So — who needs to follow Making Tax Digital rules? If you’re self-employed, a landlord, or run any VAT-registered business in the UK, the short answer is: probably you, sooner than you think. Making Tax Digital (MTD) is HMRC’s push to digitalise the entire UK tax system. The deadlines are real, the penalties are real, and the window to prepare is shrinking. This guide breaks down exactly who falls under MTD, when the rules kick in, and what you actually need to do about it.

There’s a particular kind of dread that hits when HMRC sends something through the post. The envelope just looks ominous — official, slightly beige, indifferent to whatever you had planned for Tuesday. MTD has been producing that dread in waves since 2019, mostly because the rollout was staggered. The rules shifted, the deadlines moved, and a fair few people just hoped the whole thing might quietly go away.

It hasn’t.

Who Needs to Follow Making Tax Digital for VAT?

If you run a VAT-registered business with taxable turnover above £90,000 (the current registration threshold), MTD for VAT has applied to you since April 2019. Voluntarily registered businesses — those below the threshold who chose to register anyway — were pulled in from April 2022.

So if you file VAT returns through compatible software and keep digital records of your VAT transactions, you already follow Making Tax Digital rules — whether you thought of it that way or not. The VAT phase is, broadly speaking, the settled chapter of this story. The chapters still being written are the ones that matter most right now.

Who Needs to Follow Making Tax Digital for Income Tax?

This is where things get genuinely disruptive for a large chunk of the UK’s working population. Making Tax Digital for Income Tax Self Assessment (MTD ITSA) is the next major wave — and it’s coming fast.

Here’s the core of it:

- From April 2026: Self-employed people and landlords with combined qualifying income above £50,000 must follow Making Tax Digital rules for income tax.

- From April 2027: The threshold drops to £30,000.

- From April 2028: A further planned drop to £20,000 — pulling in a very significant proportion of sole traders and landlords across the country.

(External reference: HMRC’s official MTD for Income Tax guidance)

What does following Making Tax Digital rules actually mean in practice for income tax?

- Keep digital records of income and expenses through HMRC-recognised software.

- Submit quarterly updates to HMRC — four times a year instead of the once-a-year Self Assessment return.

- File an end-of-period statement at the close of each tax year.

- Submit a final declaration confirming your overall tax position — this replaces the traditional Self Assessment return.

It’s a fundamental shift in how tax reporting works. Not just a new form to fill in, but a completely different rhythm and system.

Self-Employed? Here’s Exactly When MTD ITSA Applies to You

For MTD income tax purposes, self-employment means income from a trade, profession, or vocation reported on a Self Assessment tax return. That includes:

- Sole traders across every industry — builders, consultants, freelancers, therapists, market traders

- People with multiple self-employed income streams, where HMRC combines all figures for threshold purposes

It does not include employment income (PAYE) or limited company dividends — those fall under different tax machinery entirely.

Partners in business partnerships face a separate future phase, which HMRC has not yet given a firm date for.

Landlords: Who Needs to Follow Making Tax Digital Rules Here?

If you own rental property and receive income from it, you count as a landlord for MTD purposes — even if you don’t think of yourself that way. The retired schoolteacher who inherited a flat and rents it out? Caught by these rules once rental income crosses the relevant threshold. The young professional who kept their first flat after moving in with a partner? Same story.

Rental income from UK or overseas property counts toward the qualifying income threshold. If your combined self-employment and rental income exceeds £50,000 from April 2026 (dropping to £30,000 in 2027, then £20,000 in 2028), Making Tax Digital rules apply to you.

The team at Ask Accountants UK Ltd works with landlords across London — many of whom were genuinely surprised to learn MTD applied to them. Their property accounting services address MTD compliance for rental income directly, which gives landlords one less thing to lie awake worrying about.

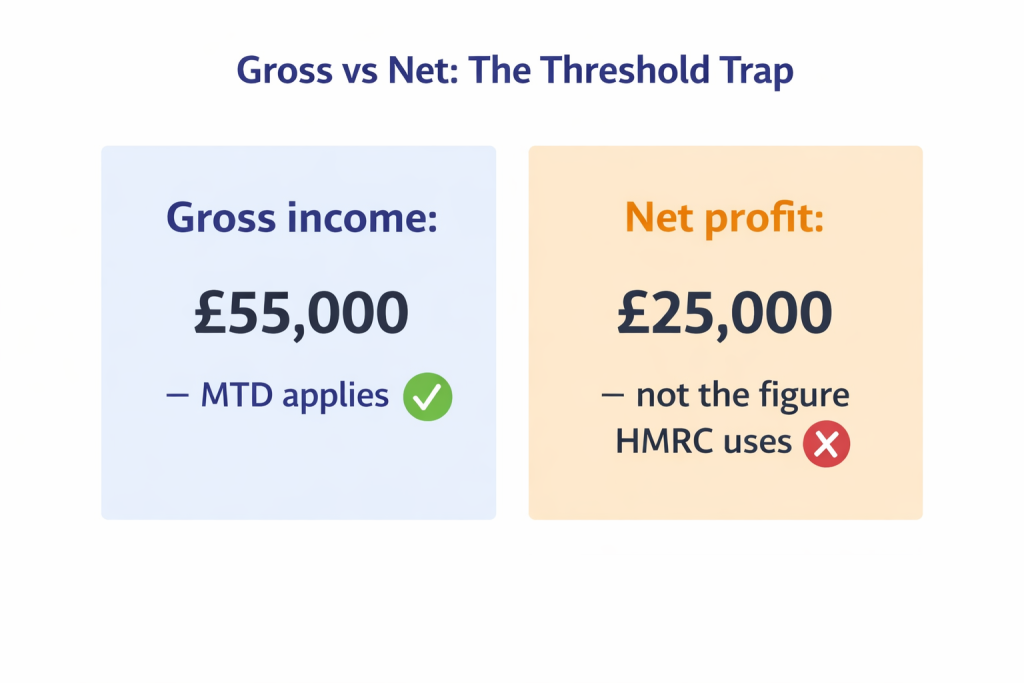

What “Qualifying Income” Actually Means — Don’t Get This Wrong

This confuses people regularly. Qualifying income for MTD ITSA purposes means gross income — not profit, not net income after expenses.

Say your rental property brings in £45,000 in rent but costs you £30,000 in mortgage interest, maintenance, and agent fees. Your qualifying income is still £45,000. A freelance consultant with a turnover of £55,000 and expenses of £20,000 still has qualifying income of £55,000 — well above the initial threshold.

Many people look at their profit and assume they sit safely below the threshold, when their gross income puts them squarely in scope. Don’t make that mistake.

The Making Tax Digital Rules Timeline: At a Glance

| Phase | Start Date | Who Is Affected | Income Threshold |

|---|---|---|---|

| MTD for VAT | April 2019 | VAT-registered businesses above threshold | £90,000 taxable turnover |

| MTD for VAT (extended) | April 2022 | All VAT-registered businesses | All voluntary VAT registrations |

| MTD for Income Tax (Phase 1) | April 2026 | Self-employed & landlords | Qualifying income >£50,000 |

| MTD for Income Tax (Phase 2) | April 2027 | Self-employed & landlords | Qualifying income >£30,000 |

| MTD for Income Tax (Phase 3) | April 2028 | Self-employed & landlords | Qualifying income >£20,000 |

Who Is Currently Exempt from Making Tax Digital?

MTD for Income Tax doesn’t apply to everyone yet — and some groups hold specific exemptions:

- Partnerships: Not included in the current rollout. HMRC has signalled they will be added eventually, but no firm date exists yet.

- Trusts and estates: Currently excluded.

- People below the income thresholds: If your qualifying income sits under £50,000 in 2026, you aren’t yet mandated — though you may be by 2028 if the £20,000 threshold holds.

- Those with digital exclusion exemptions: HMRC grants exemptions to people who genuinely cannot use digital tools — due to age, disability, remote location, or religious reasons. These assessments happen case by case.

- Limited companies: MTD for Corporation Tax has no confirmed mandation date. Limited companies still file Corporation Tax returns through a different process.

⚠️ A note on exemptions: Being currently exempt is not the same as being permanently exempt. HMRC’s stated ambition is a fully digital tax system. The thresholds will fall. Planning now costs far less than scrambling later.

Making Tax Digital Rules Day-to-Day: What Does Compliance Look Like?

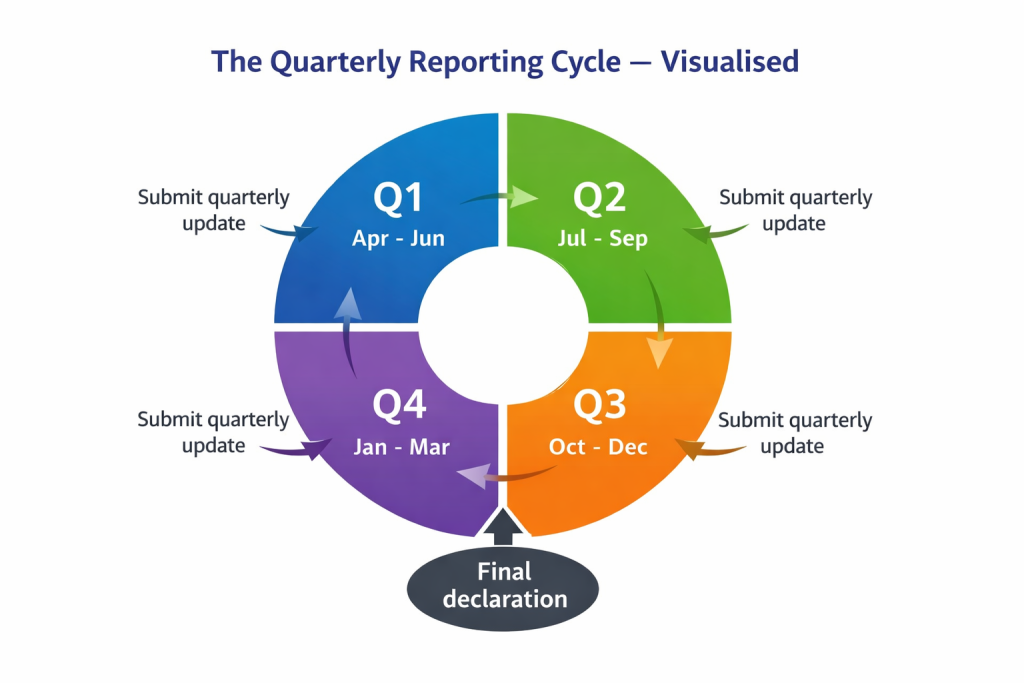

Say you’re a self-employed graphic designer earning £60,000 a year. Under MTD ITSA from April 2026, your tax life changes like this.

Instead of doing one big annual tax return in January (often with mild panic), you submit four quarterly updates to HMRC throughout the year. These are summaries of income and expenses for each quarter. They aren’t tax payments — they’re updates to keep HMRC informed of where things stand. Your actual tax liability still gets calculated annually.

At the end of the tax year, you confirm and finalise everything with a final declaration. The quarterly submissions are more about regular visibility than a fundamentally new tax burden. That said — the administrative burden is real. Four submissions instead of one, year-round record-keeping, compatible software — the lot.

This is where cloud accounting becomes less of a nice-to-have and more of a practical necessity. Platforms like QuickBooks, Xero, and FreeAgent handle MTD-compliant record-keeping and submissions. Manual spreadsheets won’t cut it for quarterly reporting at scale — especially when HMRC requires records that digital software maintains and submits via approved channels. Read more: how cloud accounting works and why it saves time.

Choosing the Right Software When Making Tax Digital Rules Apply

Not all accounting software is MTD-compatible — and this trips people up. HMRC maintains a list of recognised providers, but choosing the right one depends on your industry, transaction volume, whether you employ staff, and how comfortable you are with technology.

The bookkeeping service at Ask Accountants UK Ltd runs on MTD-ready systems. Clients get the compliance piece handled alongside the day-to-day numbers — rather than discovering in March that their records aren’t in the right format.

(External: HMRC’s approved MTD software list)

Who Doesn’t Need to Worry Right Now — But Should Still Pay Attention

Let’s be direct. If you are:

- A PAYE employee with no other income — MTD doesn’t affect you. Your employer handles your tax through payroll.

- A limited company director — You pay yourself through PAYE and/or dividends. Your company’s Corporation Tax is a separate matter, and MTD for Corporation Tax has no confirmed date yet.

- Self-employed but earning under £20,000 — The current plans stop at that threshold. Whether HMRC ever pushes below £20,000 remains unclear.

- Retired with pension income only — Pension income doesn’t count as qualifying income for MTD purposes.

That said — if you file a self-assessment for any reason, building good digital record-keeping habits now serves you well regardless of where thresholds eventually land.

What Happens If You Don’t Follow Making Tax Digital Rules?

HMRC runs a points-based penalty system for MTD. Miss a quarterly submission deadline — you collect a penalty point. Accumulate enough points and financial penalties kick in. The exact structure varies depending on how frequently HMRC requires submissions, but repeated non-compliance adds up, literally.

Beyond the penalty points, irregular or missing quarterly data draws attention. MTD makes HMRC’s data analysis more efficient — which also means anomalies show up faster. See HMRC Tax Investigations: Complete Guide for context on how these situations typically unfold, and HMRC investigations support if you need professional backup.

(External: Gov.uk — HMRC late submission penalties)

Different Business Types: A Making Tax Digital Rules Comparison

| Business Type | MTD for VAT | MTD for Income Tax | MTD for Corp Tax | Notes |

|---|---|---|---|---|

| Sole trader (VAT-registered) | ✅ Now | ✅ From 2026/27/28 | ❌ N/A | Threshold dependent |

| Sole trader (not VAT-registered) | ❌ N/A | ✅ From 2026/27/28 | ❌ N/A | Threshold dependent |

| Landlord | If VAT-registered | ✅ From 2026/27/28 | ❌ N/A | Gross rental income counts |

| Limited company | ✅ Now | ❌ N/A | ⏳ TBC (no date set) | Directors may still need MTD ITSA personally |

| Partnership | If VAT-registered | ⏳ Future phase | ❌ N/A | Timeline not yet confirmed |

| PAYE employee only | ❌ N/A | ❌ Not required | ❌ N/A | Tax handled through payroll |

The Director Nuance: Making Tax Digital Rules Can Still Catch You

Here’s something that surprises many limited company directors. Even if your company faces no MTD Corporation Tax obligation yet, you personally may still need to follow Making Tax Digital rules. How? If you receive rental income alongside your director’s salary and dividends, and that rental income exceeds the relevant threshold — Making Tax Digital for Income Tax applies to you as an individual. The corporate structure doesn’t shield your personal tax position.

This is exactly the kind of situation that benefits from proper personal tax planning. The rules aren’t designed to catch people out — they’re just genuinely complex when multiple income sources come into play.

Frequently Asked Questions About Making Tax Digital Rules

Q: I’m self-employed with income of £55,000 but my profit is only £25,000. Do Making Tax Digital rules apply to me from April 2026?

Yes. The threshold uses gross qualifying income — your turnover of £55,000, not your profit of £25,000. Making Tax Digital rules apply to you from April 2026.

Q: I have two buy-to-let properties earning £28,000 combined. Do I need to follow Making Tax Digital rules?

Not from April 2026, as you sit below the £50,000 threshold at that stage. However, the threshold drops to £30,000 in April 2027 — and if rents increase or you acquire more property, you could enter scope by then. From April 2028, the planned threshold of £20,000 would bring you in regardless.

Q: My business is a limited company. Do Making Tax Digital rules apply to my VAT returns?

Yes — if your company is VAT-registered, MTD for VAT already applies. File VAT returns through compatible software and keep digital records of VAT transactions. Tax compliance services can help bring things up to standard if you’ve fallen behind.

Q: Can I use a spreadsheet for MTD records?

Technically yes — but it requires “bridging software” to connect your spreadsheet to HMRC’s systems for submission. It’s a workaround, not a clean solution, and it adds unnecessary complexity. Dedicated MTD-compatible accounting software is simpler, more reliable, and often cheaper than people assume.

Q: What if I genuinely cannot use digital tools?

HMRC operates an exemption process for digital exclusion. This targets people who genuinely cannot engage with digital technology — older people without internet access, those with certain problems, or people in remote areas with unreliable connectivity.

Q: I’m not sure whether my income exceeds the MTD threshold. How do I check?

Look at your most recent Self Assessment tax return. Your qualifying income for MTD purposes is the gross income from self-employment and/or rental property — the figures before expenses. If those combined gross figures cross £50,000, Making Tax Digital rules apply to you from April 2026. The self-assessment service at Ask Accountants can review your position. Also check the 2025-26 self-assessment key dates for important planning milestones.

Who Needs to Follow Making Tax Digital Rules: The Honest Summary

The history of MTD is, admittedly, a history of delayed deadlines and shifted goalposts. Reasonable people looked at the original timelines and thought: if I just wait long enough, this might not happen. That’s no longer a sensible bet. The VAT phase runs fully live. The income tax phase is legislated and approaching. HMRC has invested heavily in the infrastructure.

Who needs to follow Making Tax Digital rules? More people, every year — with thresholds falling in steps until a very large proportion of self-employed people and landlords are included. If you sit anywhere near those numbers, getting your records, software, and professional support sorted now makes more sense than a last-minute scramble.

For proper guidance on MTD readiness — whether that’s cloud accounting setup, bookkeeping, or a full review of your tax compliance position — the team at Ask Accountants UK Ltd is at 178 Merton High St, London SW19 1AY. Call 020 8543 1991 or visit askaccountantsukltd.co.uk.