Nobody sits down one Tuesday morning and thinks, “Today I’ll become an expert in inheritance tax forms.” Yet here you are — probably recently bereaved, probably confused, and almost certainly staring at a 16-page HMRC document wondering how something this important can also be this bewildering.

The IHT400 is the main inheritance tax return in the UK. If the deceased’s estate is liable for inheritance tax — or even if it might be — you’ll need to complete and submit this form before you can obtain a grant of probate. That single fact makes it arguably the most consequential piece of paperwork most people will ever touch.

This guide walks you through the IHT400 from the first page to the final signature, explaining what each section actually means in plain English, which supplementary schedules you’ll likely need, how to avoid the mistakes that slow HMRC processing down, and when calling a professional is genuinely the smarter move.

First, Let’s Sort Out Who Actually Needs to Complete IHT400

Not every estate triggers the full IHT400 process. Understanding who needs to complete IHT400 is the sensible first step before you write a single thing.

You’ll need to fill in IHT400 when:

- The estate is worth more than the nil-rate band (currently £325,000) — though see below for the residence nil-rate band

- The deceased made significant gifts in the seven years before death

- The estate includes assets that qualify for reliefs like Business Property Relief or Agricultural Property Relief

- There are complex assets — overseas property, trust interests, or business interests

If the estate is clearly below the threshold and no reliefs are being claimed, you may instead use the simpler IHT205 (for deaths before January 2022) or the newer online process. HMRC’s own guidance on when IHT400 is required is worth reading before proceeding.

For deaths on or after 1 January 2022, the IHT205 was abolished — which means more estates now fall into IHT400 territory. Worth knowing.

Before You Touch the Form: Gather Everything

Attempting to fill in IHT400 without complete information is a bit like trying to bake a cake having checked the fridge but not the cupboards. You’ll get halfway through and realise something’s missing.

Here’s what you’ll realistically need before you start:

- Death certificate (you’ll need multiple certified copies)

- The will and any codicils

- Valuations for all assets — property, investments, bank accounts, personal possessions, vehicles

- Details of all debts and liabilities — mortgages, loans, credit cards, funeral costs

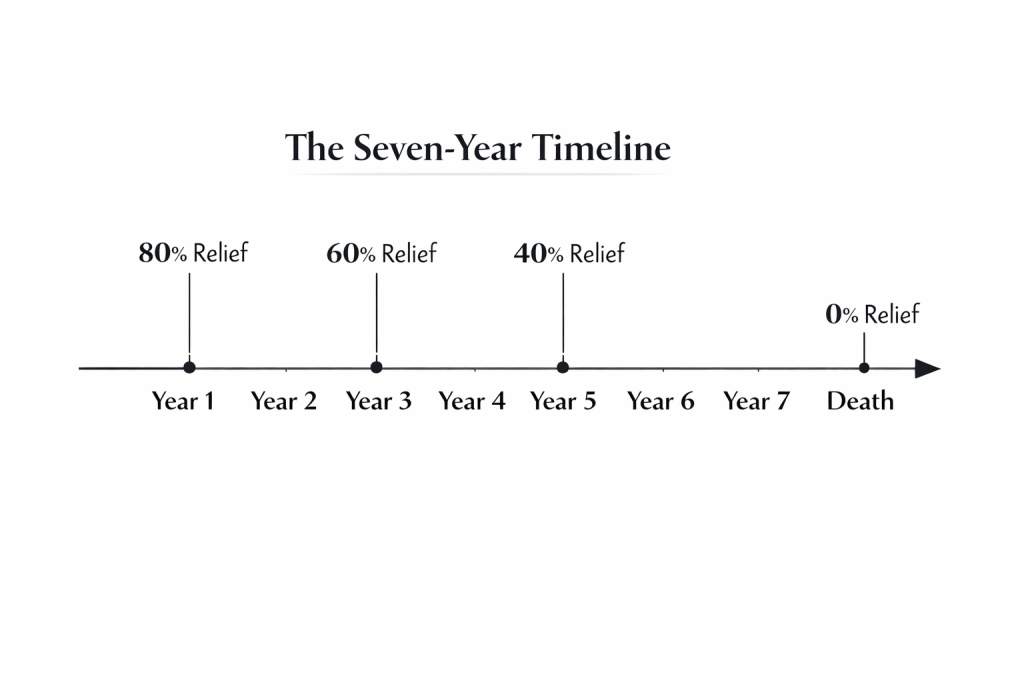

- Records of any gifts made in the previous seven years (the seven-year rule catches many executors off guard)

- Pension details — though pensions are generally outside the estate for IHT purposes, you’ll want to confirm this

- Details of any trusts the deceased was involved in

- Business interests and their valuations if applicable

Property valuations are particularly important. HMRC can and does challenge these — so getting a professional RICS-certified valuation is advisable, not optional, if property is involved. See our help filling in inheritance tax forms resource for more guidance on what documents you’ll need to hand.

The IHT400 Form Structure: What You’re Actually Looking At

The IHT400 runs to 16 pages, split into numbered sections. Each section collects a different category of information. Here’s an honest overview:

| IHT400 Section | What it covers | Difficulty (honest) |

|---|---|---|

| Pages 1–3 | Deceased’s personal details, domicile, executors | Straightforward |

| Pages 4–7 | Assets — UK property, investments, bank accounts, household goods | Moderate |

| Pages 8–10 | Foreign assets, jointly owned assets, nominated assets | Can be complex |

| Pages 11–12 | Gifts, trusts, and assets held in trust | Often the trickiest bit |

| Pages 13–14 | Reliefs and exemptions (spouse, charity, BPR, APR) | Moderate to complex |

| Pages 15–16 | Tax calculation, payment details, declaration | Straightforward once earlier pages are correct |

Pages 1–4: The Biographical Groundwork

The opening pages of the IHT400 ask for the deceased’s full name, address, date of birth and death, their National Insurance number, and domicile status. Domicile is not the same as residence — it’s a legal concept that determines which country’s tax laws govern an estate, and if the deceased spent significant time abroad or was born overseas, it may need careful thought.

You’ll also confirm whether the deceased left a will, list the executors or administrators, and confirm whether you’re applying for a grant of probate or letters of administration.

One question that trips people up: “Was the deceased entitled to assets in a trust?” Don’t skip past this. Many people hold life interests in trusts from deceased parents and have entirely forgotten about them.

The Assets Sections: This Is Where Accuracy Really Matters

Pages 4 through 10 cover the estate’s assets, and this is where the IHT400 demands real care. HMRC compares the valuations you provide against comparable sales data, land registry records, and in some cases their own internal benchmarks. Undervaluing — even accidentally — can trigger HMRC investigations and penalties.

Property: Enter the open market value at the date of death. For jointly owned properties, enter the deceased’s share only — though this gets complicated if it was owned as joint tenants versus tenants in common.

Bank and savings accounts: Use the balance at the date of death. Don’t forget ISAs — they form part of the estate for IHT purposes even though they’re tax-free during life.

Investments: Shares are valued using the “quarter up” rule — midway between the lower quarter and upper quarter of the day’s trading range. Your stockbroker can provide this, or you can use historical share price data from the London Stock Exchange or similar sources.

Personal chattels: Furniture, jewellery, vehicles, art. A professional valuation is not legally required for lower-value estates, but HMRC expects reasonable figures. Saying “miscellaneous household goods: £500” for a four-bedroom house packed with antiques will raise eyebrows.

The Gifts Question: Seven Years of Reckoning

Pages 11 and 12 deal with gifts — and this section makes many executors very uncomfortable, particularly when they realise they need to reconstruct seven years of financial history from bank statements and family memory.

The IHT400 asks about:

- Gifts made in the seven years before death — regardless of whether they would have been exempt

- Gifts with reservation of benefit — where the deceased gave something away but continued to benefit from it (classic example: gave the house to the children but kept living in it)

- Exempt transfers — gifts to spouses or civil partners, charitable donations, small gifts within annual exemptions

The seven-year rule and its impact on inheritance tax is one of the more misunderstood aspects of estate planning. Gifts made more than seven years before death are generally outside the estate; those made within three years are fully taxable. Between three and seven years, taper relief applies on a sliding scale.

⚠️ A note on gifts with reservation: If the deceased gave away their home but continued to live there rent-free, that property is treated as still belonging to the estate for IHT purposes — regardless of when the gift was made. This is a common and expensive surprise.

Reliefs and Exemptions: The Bit That Could Save the Estate Real Money

This is where knowing the rules properly pays off. Pages 13–14 of the IHT400 cover reliefs and exemptions, and claiming them correctly (or indeed at all) can dramatically reduce the tax bill.

Spouse/civil partner exemption: Transfers between spouses are exempt from IHT — both during life and on death. If the entire estate passes to a surviving spouse, no IHT is due. The nil-rate band can also be transferred to the surviving spouse’s estate when they die.

Residence Nil-Rate Band (RNRB): An additional £175,000 allowance (2024/25 figure) where a residential property passes to direct descendants. This can be complex to calculate — especially for larger estates where it tapers away above £2 million.

Business Property Relief (BPR): If the deceased owned a business or shares in an unlisted company, BPR may provide 50% or 100% relief. The rules are specific and HMRC scrutinises these claims carefully.

Charitable legacies: Gifts to registered charities are exempt, and leaving 10% or more of the net estate to charity reduces the IHT rate from 40% to 36%.

Our inheritance tax reliefs guide covers each of these in more depth if you want to explore them before completing the form.

The Supplementary Schedules: IHT400’s Supporting Cast

The main IHT400 form doesn’t stand alone. Depending on what’s in the estate, you’ll need to complete additional schedules — officially called “supplementary pages.” Missing the right ones is one of the most common reasons HMRC returns submissions for correction.

| Schedule | When required |

|---|---|

| IHT401 | Deceased was domiciled outside the UK |

| IHT402 | Claiming the transferred nil-rate band from a deceased spouse |

| IHT403 | Gifts and other transfers of value in the seven years before death |

| IHT404 | Jointly owned assets |

| IHT405 | Houses, land, buildings and interests in land |

| IHT406 | Bank and building society accounts |

| IHT407 | Household and personal goods |

| IHT408 | Household and personal goods donated to charity |

| IHT409 | Pensions |

| IHT410 | Life assurance and annuities |

| IHT411 | Listed stocks, shares and investments |

| IHT412 | Unlisted stocks, shares and investments |

| IHT413/IHT414 | Business and partnership interests / Agricultural relief |

| IHT416 | Debts owed to the estate |

| IHT418 | Assets held in trust |

| IHT419 | Debts owed by the deceased |

| IHT421 | Probate summary — sent to the Probate Registry |

The IHT400 schedules explained guide on our website goes through each of these in more detail, including which schedules are most commonly missed.

Deadlines: The Clock Is Already Running

The IHT400, along with any tax due, must be submitted within six months of the end of the month in which the person died. So if someone died on 14 March, the deadline is 30 September of the same year.

Here’s the catch: probate cannot be granted until HMRC confirms the IHT position — and IHT must be paid before probate is granted, even though you technically can’t access many of the estate’s assets without probate. It’s a bit of a chicken-and-egg situation, which is why early preparation matters enormously.

HMRC processing times for IHT400 currently run anywhere from 12 to 20 weeks for straightforward cases — so the earlier you submit, the better. Interest accrues on unpaid IHT from the six-month deadline, currently at HMRC’s standard late payment rate.

Some assets — particularly property — can be paid in annual instalments over ten years rather than all at once. This option must be elected on the form.

Can You Submit IHT400 Online?

This is one of the most searched questions around this process, and the answer is — mostly no, as of 2025. The IHT400 itself must be printed and posted to HMRC’s Inheritance Tax department. However, some supporting information can now be submitted digitally in certain circumstances.

The full picture on whether you can submit IHT400 online has changed slightly over the past few years as HMRC has piloted digital options, so it’s worth checking current guidance directly at gov.uk/inheritance-tax before assuming paper-only is still the rule.

Mistakes That Cost Executors Time, Money, and Sleep

A few errors come up repeatedly in the IHT400 process — not because executors are careless, but because the form itself doesn’t always make the consequences of getting something wrong entirely obvious.

Undervaluing property. This is HMRC’s single biggest area of scrutiny. District Valuer Services can be called in to review valuations, and if HMRC decides the property was undervalued, the executor (not just the estate) can be held liable.

Missing the IHT403 schedule. If the deceased made any gifts in the seven years before death — including birthday money that exceeds the annual exemption — the IHT403 must be completed. Many executors don’t realise how far back they need to look.

Forgetting jointly owned assets. A property owned jointly with a spouse or partner doesn’t automatically disappear from the estate — it depends entirely on whether it was held as joint tenants or tenants in common.

Not claiming the transferred nil-rate band. If the deceased’s spouse died first and didn’t use their full nil-rate band, that unused portion can be transferred. This requires IHT402, and it’s surprisingly often overlooked.

Errors in the tax calculation. The calculation on pages 15–16 references values from multiple earlier pages and schedules. A single transcription error can cascade through the entire calculation. Checking figures twice — and ideally having a second person review them — is time well spent.

Do You Need to Complete IHT400 Before Applying for Probate?

Yes. In most cases where IHT400 is required, you must complete the IHT400 before applying for probate — or at least submit it at the same time. HMRC needs to acknowledge the submission (and in taxable estates, receive payment) before the Probate Registry will process the application.

There are specific forms involved in this handover: the IHT421 (Probate Summary) is sent by HMRC directly to the Probate Registry once they’ve processed the IHT400. Until that happens, the probate application sits in a queue.

A Word on Getting Professional Help

There’s no shame in finding this overwhelming. The IHT400 was designed for professional advisers, not grieving family members trying to administer an estate between work and everything else life throws at them.

At Ask Accountants UK Ltd, based in Wimbledon (178 Merton High St, London SW19 1AY), the team regularly assists executors with completing and submitting IHT400 forms — including identifying the right supplementary schedules, checking valuations, ensuring reliefs are properly claimed, and managing the process through to probate. They handle personal tax planning, tax compliance, and HMRC investigations — so navigating the inheritance tax process is well within scope. You can reach them on 020 8543 1991.

If you decide to engage professional help, do it early — ideally before you start filling in the form, not after you’ve already submitted something that needs correcting.

FAQs: The Questions People Actually Ask

What happens if I miss the IHT400 deadline? Interest runs on any unpaid tax from the six-month deadline. Late submission can also delay probate significantly. HMRC may also charge penalties in cases of deliberate delay or omission.

Can I amend the IHT400 after submission? Yes — you can submit a corrective account (IHT400 Corrective Account) if values change after submission, for example if a property sells for a different amount than the probate valuation.

What if the estate has no IHT to pay but still needs IHT400? Some estates are required to complete IHT400 even when no tax is due — for example, where reliefs reduce the liability to zero, or where the estate is just over the threshold. The IHT400 notes from HMRC explain exactly when this applies.

How long does HMRC take to process IHT400? Currently between 12 and 20 weeks for standard cases, though complex estates can take longer. HMRC’s IHT400 processing times have been a source of frustration for many executors in recent years.

Does the IHT400 need to be witnessed or certified? The declaration on page 16 must be signed by all executors named in the application. It doesn’t need a witness, but all executors must sign — not just the lead one.

What is the IHT400 calculation worksheet? HMRC provides a separate calculation worksheet (IHT400 Calculation) to help work out the tax due. This is submitted alongside the main form, not instead of it.

Filling In IHT400: The Short Version (For Those Who’ve Read Enough)

Completing the IHT400 is genuinely demanding — not because the questions are philosophically complex, but because getting them right requires comprehensive information, careful arithmetic, and familiarity with inheritance tax rules that most people encounter only once or twice in a lifetime.

If the estate is straightforward — a house, some savings, a straightforward will, no lifetime gifts of note — a diligent executor with organised paperwork can manage it. If there are trusts, business interests, foreign assets, disputed valuations, or seven years of gift history to reconstruct, professional guidance will almost certainly save both time and money.

Either way: start early, gather everything before you write a word on the form, and don’t rush the valuations. HMRC has seen every shortcut, and none of them save time in the long run.