By the team at Ask Accountants UK Ltd · Updated April 2026 · 10 min read

The government’s MTD programme has been rolling out in stages for years now, having already transformed how VAT-registered businesses handle their returns (if you want to understand how that played out, our piece on Making Tax Digital for VAT covers the full picture). Now it’s income tax’s turn — and landlords are squarely in the frame.

Whether you own a single flat in Wimbledon or a portfolio of twenty properties scattered across London, Making Tax Digital for Income Tax Self Assessment (MTD ITSA) is heading your way. What changes, what you’ll need to do, and crucially — what the deadlines actually are — that’s what this guide is here to untangle.

⚠ Don’t Wait on This One

Unlike some HMRC changes that creep up slowly, MTD for landlords has hard rollout dates. Landlords earning over £50,000 from property and/or self-employment are already in scope from April 2026. The next threshold — £30,000 — follows in April 2027. Leaving preparation to the last minute here could mean penalties, failed software sign-ups, and a frantic rush to find compatible software during a period when everyone else is doing the same.

What Making Tax Digital for Landlords Actually Means (Without the Jargon)

Let’s strip it back. At its core, Making Tax Digital for landlords means two things change fundamentally:

- How you keep your rental records — they must be kept digitally, using compatible software.

- How often you report to HMRC — instead of one annual Self Assessment, you’ll submit quarterly updates of your rental income and expenses throughout the year, then a final annual declaration to wrap things up.

Gone, at least for income tax purposes, is the single annual tax return that landlords have historically filed (often in a January panic, let’s be honest). In its place: four quarterly digital submissions, plus an end-of-year summary. Think of it like filing a rough draft four times, then a polished final version once.

The quarterly updates don’t have to be perfect. HMRC has been clear that they’re about providing a running picture of income and expenses — not a precise tax calculation each quarter. You make corrections and adjustments in your final declaration. But — and this matters — you still have to submit them on time, even if the figures are preliminary.

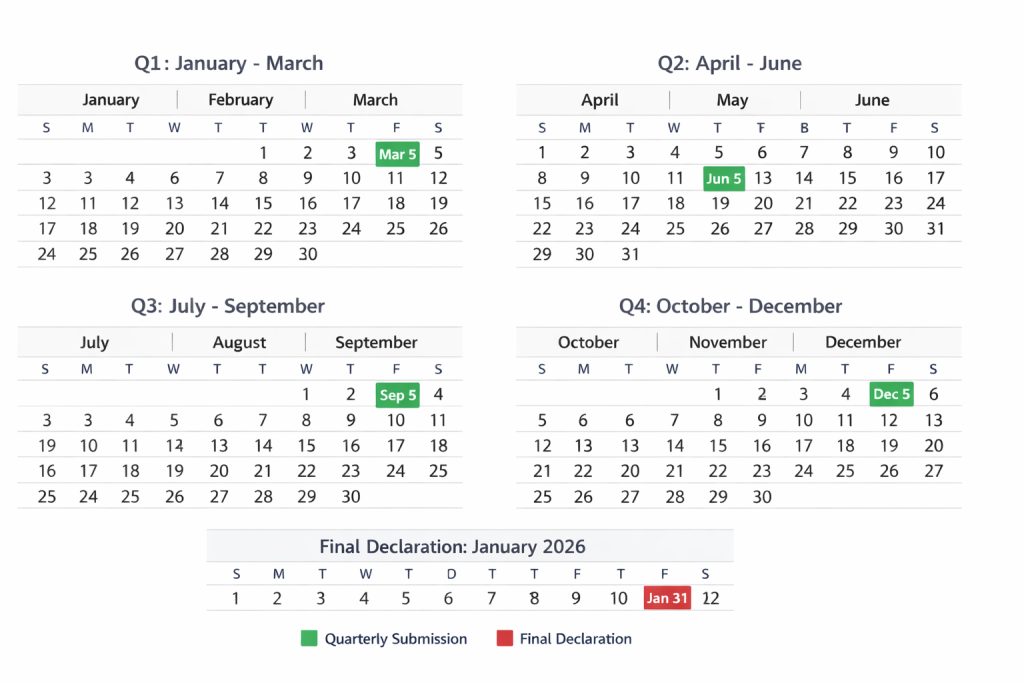

The Quarterly Submission Dates Landlords Need to Know

| Quarter Period | Submission Deadline | What to Include |

|---|---|---|

| 6 April – 5 July | 5 August | Rental income received + allowable expenses for the period |

| 6 July – 5 October | 5 November | Rental income received + allowable expenses for the period |

| 6 October – 5 January | 5 February | Rental income received + allowable expenses for the period |

| 6 January – 5 April | 5 May | Rental income received + allowable expenses for the period |

| End of Year Declaration | 31 January (following year) | Final figures, adjustments, other income sources, tax due |

Note: Quarter dates can align to calendar months (1st–31st) if your software supports the alternative quarterly period elections.

Who Gets Pulled In — and When

Not every landlord is in scope from day one. HMRC is rolling this out in waves, based on qualifying income thresholds. That said, “qualifying income” here means your gross income from property and self-employment combined — not your profit, not what’s left after mortgage payments.

| Qualifying Gross Income | MTD ITSA Start Date | Notes |

|---|---|---|

| Over £50,000 | April 2026 | Already in scope — preparation should be underway now |

| Over £30,000 | April 2027 | Start planning in 2026; software sign-up opens well before |

| Over £20,000 | April 2028 (proposed) | Announced in Spring Statement 2025; legislation pending |

| Under £20,000 (property income) | No confirmed date yet | Watch for future announcements; not currently mandated |

| Jointly owned property | Depends on individual share | Each owner assessed on their share of the income separately |

| Limited company landlords | Not in scope (currently) | MTD ITSA applies to individuals, not Ltd companies — Corporation Tax MTD is a separate programme |

Source: HMRC guidance, updated 2025–26. Thresholds are gross income, not profit.

A practical note: if you’re a landlord who also has self-employment income — a builder who rents out a couple of properties on the side, say — both income streams count towards that threshold together. If they tip you over £50,000 combined, you’re in from April 2026.

💡 Tip Worth Bookmarking

If you’re jointly owned on a property with a spouse or partner, HMRC looks at each person’s share individually. If you each receive £26,000 gross from the property, neither of you hits the £50,000 threshold — but you’d both be caught from April 2027 at the £30,000 level. This catches more landlords than you’d expect.

The Software Question: This Is Where It Gets Expensive (Or Doesn’t)

Making Tax Digital for landlords doesn’t just change when you report — it mandates how you report. You’ll need HMRC-recognised software to keep digital records and submit your quarterly updates directly. Spreadsheets alone won’t cut it, unless they’re connected to bridging software that handles the digital link.

The landscape of compatible software is genuinely expanding. QuickBooks, Xero, FreeAgent, Sage — all the major names are developing MTD ITSA-compliant products. If you’re already using cloud accounting software, chances are your provider will have an update. If you’re still managing things in a spreadsheet (or, whisper it, in a physical ledger), now’s the time to rethink that.

We’ve put together a detailed guide on using QuickBooks as a landlord, which goes through the practical setup for rental property tracking — including how to categorise income and expenses in a way that’ll translate cleanly into your quarterly submissions.

The honest reality? For landlords with straightforward portfolios, the ongoing cost of MTD-compatible software is fairly modest — often £10–30 per month. The actual effort is in the initial setup and making sure your records are properly categorised from the start. Get that right once, and the quarterly submissions themselves become genuinely quick.

Our cloud accounting service is built around exactly this kind of setup — making sure the software is configured correctly for rental property accounting, so the quarterly submissions are pulling through accurate figures rather than a tangled mess of uncategorised transactions.

Can You Still Use a Spreadsheet?

Technically — sort of. HMRC allows “bridging software” that connects a spreadsheet to its systems, enabling compliant digital submissions. In practice, this is a somewhat clunky middle ground: you’re maintaining a spreadsheet and paying for bridging software, instead of just using proper cloud accounting. For most landlords, it works out cheaper and less faff to switch to full cloud software. But if you’ve built elaborate spreadsheets over the years and genuinely love them, bridging is an option.

What Actually Changes in Your Day-to-Day as a Landlord

Here’s where I think a lot of guidance goes wrong — it talks about Making Tax Digital for landlords in abstract policy terms rather than what it actually means on a Tuesday morning when rent has come in and you’ve just paid a plumber £340 to fix a boiler.

In practical terms, here’s what shifts:

- Every rental receipt needs logging digitally as it happens (or at least regularly — not once a year in January). Bank feeds in cloud accounting software make this largely automatic once set up.

- Every allowable expense needs a digital record — repairs, insurance, letting agent fees, accountancy costs, ground rent, service charges. Again, software handles much of this if your bank account is connected.

- Four times a year, you or your accountant submits a digital update to HMRC. This isn’t a tax payment — it’s just a data submission. Actual tax is still settled via the annual declaration and payment on account system.

- Your records need to be kept for longer in digital form — HMRC may need access to them in the event of a compliance check.

For landlords who are already using bookkeeping software, the change is genuinely minimal. Four quarterly submissions via the software they already use. For landlords who’ve been filing a rough-and-ready Self Assessment once a year from a folder of receipts — the adjustment is more significant. Not insurmountable, but it does require forming new habits.

“The quarterly submissions don’t require perfection. What they do require is a functioning system — and that’s what landlords need to build now, not in March 2027.”

Expenses, Deductions, and Whether Anything Actually Changes There

Short answer: no. The rules on what you can and can’t deduct from rental income aren’t changing under Making Tax Digital. What changes is how and when those deductions are recorded and reported.

So the Section 24 mortgage interest restrictions — still in place. The wear and tear rules — unchanged. The ability to deduct repairs (but not improvements) — same as before. If you’ve been navigating personal tax planning around your rental income already, that planning doesn’t fundamentally shift under MTD.

What does change, slightly, is the timing of how these feed into your tax picture. With quarterly submissions, HMRC will have a running view of your rental profit throughout the year. This isn’t just administrative — it’s potentially useful for your own cash flow planning, too. You’ll have a clearer sense of your likely tax liability months before it’s due, rather than discovering it in January.

Penalties: HMRC’s New Points-Based System

This is where Making Tax Digital for landlords introduces something genuinely new — and genuinely worth understanding before you accidentally rack up a fine.

HMRC is moving to a points-based penalty system for late MTD ITSA submissions. Miss a quarterly deadline, you get a penalty point. Accumulate enough points (the threshold for quarterly submissions is four points), and you receive a £200 financial penalty. The points then start accumulating towards your next penalty.

There’s also a separate late payment penalty regime — an initial 2% charge if tax is still unpaid at 15 days after the due date, rising to 4% at 30 days, and then a daily rate of 4% per annum after that.

The points system sounds relatively gentle until you do the maths: four quarterly submissions per year means you could theoretically hit four points — and a £200 fine — in a single tax year from missing every submission. Miss them consistently across two years and you’ve got multiple £200 penalties stacking up. It’s not ruinous, but it’s entirely avoidable.

For the full picture on what HMRC investigations and compliance checks can involve, our guide to HMRC investigations is worth a read — particularly if your rental income history is complex or you’ve had gaps in your filing.

Limited Company Landlords: Are You Off the Hook?

For now, yes — mostly. Making Tax Digital for Income Tax applies to individuals with rental or self-employment income above the relevant thresholds. If your properties sit inside a limited company, the company files Corporation Tax returns, which are governed by a separate (and currently separate-timeline) MTD programme called Making Tax Digital for Corporation Tax.

That said, if you’re a director of a property company and you personally own some properties alongside it, your personal rental income may still fall under MTD ITSA requirements.

It’s also worth noting that the tax landscape for limited company landlords has shifted considerably over the past few years — property accounting via a limited company involves a distinct set of considerations that go well beyond just MTD compliance. If you’re unsure whether your structure is still working optimally, that’s a conversation worth having sooner rather than later.

The Practical Preparation Checklist — Actually Useful, Not Just a List of Vague Advice

Right. If you’re in scope from April 2026 (gross income over £50,000), here is what a sensible preparation timeline looks like:

- Confirm your qualifying income. Add up your gross rental receipts (not profit) and any gross self-employment income. If it exceeds £50,000, you’re in scope now.

- Choose your software. Research MTD ITSA-compatible platforms — QuickBooks, Xero, FreeAgent, Sage are all developing compliant solutions. Check HMRC’s updated list at gov.uk for the latest approved providers.

- Set up your property accounting categories. Each property should ideally have its own income and expense categories — rental income, repairs, insurance, letting agent fees, mortgage interest (for reference, not deduction), etc.

- Connect your bank feeds. Most cloud accounting software connects directly to your bank account, pulling in transactions automatically. This is the single biggest time-saver in the whole MTD setup process.

- Register for MTD ITSA with HMRC. You’ll need to sign up through your software or through HMRC’s online portal. This can’t be done at the last minute — allow time for the registration to process.

- Decide whether you want a bookkeeper or accountant involved. You can handle quarterly submissions yourself, but many landlords find that having professional oversight — particularly for the end-of-year declaration — saves both time and money in the long run. Our bookkeeping service is specifically geared around this kind of ongoing rental income management.

For those in the April 2027 wave, the window for preparation is now open. Don’t mistake having another year for having plenty of time — software onboarding, historic data entry, and forming new record-keeping habits all take longer than you’d expect.

Self Assessment Isn’t Going Away — It’s Changing Shape

One misconception worth addressing: Making Tax Digital for landlords doesn’t replace Self Assessment. You’ll still file an annual declaration — it just happens within the MTD framework rather than through the traditional Self Assessment portal. The key dates for the 2025–26 Self Assessment cycle still apply to your final declaration, and the January 31st payment deadline remains firmly in place.

What MTD does change is that by the time you reach your annual declaration, the bulk of your income and expense data has already been submitted. The final stage becomes more about adjustments, claims, and confirming accuracy than a mad scramble to locate twelve months of receipts. In theory, anyway. In practice, it depends entirely on how well you’ve kept your records through the year — which loops us back to getting the right software and habits in place now.

If you’d like to understand more about your Self Assessment obligations alongside the MTD requirements, that’s a sensible thing to review alongside your MTD preparation rather than treating them as separate concerns.

Frequently Asked Questions: Making Tax Digital for Landlords

Who Actually Needs to Comply?

Does Making Tax Digital apply to landlords who only have one rental property?

It depends entirely on the gross income from that property (combined with any self-employment income). If the total exceeds the relevant threshold — £50,000 from April 2026, £30,000 from April 2027, £20,000 from April 2028 (proposed) — then yes, it applies regardless of how many properties you own. One property generating £55,000 a year in gross rent puts you in scope from April 2026.

I file a joint tax return with my spouse for our rental income. How does MTD ITSA work for us?

There’s no such thing as a joint income tax return in the UK — each individual files their own. For jointly owned property, each person reports their share of the income and expenses. If your share of the gross rental income exceeds the threshold, you’re individually in scope for MTD ITSA, regardless of what your spouse’s position is.

How the Quarterly Reporting Process Works

Will the quarterly updates change how much tax I pay?

No. The quarterly submissions are data submissions — they’re not tax payments and don’t trigger tax assessments mid-year. Your actual tax liability is still calculated and settled via your annual declaration, with payments due by 31 January and 31 July (payments on account). MTD changes the reporting process, not the tax calculation rules.

What if I make a mistake in a quarterly submission?

Corrections can be made in subsequent submissions or through the end-of-year declaration. HMRC has been reasonably clear that quarterly submissions are expected to be provisional — the final declaration is where everything gets properly reconciled. That said, deliberately submitting incorrect figures is a different matter entirely.

Landlords With More Complex Situations

I’m a landlord with properties overseas — does MTD ITSA apply to my foreign rental income?

Overseas property income is generally reported separately on your UK Self Assessment (or MTD annual declaration). The interaction between MTD ITSA and overseas income is an area where professional advice is genuinely valuable, particularly if you’re also navigating double taxation treaties. This sits neatly within the scope of tax compliance support that an accountant can provide.

Choosing Software and Whether You Need an Accountant

What software is HMRC-compatible for Making Tax Digital for landlords?

HMRC maintains an updated list of approved software providers on their website — you can check the current list at gov.uk. QuickBooks, Xero, FreeAgent, Sage, and a number of specialist landlord software packages are all developing MTD ITSA-compliant tools. The list is growing — but check directly, as compatibility can vary by tier or subscription level.

Can I still do my own Making Tax Digital submissions without an accountant?

Absolutely. If you’re comfortable with bookkeeping software and your rental income is straightforward, self-filing via MTD-compatible software is entirely feasible. Where many landlords find professional help worthwhile is in the initial setup — getting the software configured correctly, understanding which expenses to categorise how — and at year-end, where optimising allowances and planning ahead can save considerably more than the accountancy fee.

Not Sure Where You Stand With MTD? Let’s Work It Out.

The team at Ask Accountants UK Ltd works with landlords across London and beyond — from initial MTD software setup and quarterly submission management through to full Self Assessment filing, personal tax planning, and property-specific accounting advice.Get in Touch Today

📍 178 Merton High St, London SW19 1AY | 📞 020 8543 1991