations

For excepted estates in England, Wales, and Northern Ireland, executors apply for probate using the PA1P (with a will) or PA1A (without a will) forms — and simply declare that no IHT is due. No IHT400 required. No prior submission to HMRC needed.

That said, HMRC can still investigate after the fact. Signing that declaration carries genuine legal weight.

When You Genuinely Do Need to Complete IHT400 First

If the estate falls outside the excepted category — meaning it exceeds the threshold, involves complex assets, includes gifts made in the seven years before death, or holds assets in trust — you must complete the full IHT400 alongside relevant supplementary schedules.

Here’s the critical sequencing that catches most executors off guard:

- Complete and submit IHT400 to HMRC

- Pay any inheritance tax due — or arrange an instalment plan for illiquid assets like property

- Receive a unique probate code (reference number) from HMRC

- Include that code in your probate application

- The Probate Registry then processes your application

There’s no shortcut. The Probate Registry checks for this code. Without it, your application stalls.

How Long Will HMRC Take?

HMRC targets 20 working days to process an IHT400. In practice, during busy periods, this stretches considerably. Plan for four to six weeks from submission before you can apply for probate — and that assumes your IHT400 is complete and accurate on first submission, which isn’t always the case.

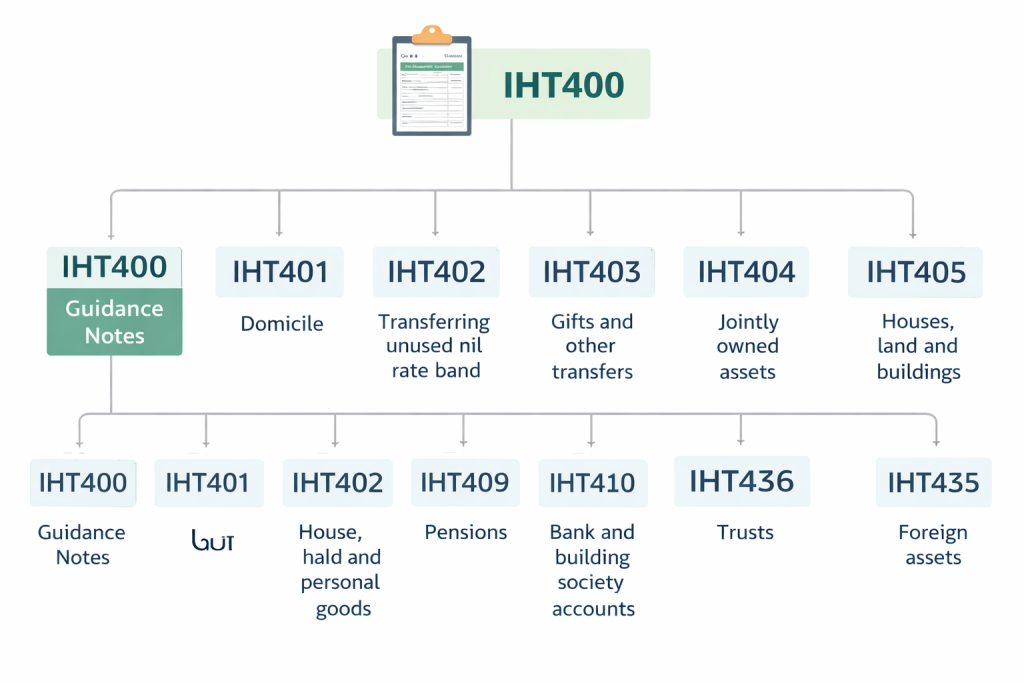

What the IHT400 Form Actually Involves

The main form runs to 16 pages. Depending on the estate’s complexity, you could complete anywhere from one to several supplementary schedules — IHT402 for claims on unused nil-rate band, IHT405 for houses and land, IHT406 for bank accounts, IHT407 for household contents, and so on.

The form asks you to account for every asset and liability, calculate the taxable estate value, claim any reliefs or exemptions, and declare lifetime gifts. Getting valuations right — particularly for property and investments — matters enormously. HMRC queries undervalued estates, and interest charges on unpaid tax accumulate fast.

For anyone dealing with a sizeable or complicated estate, having support from an experienced inheritance tax specialist — rather than piecing it together from guidance notes — saves both time and frequently money. The team at Ask Accountant in London handles exactly these kinds of estates regularly, particularly where business assets or property interests need careful valuation and relief claims.

The Excepted Estates Rule Changes Since 2022

In January 2022, the rules around excepted estates changed significantly. These changes directly affect how executors approach the question of whether IHT400 is needed before probate today.

Previously, the excepted estate threshold sat at £1 million for estates passing to a surviving spouse or civil partner. The 2022 changes extended this considerably:

- Estates up to £3 million passing entirely to a surviving spouse or civil partner now qualify as excepted

- Estates where the deceased held limited UK assets and was never UK domiciled also qualify

This means far fewer estates now require a full IHT400 before probate. If your estate falls into one of these expanded excepted categories, you can apply directly for probate without submitting anything to HMRC first.

But — and it’s a meaningful caveat — this only works where the estate genuinely qualifies. Misclassifying assets or overestimating threshold eligibility brings HMRC back post-probate to challenge the declaration.

HMRC’s own Inheritance Tax guidance and the GOV.UK probate pages are the authoritative starting point before seeking professional advice.

| Estate Type | IHT400 Required? | Probate Form | Notes |

|---|---|---|---|

| Excepted estate (below £325k, no complex assets) | No | PA1P / PA1A | Declare estate details on the probate form directly |

| Spouse/civil partner inheriting entire estate (up to £3m) | No (post-2022) | PA1P / PA1A | New rules since Jan 2022 — verify the estate qualifies first |

| Estate above nil-rate band with IHT to pay | Yes | PA1P / PA1A + HMRC code | Submit IHT400 and receive HMRC reference before applying |

| Estate with gifts made within 7 years of death | Yes | PA1P / PA1A + HMRC code | Include IHT403 schedule for lifetime gifts |

| Estate with business or agricultural assets | Yes | PA1P / PA1A + HMRC code | May qualify for Business Relief or Agricultural Relief |

| Estate with assets held in trust | Usually yes | PA1P / PA1A + HMRC code | Depends on trust type — take professional advice |

What Happens If You Skip IHT400 When You Shouldn’t

This is the scenario nobody wants to find themselves in — but it happens. Executors sometimes genuinely don’t realise the estate required a full IHT400. Perhaps they underestimated the asset values, overlooked gifts, or received poor advice early on.

The Probate Registry should catch obvious cases where HMRC involvement is clearly needed. But the system isn’t foolproof. If a grant goes out when IHT400 should have been completed, HMRC can open an investigation afterwards. Penalties apply. Interest accrues on unpaid tax from the date it was due — typically six months after the end of the month in which the person died.

Can Beneficiaries Challenge the Administration?

Yes — and this is a risk executors often underestimate. Beneficiaries or other interested parties can challenge an estate administration that appears to have skipped required steps. That creates legal exposure for the executor personally. It’s a headache nobody needs on top of the grief of bereavement.

The Paying-Before-Probate Problem — A Real Catch-22

Here’s something that surprises almost every executor: if the estate requires IHT400 and inheritance tax is due, you must pay at least some of it before you get probate — but you can’t access the deceased’s assets until after probate arrives. Circular, yes.

This is known informally as the “probate funding gap,” and it creates genuine practical difficulties.

Three Ways Around the Funding Gap

Executors have options. Banks operate direct payment schemes where HMRC collects funds from the deceased’s accounts before probate — the executor arranges this with the bank using Form IHT423, and the funds transfer straight to HMRC. Not all institutions participate, but most major high street banks do.

Some executors take out a short-term probate loan to cover the IHT bill temporarily. This costs money in interest, but it keeps the estate moving.

For larger estates with illiquid assets like property, HMRC allows inheritance tax payments in ten equal annual instalments. This eases the immediate pressure considerably. You still need to submit IHT400 and receive your probate code first — but at least you’re not scrambling to find the full tax bill upfront.

| Schedule | What It Covers | When Required |

|---|---|---|

| IHT402 | Claim for unused nil-rate band from predeceased spouse/civil partner | When transferring unused allowance |

| IHT403 | Gifts and other transfers made in lifetime | When gifts exceed annual exemptions or fall within 7 years |

| IHT405 | Houses, land, buildings and interests in land | Almost always — most estates include property |

| IHT406 | Bank and building society accounts | Standard inclusion for most estates |

| IHT412 | Unlisted stocks, shares, and private business interests | Where business assets are held privately |

| IHT416 | Debts owed to the estate | Where the deceased lent money to others |

| IHT435 | Claim for residence nil-rate band (RNRB) | When property passes to direct descendants |

Note: This is a selected list. Always check the latest IHT400 form guidance from HMRC, as schedules occasionally change.

Scotland: A Different Name, the Same IHT Rules

If the estate involves Scottish assets or the deceased lived in Scotland, the process uses different terminology. Scotland uses Confirmation rather than probate, and the Sheriff Court handles applications rather than the Probate Registry.

However, inheritance tax itself still operates as an HMRC matter — the same rules apply across the entire UK. Whether you seek Confirmation in Scotland or probate in England and Wales, if IHT400 is required, you must complete it first. The HMRC submission process doesn’t change based on jurisdiction.

For Scottish estates, Form C1 replaces PA1P for the Confirmation application. But the need to resolve IHT before proceeding remains identical in non-excepted estates.

A Realistic Timeline for Executors Who Need to Complete IHT400 Before Applying for Probate

Since the original question is at root a sequencing question, here’s what a realistic timeline looks like for an estate that requires IHT400:

Weeks 1–4: Gather everything Track down all assets and liabilities. Obtain professional valuations for property and non-standard assets. Find all accounts, insurance policies, shareholdings, and outstanding debts. Notify HMRC of the death if applicable.

Weeks 4–8: Complete IHT400 Work through the form and all relevant schedules. This is the stage where professional help genuinely pays for itself. An experienced inheritance tax adviser spots reliefs and exemptions that a layperson misses — and missing them is expensive.

Weeks 8–12: Submit and pay Send IHT400 to HMRC. Arrange payment of inheritance tax due or the first instalment. Then wait for HMRC to process the submission and issue the probate code. Allow six to eight weeks in practice, not the official 20 working days.

Weeks 12–16+: Apply for probate Submit the PA1P or PA1A with the HMRC reference number included. The Probate Registry adds its own processing time — typically four to eight weeks depending on caseload.

So realistically: four to six months minimum from death to grant of probate, for a complex estate requiring IHT400. Often longer. Plan accordingly.

⚠️ Watch Out: HMRC charges interest on unpaid inheritance tax from six months after the end of the month of death. Interest keeps running even while HMRC processes your paperwork. Start the IHT400 process early — not because of arbitrary deadlines, but because the financial cost of delay is real and avoidable.

Reliefs That Reduce What You Owe — Don’t Leave Money on the Table

One of the most expensive mistakes executors make when completing IHT400 is failing to claim all available reliefs. The form asks for them — but it doesn’t flag which ones apply to your specific estate.

Business Property Relief (BPR) reduces the taxable value of qualifying business assets by 50% or 100%. This applies to interests in unincorporated businesses, shares in unlisted companies, and some AIM-listed shares. The relief is substantial and gets missed more often than it should.

Agricultural Property Relief (APR) applies to agricultural land and farmhouses — again at 50% or 100% depending on the nature of the interest.

Nil-Rate Band Reliefs Worth Knowing

The Residence Nil-Rate Band (RNRB) — currently £175,000 — applies when a residential property passes to direct descendants. Combined with the standard nil-rate band, this shields up to £500,000 from IHT for a single person, or £1 million for a married couple through transfers. Executors must complete IHT435 to claim it.

The transferable nil-rate band — claimed via IHT402 — lets you add the unused portion of a predeceased spouse’s or civil partner’s nil-rate band to the survivor’s threshold. Many families discover this only once they’re already deep in the IHT400 process.

The Charitable Giving Rate Reduction

If the will directs at least 10% of the net estate to charity, the IHT rate drops from 40% to 36%. For larger estates, this is worth modelling carefully — particularly where beneficiaries have some flexibility in their expectations.

HMRC’s Inheritance Tax forms page and their Business Relief guidance cover these reliefs in detail. Our IHT400 complete guide also walks through how these reliefs interact in practice.

When to Get Professional Help — and When You Probably Don’t Need It

If the estate is genuinely simple — one property, a couple of bank accounts, no gifts, passing to a spouse — and it clearly qualifies as excepted, many executors handle the process without professional help. HMRC’s guidance is thorough, and the PA1P form is navigable.

But if any of these apply, the cost of professional support pays for itself quickly:

- The estate exceeds the IHT threshold and IHT400 is required

- The estate holds business interests, farm assets, or investment portfolios

- The deceased made gifts in the seven years before death

- Assets sit in multiple countries

- Beneficiaries disagree about the estate administration

- You simply don’t have months to dedicate to what is, objectively, a complex administrative process

The team at Ask Accountant — based at 178 Merton High St, London SW19 1AY — handles inheritance tax work as part of a wider range of tax advisory services. Whether that means claiming the right reliefs, defending valuations with HMRC, or simply ensuring IHT400 schedules go in correctly the first time, having experienced hands on the form before submission prevents costly delays. Call them on +44(0)20 8543 1991 to talk through your situation.

FAQ: Do I Need to Complete IHT400 Before Applying for Probate?

Can I apply for probate at the same time as submitting IHT400? No. You submit IHT400 first, wait for HMRC to process it and issue a reference code, then apply for probate. These steps happen in sequence.

What if I can’t tell whether the estate is excepted or not? Complete IHT400 anyway. It’s more work — but it’s far better than under-declaring and facing HMRC interest charges or penalties later. If genuinely uncertain, speak with a tax specialist or call HMRC’s probate helpline directly.

How long does HMRC take to process IHT400? HMRC’s official target is 20 working days. In practice, during busy periods, this stretches considerably. Build six to eight weeks into your timeline as a working assumption.

What happens if I find assets after probate is granted? You may need to submit a further IHT400 return or an amendment. Additional IHT may be owed, plus interest if those assets should have been declared earlier. Take advice before deciding how to proceed — don’t just ignore it.

Does the executor personally owe the inheritance tax? The estate owes inheritance tax, not the executor personally. However, executors carry a legal duty to ensure the estate pays it correctly and on time. An executor who distributes assets before settling IHT can face personal liability. That’s a responsibility that deserves serious attention.

Can I use the deceased’s bank accounts to pay IHT before probate? Yes — through the direct payment scheme. HMRC can collect IHT from the deceased’s UK bank accounts before probate using Form IHT423. Most major high street banks participate. Not all accounts qualify, so check with the bank early.

One Final Thought

Dealing with an estate is one of those tasks where the gap between “I think I understand this” and “I actually understand this” carries a financial price tag. The IHT400-before-probate sequence genuinely confuses most people the first time they encounter it — but once you understand the logic, the path through it becomes manageable.

Start early. Get valuations done promptly. Don’t assume an estate qualifies as excepted without checking carefully. And if the numbers are significant or the assets are anything other than straightforward, get proper advice. The cost of professional help is almost always smaller than the IHT saved through correctly claimed reliefs — or the interest avoided by getting the timeline right.

For more on navigating the IHT400 and probate process, Ask Accountant’s inheritance tax hub and their detailed IHT400 complete guide are practical starting points alongside HMRC’s official resources. You might also find their piece on IHT400 processing times useful for setting realistic expectations.