Here’s something nobody tells you at dinner parties (because who discusses tax at dinner parties?): roughly 96% of UK estates won’t pay a penny in inheritance tax. Yet the 4% who do fork out an average of £180,000 to HMRC. That’s not pocket change—that’s someone’s house deposit, a comfortable retirement nest egg, or your kids’ university fees multiplied by three.

The strangest bit? Many families stumble into this tax trap purely through inaction. Their house appreciated. Savings accumulated. Suddenly, what felt like a modest middle-class estate crosses that £325,000 threshold, and boom—40% of everything above vanishes to the taxman.

I’ve spent two decades helping families navigate this minefield at Ask Accountant, and I’ll be straight with you: maximising your inheritance tax allowance isn’t about dodgy offshore schemes or complex trusts (though those have their place). It’s about understanding the rules that already exist and actually using them before it’s too late.

What’s Your Starting Point? Understanding the Nil-Rate Band

The nil-rate band—let’s call it the NRB because typing that out repeatedly gets tedious—sits at £325,000 for the 2025-26 tax year. It’s been frozen there since 2009. Yes, 2009. That’s sixteen years of house price inflation, stock market growth, and general wealth accumulation whilst this threshold hasn’t budged an inch.

Everything in your estate below this magic number? Tax-free. Everything above? HMRC takes 40%.

Quick maths: If your estate totals £525,000, that’s £200,000 over the threshold. At 40%, your beneficiaries hand over £80,000. Ouch.

But wait (and this is where it gets slightly less depressing): if you’re passing your main residence to your children or grandchildren, you might qualify for the residence nil-rate band (RNRB). That adds another £175,000 to your tax-free allowance, bringing your total to £500,000.

For married couples or civil partners, unused allowances transfer to the surviving spouse. So a couple could potentially shield up to £1 million from inheritance tax—provided they’ve planned properly and the property goes to direct descendants.

Here’s the catch that trips people up: the RNRB tapers away for estates over £2 million. For every £2 your estate exceeds this threshold, you lose £1 of the residence allowance. At £2.35 million, it disappears entirely.

Seven Years and You’re Clear: The Gift Strategy Nobody Implements

The seven-year rule sounds simple enough. Give something away, survive seven years, and it’s completely outside your estate for inheritance tax purposes. These are called Potentially Exempt Transfers (PETs), which might be the least inspiring acronym in UK tax law.

Yet most people I meet have never made a single strategic gift.

Why? Usually because they’re worried about:

- Needing the money later

- Looking like they’re giving up control

- The awkward conversation with adult children about wealth

- Whether they’ll actually make it seven years (morbid, but fair)

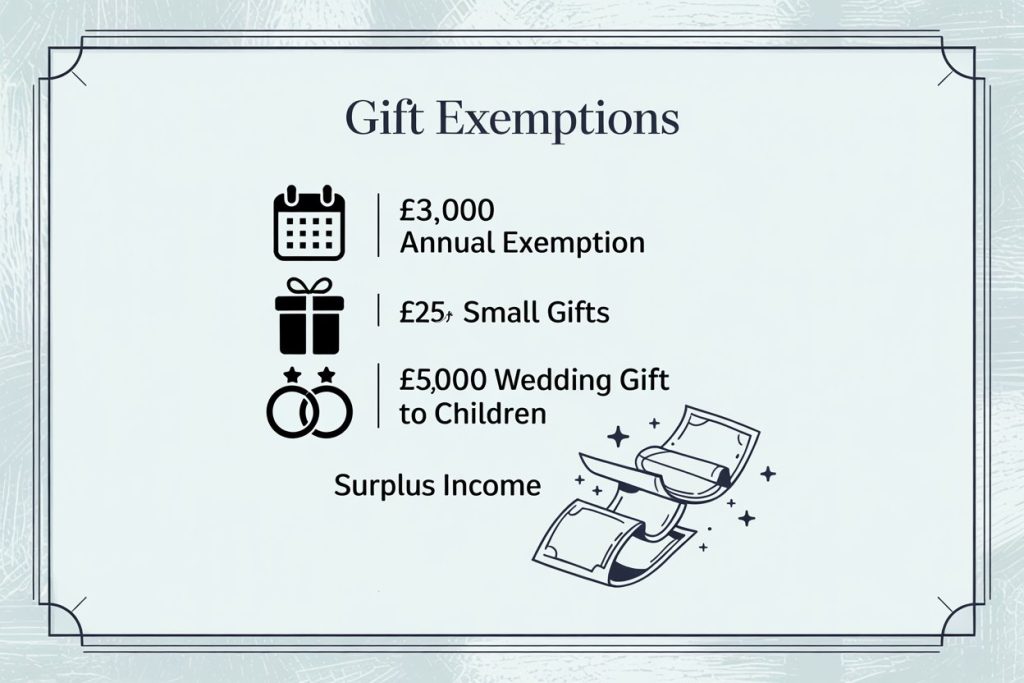

Let’s address these head-on. You don’t have to gift everything at once. You can gift incrementally. And importantly, you have annual exemptions that don’t even trigger the seven-year countdown:

- £3,000 per year to anyone (the “annual exemption”)

- £250 to as many people as you like (as long as they haven’t received your £3,000)

- Wedding gifts: £5,000 to your children, £2,500 to grandchildren, £1,000 to anyone else

- Regular gifts from surplus income (no limit, but must be truly surplus)

That last one—regular gifts from surplus income—is criminally underused. If you’ve got pension income of £50,000 annually but only need £35,000 to maintain your lifestyle, you can gift that £15,000 every year indefinitely without it ever counting toward your estate. You just need to keep meticulous records proving the pattern.

Combined, these exemptions let you shift substantial wealth out of your estate without waiting seven years or worrying about dying prematurely.

The Marriage Advantage: Doubling Your Inheritance Tax Allowance

Spouses and civil partners get extraordinary inheritance tax treatment. Everything you leave to your spouse is 100% exempt from inheritance tax, regardless of value. No limits. No questions.

Even better: any unused portion of your inheritance tax allowance transfers automatically to your surviving spouse.

Here’s how this works in practice:

| Scenario | First Death | Second Death | Tax-Free Allowance |

|---|---|---|---|

| Single person leaves estate to children | – | £500,000 (with RNRB) | £500,000 |

| Married couple, first spouse leaves everything to survivor | £0 used | Inherits both allowances | Up to £1,000,000 |

| Married couple, first spouse gifts £200,000 to children, rest to surviving spouse | £200,000 used | £800,000 remaining | £800,000 |

This transfer happens automatically. You don’t need to claim it or fill in special forms—though your executor will need to calculate it correctly.

But here’s where people mess up: they assume “leaving everything to the spouse” is always the best strategy. Sometimes it is. Sometimes it’s better to use part of the first spouse’s allowance by gifting to children or trusts at the first death, especially if the combined estate will substantially exceed £1 million.

Property: Your Biggest Asset and Your Biggest Headache

Most UK estates that hit inheritance tax do so because of property. The family home in Surrey bought for £150,000 in 1995 is now worth £800,000. Add pensions, savings, and investments, and you’re suddenly well over the threshold.

The residence nil-rate band was designed to address exactly this problem. But it comes with conditions:

- You must pass the property to direct descendants (children, stepchildren, adopted children, foster children, grandchildren)

- It only applies to your main residence

- It tapers away for estates over £2 million

That “direct descendants” requirement eliminates a lot of people. No nephew, or no best friend who’s been like family. No partner you’ve lived with for 20 years but never married. The rules are rigid.

If you’ve downsized or moved into care, there’s something called “downsizing relief” that can preserve your RNRB—but you’ll need proper documentation showing what happened to the sale proceeds.

What About Second Properties?

Here’s the thing about buy-to-let properties or holiday homes: they don’t qualify for the residence nil-rate band unless one of them was your main residence. If you own three rental properties and moved into rented accommodation yourself, tough luck—no RNRB for you.

Your executor can choose which property to designate as the main residence (assuming you lived in more than one during your lifetime), but only one property qualifies.

The Subtle Art of Spending It

There’s a brilliantly simple inheritance tax strategy that financial advisers rarely mention because it doesn’t involve their products: spend your money.

You’ve saved diligently for decades. You’ve downsized. You’re living modestly. Meanwhile, your estate creeps upward, edging toward or past the inheritance tax threshold.

At some point, you have to ask: what’s the money for?

If your kids are struggling with mortgage payments whilst you’re sitting on £600,000 in a cash ISA earning 4%, there’s a disconnect. Strategic gifting while you’re alive means you see the impact—your daughter gets her extension, your grandson gets university fees paid, your family goes on that group holiday everyone will remember.

Yes, you need to maintain enough for emergencies, care costs, and unexpected longevity. But many people overestimate what they’ll need and underestimate how much their children need support now.

The technical term for this is “dying with your boots on”—using your wealth during your lifetime rather than hoarding it for an eventual tax bill that benefits nobody except the Treasury.

Business and Agricultural Relief: The Secret Weapons

If you own a business or farmland, you might qualify for reliefs that can reduce your inheritance tax bill to zero. These are absurdly generous compared to other tax breaks:

- Business Property Relief (BPR): Up to 100% relief on qualifying business assets

- Agricultural Property Relief (APR): Up to 100% relief on qualifying agricultural property

But (and it’s a significant but), the Autumn 2024 Budget changed things. From April 2026, there’s a £1 million cap on combined APR and BPR at 100%. Above that, relief drops to 50%.

Still, 50% relief on anything over £1 million is substantially better than paying the full 40% rate.

Qualifying for these reliefs is complicated. Your business needs to be a trading business (not just investment). Your farm needs to be actively farmed. You generally need to have owned the assets for at least two years. And if you sell up before you die, the relief evaporates.

For farming families and business owners, specialist advice from firms like Ask Accountant (located at 178 Merton High St, London SW19 1AY, phone +44(0)20 8543 1991) becomes essential. Getting this wrong can cost hundreds of thousands.

Trust Structures: Not As Scary As They Sound

Trusts have a reputation for being either tax-dodging schemes for the ultra-wealthy or impenetrable legal constructs nobody understands. Neither characterisation is particularly fair.

A trust is simply a legal arrangement where you give assets to trustees to hold for the benefit of beneficiaries according to rules you set. They can be useful for:

- Protecting assets for vulnerable beneficiaries

- Maintaining control after you’ve technically given wealth away

- Reducing inheritance tax when structured correctly

- Avoiding probate delays

The inheritance tax implications depend on the type of trust. Some trusts trigger immediate tax charges. Others shelter assets completely if set up correctly.

Since April 2025, the UK has moved from a domicile-based system to a residence-based system for inheritance tax. This affects how trusts are treated, particularly for non-UK residents or those planning to leave the UK. If you’ve lived here for 10 of the last 20 years, your worldwide assets could be caught.

Trusts aren’t something you set up on a Saturday afternoon with a template from the internet. You need proper legal advice. But for estates over £1 million, they’re worth exploring.

Pensions: The Current Tax Haven (Whilst It Lasts)

Here’s a little-known fact that won’t stay true much longer: pensions currently sit outside your estate for inheritance tax purposes.

If you die with £500,000 in your pension, that’s £500,000 your beneficiaries inherit without a penny of inheritance tax. They might pay income tax on it (depending on their age and when they access it), but inheritance tax? Zero.

This makes pensions one of the most inheritance tax-efficient wrappers you can own. It’s why savvy pensioners often spend their ISAs first and leave their pensions untouched.

But—and this is crucial—this changes in April 2027. From then, inherited pensions will fall into the inheritance tax calculation.

So if you’ve been strategically maintaining a large pension pot as an inheritance planning tool, you’ve got until April 2027 to reconsider your approach.

Charitable Giving: Reduce Your Rate to 36%

If you leave at least 10% of your net estate to charity, your inheritance tax rate drops from 40% to 36%.

Let’s say your taxable estate (after all allowances) is £200,000:

- At 40%, that’s an £80,000 tax bill

- At 36%, it’s £72,000

So giving £20,000 (10% of £200,000) to charity costs your heirs only £8,000 extra. You’ve donated £20,000, but the net cost to the estate is £8,000.

| Estate Value Above Threshold | Charitable Donation (10%) | IHT at 40% | IHT at 36% (with charity) | Net Saving to Heirs |

|---|---|---|---|---|

| £200,000 | £20,000 | £80,000 | £72,000 | £8,000 |

| £500,000 | £50,000 | £200,000 | £180,000 | £20,000 |

| £1,000,000 | £100,000 | £400,000 | £360,000 | £40,000 |

Leaving at least 10% of the net estate to charity can reduce the Inheritance Tax rate from 40% to 36%, increasing the amount passed to heirs while supporting charitable causes.

Whether this makes sense depends on whether you’d have given to charity anyway. If you’re charitably inclined, it’s a remarkably efficient way to reduce your tax bill whilst supporting causes you care about.

Record Keeping: The Boring Bit That Saves Fortunes

Every time I help an executor navigate an estate, we hit the same problem: inadequate records.

Your executor needs to know:

- Every gift you made in the seven years before death

- When each gift was made

- Who received it

- What exemption you claimed (if any)

- Whether it was from surplus income

Without this documentation, HMRC assumes the worst-case scenario. That £5,000 you gave your daughter? If there’s no record of it being a wedding gift, it counts against your nil-rate band. Those monthly payments to your grandson? Without proof they came from surplus income, they’re potentially exempt transfers starting their seven-year countdown.

I recommend:

- A dedicated file (physical or digital) for all gift records

- Annual summaries of what you gave and to whom

- Bank statements highlighted to show surplus income patterns

- Letters accompanying significant gifts stating the exemption you’re claiming

- Regular reviews with your accountant

This isn’t exciting. It won’t make you feel warm inside. But it could save your estate tens of thousands in unnecessary tax.

Life Insurance: Paying the Bill Without Shrinking the Estate

If you know you’ll have an inheritance tax bill but don’t want to reduce your estate, life insurance written in trust can cover the liability.

The concept is elegant: you take out a policy for the expected tax amount, write it in trust (so it’s outside your estate), and when you die, the payout goes directly to your beneficiaries to cover the HMRC bill.

For a 65-year-old in reasonable health, insuring a £100,000 inheritance tax liability might cost £150-200 per month. That’s £2,000-2,400 annually. Over 20 years, you’d pay £40,000-48,000 to protect £100,000.

Whether that’s worthwhile depends on:

- Your health and likely longevity

- Whether you’d rather spend/gift that monthly premium

- How much you value certainty

For some families, knowing the tax is covered brings peace of mind worth more than the arithmetic suggests. For others, it’s dead money (pun intended) that could be better deployed.

Common Mistakes That Cost Families Thousands

Mistake #1: Assuming the Family Home Is Always Tax-Free

The residence nil-rate band has conditions. If you leave your house to your spouse with the plan that it eventually goes to the kids, that works. If you leave it jointly to your spouse and children, you’ve potentially messed up the RNRB for the first death.

Mistake #2: Making Gifts But Still Benefiting

The “gift with reservation” rules are brutal. If you give your house to your children but continue living there rent-free, HMRC treats it as if you still own it. Same if you gift shares but retain the dividends.

For a gift to count, you must genuinely give up benefit and control. If you’re giving away property but want to keep living there, you need to either pay market rent or structure it properly through co-ownership arrangements.

Mistake #3: Leaving It Too Late

I’ve met countless people in their early 80s who suddenly realise they should have started gifting a decade earlier. The seven-year clock doesn’t care about your good intentions.

Start planning in your 60s, not your 80s. Start gifting when you can afford to, not when you think you’re about to die.

Mistake #4: DIY Estate Planning for Complex Situations

If your estate is straightforward—a house, some savings, standard family—you can probably handle the basics yourself with decent guidance. If you’ve got business assets, multiple properties, trusts, or a complicated family situation (second marriages, estranged children, vulnerable beneficiaries), you need professional help.

The Ask Accountant team specialises in inheritance tax and estate planning advice. Ring them on +44(0)20 8543 1991 or visit their office in Merton (178 Merton High St, London SW19 1AY) before you make costly errors.

The 2025-2030 Freeze: Why Now Matters More Than Ever

The nil-rate band and residence nil-rate band are frozen until at least 2030. Five more years of inflation, house price growth, and wealth accumulation with no increase in the tax-free threshold.

This “fiscal drag” means more estates will be caught by inheritance tax without changing anything. Your estate might be £400,000 today—safely under the threshold. In five years, with normal growth, it could be £550,000. Suddenly you’ve got a £90,000 inheritance tax bill you didn’t plan for.

The window for action is now. Use your annual exemptions. Start the seven-year clock on larger gifts. Review your will. Consider whether life insurance or trusts make sense.

Doing nothing is a decision—usually an expensive one.

FAQ: Your Inheritance Tax Allowance Questions Answered

How much can I inherit without paying tax in 2025?

You can inherit up to £325,000 from anyone tax-free (the nil-rate band). If you’re inheriting your parents’ main home and they’ve left it to you as a direct descendant, that increases to £500,000 per person. For a married couple, the combined allowance can reach £1 million. Anything above these thresholds is taxed at 40%.

Can I give my son £100,000 UK tax-free?

Yes, you can give your son £100,000 without immediate tax consequences. However, it becomes a Potentially Exempt Transfer (PET). If you survive for seven years after making the gift, it’s completely tax-free. If you die within seven years, it counts toward your estate for inheritance tax calculations. You can reduce this by using your annual £3,000 exemption first.

How much money can be legally given to a family member as a gift UK?

There’s no legal limit on how much you can gift. However, gifts over £3,000 per year (outside of specific exemptions like wedding gifts) are PETs and only become fully tax-free if you survive seven years. You can also make unlimited gifts from surplus income without triggering the seven-year rule, provided you can prove they don’t affect your standard of living.

What is the 7-year rule for inheritance tax?

The seven-year rule states that gifts made more than seven years before your death are completely exempt from inheritance tax. If you die within seven years, the gift is added back into your estate. However, “taper relief” reduces the tax on gifts made between 3-7 years before death. Gifts made within three years are taxed at the full 40% rate.

Do I need to tell HMRC if someone gives me money?

As the recipient of a cash gift, you don’t need to inform HMRC. The responsibility falls on the executor of the giver’s estate to report gifts made within seven years of death when calculating inheritance tax. Keep records of large gifts received, including dates and amounts, as this helps executors later.

How can married couples use their inheritance tax allowance?

Married couples can transfer unused allowances to the surviving spouse. If the first spouse leaves everything to the survivor, their full allowance (£325,000 plus potentially £175,000 residence nil-rate band) transfers automatically. This means the surviving spouse could have up to £1 million in combined tax-free allowances when they eventually pass away.

Does the residence nil-rate band apply to rental properties?

No. The residence nil-rate band only applies to your main residence, which must be left to direct descendants (children, stepchildren, adopted children, foster children, or grandchildren). Buy-to-let properties and second homes don’t qualify unless one of them was your main residence at some point.

Can I avoid inheritance tax by spending my money?

Absolutely. Money you spend during your lifetime isn’t part of your estate when you die. If inheritance tax is a concern and you’ve got more than enough to live comfortably, strategic spending—whether on yourself, helping family members now, or experiences you’ll all remember—reduces your estate naturally. Just make sure you keep enough for care costs and emergencies.

What happens to my pension when I die?

Currently, pensions sit outside your estate for inheritance tax purposes. However, this changes from April 2027, when inherited pensions will be included in inheritance tax calculations. If you have a substantial pension pot and inheritance tax concerns, review your strategy before 2027.

Should I set up a trust for inheritance tax planning?

Trusts can be valuable tools for inheritance tax planning, particularly for estates over £1 million, vulnerable beneficiaries, or complex family situations. However, they’re not suitable for everyone and come with their own tax implications and costs. Speak with a specialist—Ask Accountant’s team can review your specific circumstances and recommend whether a trust makes sense for you.

Where to Go From Here

Maximising your inheritance tax allowance isn’t a one-time task you tick off a list. Your estate value changes. Tax rules evolve. Family circumstances shift.

What matters is having a plan and reviewing it regularly—ideally every 2-3 years, or whenever something significant changes (marriage, divorce, property purchase, business sale, inheritance received).

Start with the basics:

- Calculate your current estate value

- Understand which allowances apply to you

- Use your annual gifting exemptions

- Keep meticulous records

- Review your will

For estates approaching or exceeding the inheritance tax threshold, professional advice isn’t a luxury—it’s an investment that typically pays for itself many times over.

The team at Ask Accountant in London (call +44(0)20 8543 1991 or visit us at 178 Merton High St, London SW19 1AY) specialises in inheritance tax planning, business advice, and proactive tax advisory solutions. We help families across the UK protect their wealth legally and efficiently.

Your legacy shouldn’t be a surprise tax bill. With the right planning, your inheritance tax allowance becomes a powerful tool for passing wealth to the people who matter most—on your terms, in your timeline.