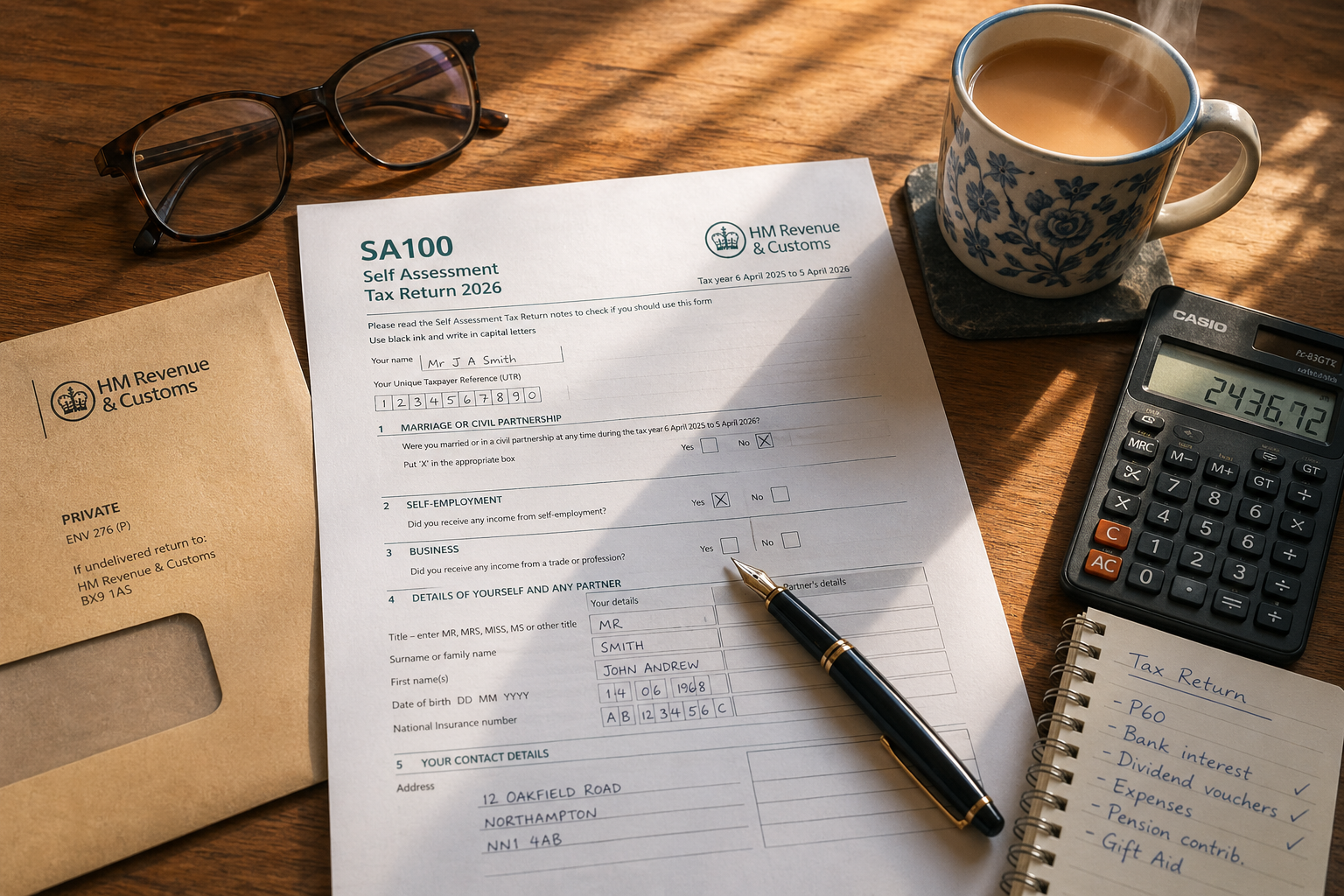

There is a particular flavour of dread that lives inside a brown HMRC envelope. You know the one. It lands on the doormat sometime around late spring, looking very polite and very official, and your stomach does that small, ungenerous flip. Right, you think. Tax return season again.

If that’s where you are right now — or where you’ll be in a few months — let’s make this less awful than it has to be. The SA100 form 2026 covers the 2025/26 tax year (income earned between 6 April 2025 and 5 April 2026), and despite its reputation, it is genuinely doable on your own. You need patience, a working calculator, and the willingness to read the small print twice. Three times if you’re like me.

I run through this every year for clients at Ask Accountants UK Ltd, and the pattern is always the same: people don’t struggle because the form is impossibly hard. They struggle because nobody ever explained which bits actually apply to them. So that’s what I want to do here — strip the form down to its useful parts and tell you what’s worth your attention.

So what actually is the SA100?

Eight pages. That’s it. Eight pages of questions HMRC uses to work out whether you’ve paid the right amount of tax for the year. The SA100 form 2026 is the main return — the spine of the whole Self Assessment process — and everything else (we’ll get to those bewildering “SA1-something” pages in a minute) bolts onto it.

You’ll need it if you fall into any of these camps:

- Self-employed sole trader earning more than £1,000 (gross, before expenses) in 2025/26

- A landlord taking rental income over £1,000

- A company director, generally

- Anyone with untaxed income over £2,500 — savings, dividends, foreign income, the lot

- High earners pulling in more than £100,000

- Families caught by the High Income Child Benefit Charge (kicks in at £60,000 of adjusted net income)

- Anyone with capital gains above the £3,000 annual exempt amount for 2025/26

Quick reality check: roughly 12 million people file a Self Assessment each year in the UK. You’re not alone, and you’re definitely not being singled out.

💡 A small mercy worth knowing: If you’re filing online and you owe less than £3,000, HMRC can collect it automatically through your tax code in the 2027/28 year. You’ll need to file by 30 December 2026 to qualify. It softens the January cash-flow blow considerably.

The dates that actually matter

Miss these and HMRC starts charging you for the privilege. I’m not joking — there’s a £100 penalty the moment you slip past the online deadline, regardless of whether you owe a penny.

| Deadline | What’s Due | Tax Year |

|---|---|---|

| 5 October 2026 | Register for Self Assessment (first-time filers only) | 2025/26 |

| 31 October 2026 | Paper SA100 must arrive at HMRC | 2025/26 |

| 30 December 2026 | Online filing if you want tax under £3,000 collected via PAYE code | 2025/26 |

| 31 January 2027 | Online return + balancing payment + first payment on account | 2025/26 + 2026/27 |

| 31 July 2027 | Second payment on account | 2026/27 |

For a more granular breakdown, our 2025/26 Self Assessment key dates guide has the full calendar with reminders.

Before you touch the form: gather the paperwork

Half the time people get stuck on the SA100 form 2026, it’s because they’re trying to fill it in without the right documents to hand. Don’t do that to yourself.

Pull together:

- Your Unique Taxpayer Reference (UTR) — that 10-digit number HMRC issues

- National Insurance number

- P60 if you’re employed (or P45 if you left a job mid-year)

- P11D for benefits in kind

- All invoices and bank statements if you’re self-employed

- Rental statements if you’re a landlord

- Dividend vouchers and savings interest certificates

- Records of any Gift Aid donations and pension contributions

- Records of capital disposals — sales of shares, second properties, that sort of thing

A boring tip that has saved my clients more times than I can count: scan everything as you go through the year. A shoebox of crumpled receipts in March is nobody’s friend.

Walking through the SA100 itself

The form is divided into ten roughly logical sections, and you only fill in the boxes that actually apply to you. The rest you leave blank. (Tempting though it is to put zeros everywhere — please don’t, it confuses the processing system.)

Page TR1 — Who you are. Date of birth, name, address, NI number, phone. Slightly dull. Get it right anyway, because misspelt names and old addresses are a surprisingly common reason returns get held up.

Page TR2 — What kind of income did you have? Tick boxes for employment, self-employment, partnership, UK property, foreign income, trusts, capital gains, residence questions. Each tick triggers a corresponding supplementary page (more on those in a moment). If you’re filing online, the system simply asks you these questions and unfolds the relevant sections — far less faffing than the paper version.

Page TR3 — Income. UK interest from banks and building societies, UK dividends, UK pensions, state pension, taxed and untaxed income from various sources. Be careful with savings interest: only what exceeds your Personal Savings Allowance gets taxed, but you still report the gross amount.

Page TR4 — Tax reliefs. Pension contributions (the relief at source ones, mainly), Gift Aid, blind person’s allowance. Don’t sleep on Gift Aid if you’re a higher-rate taxpayer — you can claim back the difference between the basic rate already given to the charity and your higher rate. People miss this constantly.

Page TR5 — Other information. Marriage Allowance transfer, student loans, High Income Child Benefit Charge. The Child Benefit charge is one of those quiet tax traps — for every £200 of adjusted net income above £60,000, you pay back 1% of the benefit, until it’s fully clawed back at £80,000.

Page TR6 — Finishing up. Underpaid or overpaid tax from previous years, refund details, declaration. Sign here. Mean it.

Now, those supplementary pages

This is where things get specific. Think of the SA100 as the main course and the supplementary pages as the side dishes you only order if you fancy them.

| Form | Who Needs It |

|---|---|

| SA101 | Less common income, deductions and reliefs (EIS, SEIS, VCT investments) |

| SA102 | Employees and company directors — one per job |

| SA103S | Self-employed with turnover under £90,000 (short version) |

| SA103F | Self-employed with turnover above £90,000 (full version) |

| SA104S / SA104F | Business partnerships (short / full) |

| SA105 | UK rental property income |

| SA106 | Foreign income or claiming foreign tax credit relief |

| SA107 | Income from trusts, settlements, deceased estates |

| SA108 | Capital Gains Tax — share sales, property sales, etc. |

| SA109 | Non-UK residents and dual residents |

| SA110 | Tax calculation summary (only if you’re working out your own tax) |

Most filers I see only need a couple of these. A self-employed plumber filing for 2025/26 typically uses just SA100 + SA103S. A landlord with one buy-to-let needs SA100 + SA105. Add an employed job on top and SA102 joins the party.

Filing online is genuinely better, by the way. Roughly 97% of returns now go that route, and HMRC’s online system silently does the supplementary-page selection for you based on the questions it asks. No need to download SA105 separately or anything like that.

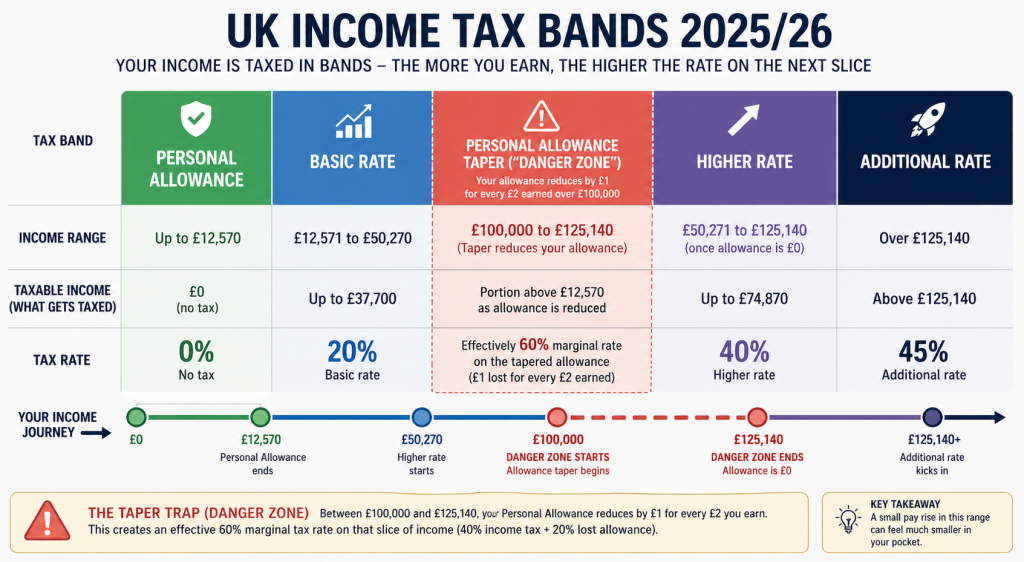

What the numbers look like for 2025/26

The rates haven’t moved much from 2024/25 — Personal Allowance is frozen at £12,570, which means more and more people are being dragged into higher tax bands as wages rise. Fiscal drag, the Treasury’s quiet little revenue raiser.

| Band | Income Range | Income Tax Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 – £50,270 | 20% |

| Higher Rate | £50,271 – £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

The Personal Allowance starts tapering once your income passes £100,000 — losing £1 for every £2 above the threshold, until it disappears entirely at £125,140. This creates an effective marginal rate of 60% in that band, which is why pension contributions and Gift Aid become so attractive for high earners. Our team explores this regularly through personal tax planning work.

Dividends sit on a separate scale: £500 dividend allowance, then 8.75% / 33.75% / 39.35% depending on your tax band.

For the self-employed, Class 2 National Insurance has been abolished from 2024/25 onwards (you can still pay it voluntarily to protect benefit entitlements). Class 4 NI runs at 6% between £12,570 and £50,270, then 2% above that. Worth noting — the self-assessment tax rates guide has more depth here.

Penalties — and why I beg you to file early

Late filing penalties stack up like Lego bricks, each one snapping onto the last:

- Day after deadline: £100 fixed penalty. Automatic. No tax owed? Doesn’t matter, you still pay.

- 3 months late: £10 per day, up to 90 days. That’s potentially £900 just for procrastination.

- 6 months late: Another 5% of tax due, or £300 — whichever is greater.

- 12 months late: Same again. In serious cases, more.

And that’s just the filing side. Late payment attracts its own family of charges: 5% surcharge at 30 days, 6 months and 12 months, plus daily interest at the Bank of England base rate plus 2.5%. At current levels, that’s roughly 7%-plus per annum on whatever you owe.

⚠️ The unglamorous truth: “I didn’t know” is not a reasonable excuse. Neither is “I found it complicated” or “my accountant didn’t file it for me.” HMRC’s appeals team has heard them all and remains spectacularly unimpressed.

Making Tax Digital — the change rumbling toward us

Worth flagging before we wrap up. From April 2026, Making Tax Digital for Income Tax Self Assessment (MTD for ITSA) begins its phased rollout. If you’re self-employed or a landlord with combined gross income over £50,000, you’ll need to:

- Keep digital records

- Submit quarterly updates to HMRC through MTD-compatible software

- File a final declaration after year-end

This isn’t replacing the SA100 immediately for most people, but it’s the direction of travel. The £30,000 threshold rolls in from April 2027, and £20,000 by April 2028. If you’re in scope, switching to cloud accounting now rather than scrambling later is the sensible move.

Common mistakes — the ones I see again and again

Honestly, after years of cleaning up returns, the same handful of errors crop up:

- Putting employed P60 figures in the self-employed boxes. Different page entirely.

- Forgetting to declare interest from “small” savings accounts. Even £40 of taxable interest needs to go on the form if it’s over your allowance.

- Claiming expenses that aren’t “wholly and exclusively” for business purposes. The smart suit you wear to client meetings? Not allowable. Sorry.

- Missing the dividend allowance reduction. It dropped to £500 for 2024/25 onwards — much smaller than people remember.

- Ignoring payments on account when calculating what’s due. They’re not extra; they’re advance instalments toward next year’s bill.

- Filing without the right supplementary pages. Then HMRC rejects it and the clock keeps ticking.

If any of this is making your eye twitch, that’s normal. The form is workable if you have the patience for it, but it isn’t designed to be intuitive. There’s a reason a lot of people use HMRC’s official guidance notes alongside the form itself — they fill in the gaps the form doesn’t explain.

When it might be worth handing it over

Look, I’m an accountant — of course I’m going to suggest accountants are useful. But I’ll be honest about when it actually pays to bring one in:

- You’ve got more than two income streams (employment + freelance + rental, say)

- You hit the £100k tapering trap

- You’ve sold a property or significant investment

- You’re a director with dividends and a salary mix

- You’ve got foreign income or you’re navigating residence rules

- You’re behind on previous returns (HMRC compliance gets complicated quickly)

- You’ve received an enquiry letter

For straightforward returns — one PAYE job, a bit of side hustle income — many people manage perfectly well on their own. For the messier cases, the cost of professional help usually pays for itself in time saved, mistakes avoided, and reliefs identified that you’d never have spotted. Our Self Assessment service handles everything from a basic SA100 to genuinely complex multi-source returns, and we’re based at 178 Merton High St in Wimbledon if you’d rather speak in person — give us a ring on 020 8543 1991 if you’d like to chat through your situation.

If you’re a CIS subcontractor specifically, by the way — the SA100 is your route to claiming back overpaid CIS deductions, and our CIS refund team handles those routinely.

Final thoughts

The SA100 form 2026 isn’t the monster it pretends to be. It’s a structured questionnaire with strict deadlines and unforgiving penalties, but the questions themselves are mostly answerable if you’ve kept reasonable records and you’re willing to go slowly through the form. File early. Keep evidence of everything for at least six years (HMRC can ask). And if it gets to mid-January and you’re still staring at a blank screen, get help — that £100 penalty is steeper than most accountants’ first-hour rate.

The 31 January 2027 deadline will arrive whether you’re ready or not. Better to meet it on your terms.

Frequently Asked Questions

What is the SA100 form 2026 used for? It’s the main Self Assessment tax return for individuals, used to report all taxable income and gains for the 2025/26 tax year (6 April 2025 to 5 April 2026) to HMRC.

Where can I download the SA100 form 2026? Directly from GOV.UK on the official Self Assessment page. Bear in mind that filing online is faster, and the system handles supplementary pages automatically.

Do I have to use a paper SA100? No — and most people don’t. About 97% of taxpayers file online via the HMRC Government Gateway. Paper is allowed but the deadline is three months earlier (31 October 2026 vs 31 January 2027).

What happens if I miss the SA100 deadline? Automatic £100 penalty on day one, then daily fines after three months, plus extra percentage-based penalties at six and twelve months. Interest accrues on unpaid tax separately.

Can I amend my SA100 form 2026 after submitting? Yes. You have until 31 January 2028 to amend the 2025/26 return. Changes are made through your Government Gateway account or by writing to HMRC.

Do I need an accountant to file the SA100? No, but for complex situations — multiple income streams, capital gains, foreign income, high earnings — professional help often saves more than it costs. For straightforward returns, doing it yourself is perfectly reasonable.

What’s the £1,000 trading allowance? If your gross self-employment or property income is under £1,000 in the tax year, you don’t need to file at all (with some exceptions). Above £1,000, the SA100 (plus relevant supplementary pages) is required.