You open your tax computation, scan down to the bottom line — and your face does something involuntary. The number looks wrong. Too big. Possibly a typo. Every year, thousands of limited company directors ask exactly the same question: why is my corporation tax so high? The answer is rarely one thing. It is almost always a combination of structural factors, missed planning opportunities, and — occasionally — the straightforward consequence of having a genuinely good year.

This guide works through the most common culprits honestly. No vague advice about “maximising allowances.” No watered-down generalities. Just the specific reasons UK companies end up with a higher corporation tax bill than they expected — and what you can actually do about them.

There is good news buried in most of these sections. Several of the reasons corporation tax ends up high are entirely fixable, provided someone looks at the position before the year ends rather than after.

What your corporation tax bill is actually based on

Corporation tax is not a charge on your turnover. HMRC does not calculate it from what landed in your bank account, and your director’s salary has no direct bearing on it either. The charge falls on your company’s taxable profits — income minus allowable deductions, capital allowances, and applicable reliefs.

The UK corporation tax rates and what the taper actually does to your bill

Since April 2023, the UK runs a two-rate system with a graduated taper in the middle:

- Profits up to £50,000 — 19% (small profits rate)

- Profits between £50,001 and £250,000 — marginal relief applies, blending toward 25%

- Profits above £250,000 — 25% (main rate)

The middle band is where most surprises happen. Marginal relief creates an effective marginal rate of around 26.5% on profits within that taper. That is counterintuitively higher than the main rate. If your profits sit anywhere between £50,000 and £250,000, and you keep asking yourself why is my corporation tax so high, this band is almost certainly part of the explanation.

| Profit band | Rate | What to watch out for |

|---|---|---|

| Up to £50,000 | 19% | Threshold divides between all associated companies |

| £50,001–£250,000 | Marginal relief (~26.5% effective marginal) | Easy to fall into after a strong year |

| Over £250,000 | 25% | Quarterly instalments apply above £1.5m |

| Ring-fenced profits (oil, gas) | 30% + 10% supplement | Sector-specific rules apply entirely separately |

The associated company trap that catches directors by surprise

HMRC divides both the £50,000 and £250,000 thresholds equally between all associated companies you control. Run two limited companies, and each one’s small profits threshold drops to £25,000. Three companies: £16,667 each. Directors who set up a second entity for a side project — without any tax modelling — often discover both companies pay more than expected. The implications for corporate tax planning in multi-company structures deserve proper attention before, not after, incorporation.

Expenses that push your corporation tax higher than they should

The rule sounds clean: HMRC allows deductions for expenses incurred “wholly and exclusively” for the purposes of the trade. In practice, that test catches businesses who act in complete good faith.

The most commonly disallowed expenses in UK company accounts

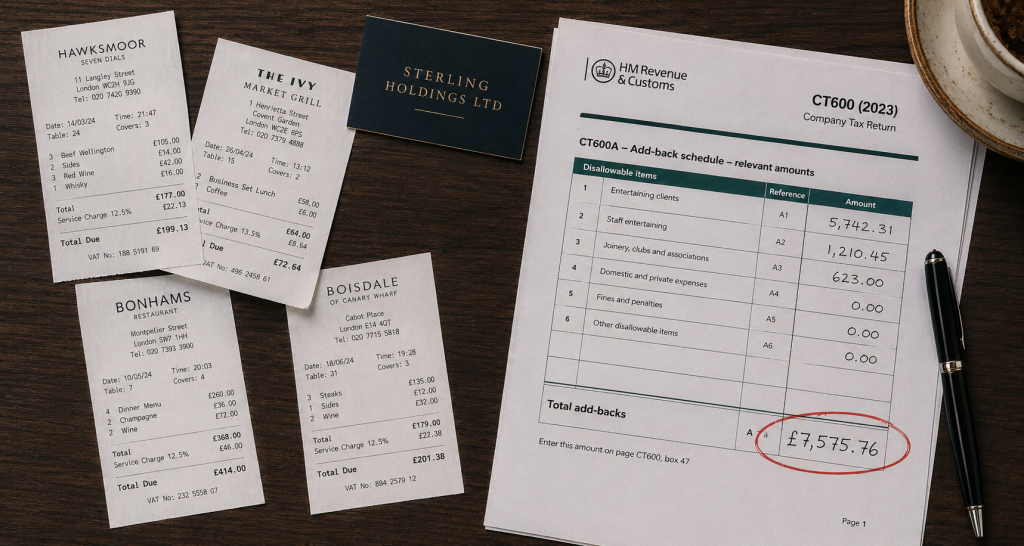

Client entertaining is the textbook example. Dinners with clients, hospitality packages, event tickets — HMRC disallows all of these for corporation tax purposes, regardless of the commercial rationale. Every pound of disallowed expenditure becomes an extra pound of taxable profit. At 25%, that means 25p of additional tax per disallowed pound. Across a full year of casual claims, the total is often genuinely surprising.

Other items that regularly get added back:

- Depreciation — always added back and replaced by capital allowances in the tax computation

- Personal expenses charged to the company (which also trigger benefit-in-kind issues)

- Fines and regulatory penalties

- Anything with a personal element that lacks a clear business-only purpose

The one that surprises people every time

Depreciation never reduces your corporation tax bill. HMRC adds it back in the computation and replaces it with capital allowances. If your accountant charges significant depreciation but claims no corresponding capital allowances — particularly the Annual Investment Allowance — you overpay. Ask to see both figures side by side.

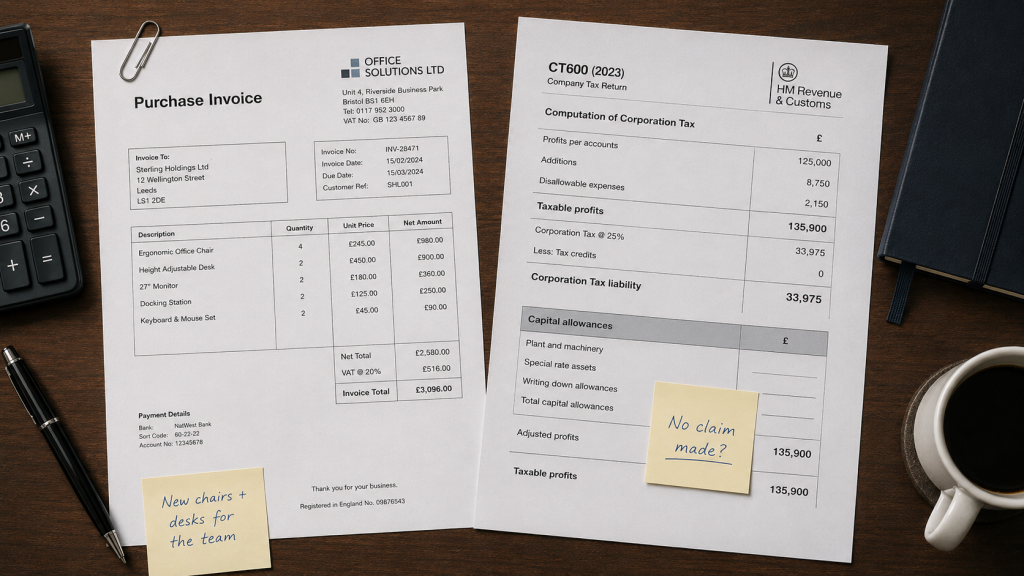

Missed capital allowances: a common reason corporation tax stays too high

The Annual Investment Allowance lets businesses deduct 100% of qualifying plant and machinery costs up to £1 million in the year of purchase. That is a significant relief. And yet businesses leave it on the table constantly — because nobody identified qualifying assets, claimed in the wrong period, or simply asked the right questions during accounts preparation.

What actually qualifies for the AIA

Qualifying expenditure covers more than most directors assume:

- Office equipment, computers, and machinery

- Commercial vehicles (cars have their own restricted rules)

- Certain fixtures within buildings — carpets, heating systems, CCTV, electrical systems

- Some types of building improvement work

If you had a year of significant capital spending and your corporation tax bill still looks eye-watering, check the capital allowances position first. Prior-year amendments can sometimes recover missed claims too — another reason why a thorough accounts and tax review pays for itself.

How your salary and dividend mix affects your corporation tax bill

This matters particularly for owner-managed businesses. The method you choose to extract money from your company directly affects the company’s taxable profit — and, in turn, why your corporation tax is high.

Why dividends keep taxable profit higher than a salary would

A director’s salary is a deductible expense for the company. Dividends are not. If you draw primarily through dividends — which many directors do, because the personal tax position can look more efficient — the company’s taxable profit stays higher than it would with a different extraction mix.

The trade-off runs in both directions: a higher salary reduces corporation tax but raises personal income tax and NICs. Getting the balance right requires modelling both together. The optimal split shifts with profit level, marginal relief exposure, personal tax position, and other income sources. A one-off calculation at incorporation — never revisited — rarely reflects the current reality. Proper personal tax planning alongside corporate planning is the right approach.

Pension contributions: the overlooked lever

Employer pension contributions reduce corporation tax, carry no NICs charge, and build retirement savings simultaneously. If you have been deferring contributions because “cash is tight,” model the position including the tax saving first. The net cost after corporation tax relief is often much lower than the headline figure suggests — sometimes low enough to change the decision entirely.

R&D relief: why your corporation tax rate may be higher than it needs to be

Research and development tax relief is one of the most consistently underclaimed reliefs in UK tax law — particularly among small businesses that assume it applies only to pharmaceutical companies or deep-tech startups.

Which businesses actually qualify for R&D relief

The qualifying test asks whether your company attempted to resolve a technological or scientific uncertainty while developing or improving a product, process, or system. That definition covers more ground than most people realise:

- Custom software development that required solving non-obvious technical problems

- Novel manufacturing processes or bespoke engineering solutions

- Certain construction methodologies

- New financial products with genuinely novel underlying architecture

The scheme underwent significant restructuring from April 2024, merging the previous SME and RDEC regimes for most companies. If you had an R&D assessment a few years ago and it produced a negative result, the current rules may give a different answer. If you have never had one assessed at all and your corporation tax is persistently high, a specialist review makes sense. The HMRC guidance on R&D relief outlines what qualifies under the merged scheme.

Prior-year losses that could reduce your corporation tax today

Companies can carry forward trading losses and set them against current profits, which reduces the taxable base. In theory, accountants handle this automatically. In practice, changes of accountant, disorganised record periods, or nobody explicitly verifying the historic position mean losses sometimes sit unused.

How trading loss rules changed in 2017 — and why it matters now

Post-April 2017 losses carry more flexibility than their predecessors. Companies can set them against total profits rather than just profits of the same trade. Pre-2017 losses remain more restricted. If your business had difficult years in 2020 or 2021 — and many did — ask your accountant to confirm explicitly that you carry those losses forward into current computations. If the answer is uncertain, that deserves investigation. See also how to recover overpaid corporation tax as an SME.

Why timing decisions keep your corporation tax bill higher than necessary

UK corporation tax runs on an accruals basis — income and expenses land in the year they are earned or incurred, not when cash moves. That creates legitimate planning opportunities, but only if someone acts before the accounting year closes.

Practical timing moves that reduce taxable profit

- Bring a major capital purchase forward into the current period to generate a full AIA deduction in a high-profit year

- Pay employer pension contributions before the year end — contributions after it fall into the following period

- Accelerate allowable expenditure into the current year when you expect lower profits next year

- Defer income into the next period where commercially sensible and the accounting treatment permits it

The fundamental problem with the standard “drop your receipts in January” approach is that the year is already over. Nothing remains to plan — tax gets counted rather than managed. For businesses where the question why is my corporation tax so high comes up every spring, the answer is usually that nobody reviewed the position in October or November, when action remained possible. Quarterly conversations with an accountant who offers proactive business advice change that dynamic entirely.

When growth is the reason — and your corporation tax bill still needs managing

Sometimes the honest answer is the most satisfying one. Your corporation tax is high because your company made significantly more money. That is good news. But unplanned growth still produces nasty surprises.

How a strong year pushes companies into a higher corporation tax rate

A company moving from £45,000 to £130,000 in taxable profit jumps from a 19% charge into the marginal relief zone in a single year. Without advance modelling — no pension review, no salary adjustment, no AIA planning — the bill feels like a punishment for success. It is not. It reflects absent planning.

The team at Ask Accountants UK Ltd works regularly with businesses at exactly this inflection point — where growth moves faster than the tax planning. Modelling a good year’s tax implications before the year ends consistently produces better outcomes than unpicking it afterwards.

HMRC enquiries: when your high corporation tax bill follows a compliance check

One more reason deserves mention, even if it is less comfortable: an HMRC enquiry that results in additional assessed tax, with interest and penalties on top.

What to do if HMRC queries your corporation tax return

If you receive an HMRC letter querying items in your return, or if a compliance check opens, get specialist representation immediately. How you respond in the early stages shapes everything that follows. The HMRC investigations process carries specific rules around timelines, evidence, and communication — and DIY responses routinely make matters worse. The complete guide to HMRC tax investigations sets out what to expect at each stage.

What common reliefs save in real numbers — a quick reference

| Relief or action | Example spend | Approx. saving | Key condition |

|---|---|---|---|

| Annual Investment Allowance | £40,000 | ~£10,000 | Qualifying plant or machinery |

| Employer pension contribution | £20,000 | ~£5,000 | Paid before year end |

| R&D merged scheme credit | £60,000 qualifying costs | £15,000+ | Genuine technological uncertainty |

| Director salary increase | +£10,000 | ~£2,500 CT reduction | NIC trade-off must be modelled |

| Prior year loss utilisation | £30,000 b/fwd | ~£7,500 | Losses correctly recorded |

| Timing capital expenditure | £50,000 purchase | Up to £12,500 | Falls within accounting period |

Illustrative only. Actual savings depend on your profit level, accounting period, associated companies, and prior claims. Always take specific advice before acting.

Still wondering why your corporation tax is so high?

Ask Accountants UK Ltd — 178 Merton High St, London SW19 1AY — works with limited companies across London on accounts and tax, corporate tax planning, bookkeeping, self assessment, and HMRC investigations. Call 020 8543 1991 or visit askaccountantsukltd.co.uk/contact-us.

Frequently asked questions about high corporation tax bills

Why is my corporation tax so high when my profits look modest?

Disallowed expenses, missed capital allowances, and the associated company rules all push taxable profit above what you might expect from your trading figures. The marginal relief taper also creates an effective marginal rate of around 26.5% — higher than the main rate — for profits between £50,000 and £250,000. A full review of your CT computation identifies which factors drive the figure. See also accounting for small companies — compliance guide.

What is the UK corporation tax rate in 2024–25?

The main rate stands at 25% for profits above £250,000. The small profits rate of 19% applies to profits up to £50,000. Between those figures, marginal relief tapers the charge. HMRC divides both thresholds between associated companies — so controlling multiple companies changes the entire calculation. The HMRC corporation tax rates page holds the current official figures.

Can I reduce my corporation tax legally?

Yes — and several entirely standard routes exist. Employer pension contributions, Annual Investment Allowance claims, salary and dividend optimisation, R&D relief, and prior-year loss carry-forwards all reduce taxable profit legitimately. The critical caveat is timing: most measures require action before the accounting year ends. Tax compliance and corporate tax planning done proactively — rather than retrospectively — delivers the difference.

What expenses does HMRC disallow for corporation tax?

Client entertaining tops the list — HMRC disallows it regardless of how commercially driven it is. Depreciation always gets added back and replaced by capital allowances. Personal expenses run through the company, regulatory fines, and anything lacking a wholly business purpose all face disallowance too. Your accountant should show these add-backs explicitly in the tax computation. If you cannot see them, ask.

What is marginal relief and how does it raise my corporation tax?

Marginal relief tapers the charge from 19% to 25% for companies with profits between £50,000 and £250,000. The mechanism creates an effective marginal rate of around 26.5% on profits within the band — temporarily higher than the main rate. A company earning £120,000 in taxable profit pays a higher marginal rate than one earning £400,000. Planning profit levels through pension contributions, capital expenditure timing, or salary adjustments can reduce the exposure significantly.

Does owning two companies affect my corporation tax rate?

Yes — significantly. Associated companies share the £50,000 and £250,000 thresholds equally, so two associated companies each face a small profits threshold of £25,000 and a marginal relief upper limit of £125,000. Both can sit inside the taper simultaneously. Model this before incorporating a second entity. Read more about financial consultancy for business structures.

When does corporation tax become due?

For most small companies, payment falls due nine months and one day after the accounting period ends — so a 31 March year end means a 1 January payment deadline. Companies with profits above £1.5 million pay in quarterly instalments. Missing the deadline triggers interest on top of the tax. The guide to corporation tax return deadlines covers both the payment and filing timetables in full.

What happens if I overpaid corporation tax?

Companies can amend a corporation tax return within 12 months of the original filing deadline. Overpayments from missed allowances or unapplied losses qualify for repayment via amendment or an overpayment relief claim. Recovering overpaid tax as an SME explains both routes and what documentation HMRC requires.