The UK inheritance tax nil rate band 2026 still sits at £325,000 — exactly where it landed back in April 2009. Seventeen years. No rise. While average UK house prices have roughly doubled in that window, the threshold has stayed politely still, like a guest who arrived early and refuses to leave. And that frozen figure is doing more damage to ordinary families than any headline tax rate rise ever could.

If that sounds like a stealth tax, well… that’s because it is. The Treasury doesn’t need to raise rates when inflation is doing the job for them. A modest family home in much of the South East now breaches £325,000 on its own, before anyone’s even counted the savings account, the ISA, or the slightly embarrassing collection of stamps in the loft.

So here’s what we’re going to unpack together: where the thresholds sit, who’s genuinely caught in the net, how the rules bend for married couples and for anyone passing a home to their children, and what the 2025 Autumn Budget changed for 2026 and the years beyond. I’ll mention Ask Accountants UK Ltd where it’s actually useful — not because I’m trying to sell you anything, but because this stuff trips people up constantly, and we’ve cleaned up more than a few messes over the years.

How the UK inheritance tax nil rate band 2026 actually works

Two allowances. That’s the foundation of the whole system.

The first is the standard nil rate band (NRB) of £325,000 per person. Frozen. Still frozen. Now frozen until April 2031, following Chancellor Rachel Reeves’s November 2025 Budget announcement — an extension of a freeze that was already in place from earlier Finance Acts. You can verify the current rates directly on GOV.UK’s inheritance tax page.

The second is the residence nil rate band (RNRB) of £175,000 per person, which you only get if you leave a qualifying home to direct descendants (children, grandchildren, stepchildren, adopted children — nieces and nephews, sadly, don’t count).

Stack them together and a single homeowner passing their house to the kids can shelter up to £500,000. A married couple or civil partnership? Up to £1 million combined, because unused allowances are transferable between spouses. That’s the headline the government likes you to remember. It’s also the headline that ignores an awful lot of fiddly reality — which we’ll get to.

| Allowance | Amount per person (2026/27) | When it applies | Frozen until |

|---|---|---|---|

| Nil Rate Band (NRB) | £325,000 | Any estate, any beneficiary | 5 April 2031 |

| Residence Nil Rate Band (RNRB) | £175,000 | Main home → direct descendants | 5 April 2031 |

| Combined (single homeowner) | £500,000 | Must leave qualifying home to lineal heirs | 5 April 2031 |

| Combined (married / civil partners) | Up to £1,000,000 | Both allowances transferred, both used | 5 April 2031 |

| Standard IHT rate | 40% | On the slice above the combined thresholds | — |

| Reduced charity rate | 36% | If 10%+ of net estate goes to charity | — |

So who actually writes a cheque to HMRC?

Far fewer people than you’d think from the headlines.

The most recent complete HMRC data (2022/23) shows around 31,500 estates paid inheritance tax — roughly 4.6% of all UK deaths. Less than 1 in 20 estates. That proportion has barely shifted in over 15 years, despite property inflation. Full figures are available in HMRC’s inheritance tax liabilities statistics.

But — and this is the bit the charts don’t show — the number is quietly rising. The Office for Budget Responsibility forecasts IHT receipts of £8.7 billion in 2025/26, up sharply from £6.7 billion three years earlier. More estates, bigger bills, same frozen thresholds. A mathematical certainty.

The real pattern looks like this:

- London and the South East produce a disproportionate share of taxpaying estates. Property values do the heavy lifting.

- Average tax bill per taxpaying estate: roughly £212,000 (2022/23 HMRC figures).

- Widows, widowers and surviving civil partners pay the largest chunk — because they’ve already inherited the combined estate tax-free, and it all gets assessed on the second death.

- Cohabiting couples — even those who’ve lived together thirty years, raised children, bought a dog — get none of the spousal exemptions. A hard truth that still catches people out.

If you’re reading this and your property alone is worth more than £325,000 (and you’re not married), the UK inheritance tax nil rate band 2026 rules already have you on their radar. That doesn’t automatically mean a bill — there’s still the RNRB and other reliefs — but it does mean you should know where you stand.

Quick sanity check: Add up your home, savings, investments, ISAs, premium bonds, life policies not written into trust, cars, jewellery, any crypto, any business interests. Subtract debts and a reasonable funeral cost. If that figure sits north of £325,000 and you’re single — or north of £1 million as a couple with a home for the children — planning is no longer optional.

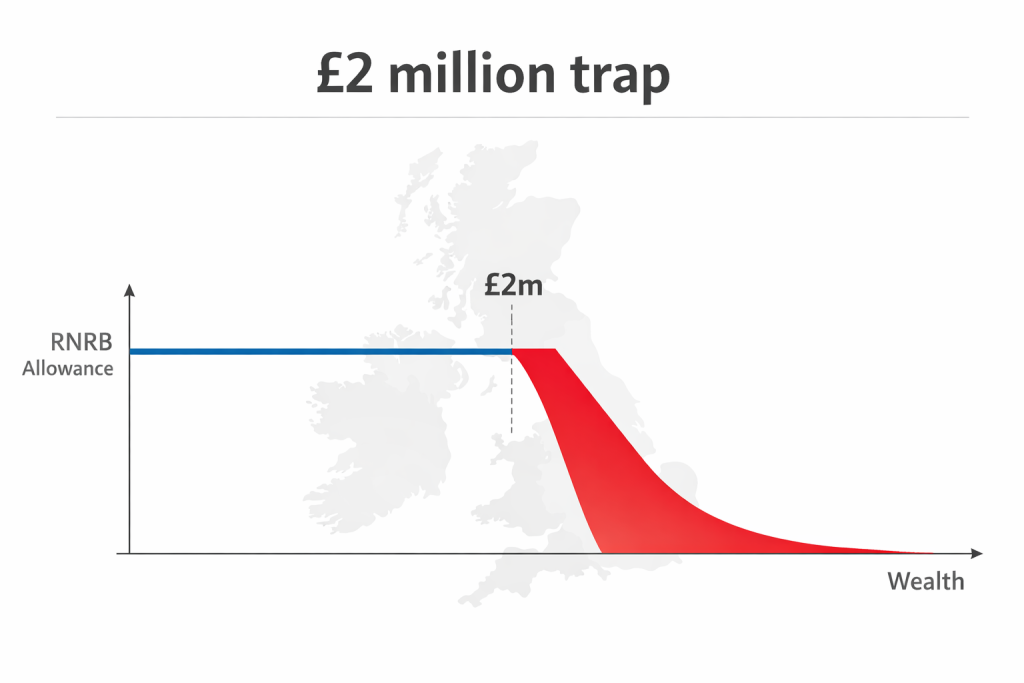

The £2 million trap nobody tells you about

Here’s where it gets spiky.

The residence nil rate band is tapered. Once your total estate crosses £2 million, you lose £1 of RNRB for every £2 you’re over. Keep going and the whole £175,000 evaporates at around £2.35 million for an individual, or £2.7 million for a couple (assuming both RNRBs stack).

This creates a genuinely odd situation where someone with an estate of £2.5 million can end up paying more tax than they’d have done with clever planning at £1.9 million. Crossing that £2 million line isn’t just breaching a threshold — it’s losing an allowance you’d otherwise have kept.

People with mid-sized business assets or a decent portfolio of property often sail into this zone without realising. Pension changes coming in April 2027 (more on those in a second) will push even more families over the line. Proper personal tax planning well before retirement age is the only sensible response.

What the 2025 Autumn Budget changed for the UK inheritance tax nil rate band 2026

Two big changes dominate the post-Budget landscape, and both bite from 2026 onwards.

First: the extended freeze. The NRB, the RNRB, and the £2 million taper threshold — all three were due to thaw in 2028, then 2030. The November 2025 Budget nailed them down until April 2031. Another year added. Inflation keeps doing its quiet work. Full context is set out in the House of Commons Library briefing on inheritance tax.

Second: agricultural and business property reliefs. Previously, qualifying farms and trading businesses could pass almost untouched by IHT via 100% relief. From April 2026, that generous 100% rate applies only up to £1 million of combined agricultural and business property per person, with a £2.5m combined allowance later confirmed for farmers following consultation. Anything above attracts relief at 50% — which, being clear about this, means a 20% effective IHT rate on value above the cap. Farmers and family businesses absolutely need tailored advice; what worked in 2024 does not work in 2026.

Third, looking ahead: pensions. From April 2027, most unspent pension pots will form part of your taxable estate for IHT purposes. This is huge. Pensions have long been the quiet hero of estate planning — people deliberately drew down ISAs and left pensions untouched, because they passed IHT-free. That’s changing. Anyone with a significant SIPP or defined contribution pot should be reviewing their strategy now, not in 2027.

The bits that reduce your bill (legally)

You’ve got more levers than you think.

- The spousal exemption — unlimited. Anything left to a UK-domiciled spouse or civil partner passes entirely free of IHT. The unused nil rate band transfers on the second death.

- The £3,000 annual gift allowance — gift up to £3,000 each tax year and it’s outside your estate immediately. Unused allowance from the previous year can be carried forward (once).

- Small gifts of up to £250 to any number of individuals.

- Wedding gifts — £5,000 to a child, £2,500 to a grandchild, £1,000 to anyone else.

- Regular gifts out of surplus income — a wonderfully underused exemption. If you can show a pattern of giving from income that doesn’t reduce your standard of living, those gifts sit outside the estate. No upper limit.

- The seven-year rule — larger gifts (potentially exempt transfers) drop out of your estate entirely if you survive seven years. Between years three and seven, taper relief reduces the tax on the gift.

- Charitable giving — anything to charity is exempt, and leaving 10%+ of your net estate to charity cuts the IHT rate from 40% to 36% on the remainder.

- Business Relief and Agricultural Relief — still valuable, still usable, but now with caps from April 2026.

On the seven-year thing, a small warning: a lot of people assume taper relief applies from year one. It doesn’t. If you die within three years of making a gift, it’s taxed at the full 40% (if it exceeds your NRB). Taper only kicks in between years three and seven. And the liability falls on the recipient, not the estate. Which can be awkward for a grandchild who wasn’t expecting a brown envelope from HMRC.

⚠️ A warning worth reading twice: Giving away your house and continuing to live in it rent-free is called a “gift with reservation of benefit”. HMRC sees right through it. The property stays in your estate for IHT purposes regardless of who’s on the deeds. This is perhaps the single most common DIY tax planning mistake we see.

A worked example, because numbers make this real

Let’s take Margaret, widowed, 78, lives in a terraced house in Wimbledon worth £850,000. She has £180,000 in savings, a small investment portfolio of £95,000, and wants to leave everything to her two children.

Her estate: £1,125,000.

Her allowances:

- Her own NRB: £325,000

- Her late husband’s unused NRB (fully transferable): £325,000

- Her RNRB (home to children): £175,000

- Her late husband’s unused RNRB: £175,000

- Total tax-free: £1,000,000

Taxable slice: £125,000. IHT due: £50,000 (40% of £125,000).

Now imagine her estate had been £2.1 million. The taper kicks in on the RNRBs — £100,000 over £2m means £50,000 of RNRB is lost. Suddenly her “million-pound shield” is only £950,000, and the extra £100,000 of estate gets taxed in full. The bill explodes. Planning ahead would have helped her manage this — an inheritance tax calculator is a good starting point, but for anything complex you want a human who understands the interaction between reliefs.

Things that quietly ruin people’s plans

A short, somewhat grumpy list based on cases I’ve seen repeat themselves:

- Out-of-date wills. A will drafted in 1998 probably doesn’t reference the RNRB, because it didn’t exist. Older trust structures can actually disqualify the RNRB entirely.

- Unequal ownership of the main home. Tenants in common with a deed that doesn’t match current circumstances can create strange outcomes.

- Assuming pensions are always IHT-free. True until April 2027. Not true after.

- Foreign assets. UK residence and long-term residence rules (reformed heavily in 2025) can bring worldwide assets into scope.

- Not claiming the transferable NRB/RNRB on the second death. You have to actively claim it. HMRC doesn’t volunteer. Miss the claim and you can lose hundreds of thousands.

- Panic gifting. Giving away large sums when you’re already unwell. The seven-year clock starts the day you give — not the day you think about giving.

A quick snapshot of recent IHT receipts (this one’s a little rough around the edges)

| Tax year | IHT receipts | Estates paying IHT | % of UK deaths |

|---|---|---|---|

| 2021/22 | £6.1 bn | ~27,800 | 4.4% |

| 2022/23 | £6.7 billion | 31,500 | 4.62% |

| 2024/25 | £8.4bn | n/a (data lag) | – |

| 2025/26 (forecast) | £8.7 billion | rising | ~5% |

Sources: HMRC, OBR forecasts. Historic estate counts subject to revision; 2023/24 onwards data will be published July 2026.

Frequently Asked Questions on the UK inheritance tax nil rate band 2026

What is the inheritance tax threshold for 2026? The standard UK inheritance tax nil rate band 2026 figure is £325,000 per person for the 2026/27 tax year. If you leave a qualifying home to your children, grandchildren, or other direct descendants, you can add the residence nil rate band of £175,000, giving you up to £500,000 as an individual. This combined threshold stays frozen until April 2031.

Can a married couple really leave £1 million tax-free? Yes — but only if they plan it correctly. Both NRBs and both RNRBs need to be available and transferable, and the home must pass to direct descendants. For estates over £2 million, taper reduces the benefit.

Does the £325,000 threshold apply to each of my children? No. The nil rate band attaches to the estate, not the beneficiaries. Whether you leave your estate to one child or ten, you still get a single £325,000 NRB (plus any spousal transfer).

What happens if my estate is worth just under £2 million? You keep the full RNRB. But estate values can fluctuate — probate valuations for property, shares and even business interests sometimes come in higher than expected. Sensible planning builds in headroom.

Are inherited pensions still tax-free? For deaths before 6 April 2027, most defined contribution pensions pass outside the estate. From April 2027, most unused pension funds will be brought into the IHT net. This is arguably the biggest estate planning shift of the decade.

Do I need to fill in an IHT return if the estate is under the threshold? Sometimes yes, even when no tax is due — particularly if you’re claiming a transferred nil rate band or RNRB. See our detailed guide to the IHT400 form for what to submit and when.

What’s the deadline for paying inheritance tax? IHT is normally due within six months of the end of the month of death. Interest runs on late payments. Certain assets (property, unlisted shares, businesses) can be paid in ten annual instalments, but interest still applies.

Where Ask Accountants UK Ltd fits in

Here’s the bit I’ll keep short because nobody enjoys being sold to.

Inheritance tax planning is one of those areas where small decisions made fifteen years too late cost families enormous amounts of money. Writing your will in your thirties is great; reviewing it every five to seven years — and after every major life event — is what actually preserves the inheritance you’re building.

At Ask Accountants UK Ltd, we deal with this daily: executors drowning in IHT400 schedules, families trying to work out whether gifting now is worth it, landlords weighing the pension changes, business owners recalibrating around the new APR and BPR caps. Our work spans personal tax planning, tax compliance, self assessment, HMRC investigations, property accounting, and financial consultancy — which is a long way of saying we see the whole picture, not just the bit in front of us.

If your estate is creeping toward or past £500,000 — and especially if it’s closing in on that £2 million taper line — a proper planning conversation tends to pay for itself many times over. Sometimes the answer is “you’re fine, stop worrying.” Sometimes it’s “we should talk about a trust.” Either way, knowing where you sit against the UK inheritance tax nil rate band 2026 thresholds is better than guessing.

You’ll find us at 178 Merton High St, London SW19 1AY — give the office a ring on 020 8543 1991, or drop us a note through the contact page. Happy to do a first chat at no charge so you know where you actually stand and what planning, if any, makes sense for your family.

And whatever you do — don’t leave this to the executor to untangle at 2am after the funeral. That’s when the mistakes happen.