Estimated reading time: 10 minutes

So you’ve got a tenant in, the standing order lands on the first of every month, and life looks tidy. Then January creeps up, a polite-but-firm letter from HMRC arrives, and you realise that tax on rental income UK landlords face isn’t optional — and it isn’t simple either. I’ve watched perfectly competent people, the sort who run businesses or hospital wards, freeze when they realise they’ve underpaid by four years. The rules shift. The reliefs shrink. And the bit everyone forgets? Mortgage interest is no longer your friend in the way it used to be.

This is the guide I wish more landlords had read before their first self-assessment. No jargon for the sake of it. No pretending it’s easy when it isn’t.

How HMRC actually treats tax on rental income UK landlords pay

Here’s the framing that helps. Rental profit isn’t separate income with its own pretty little rate. It gets stacked on top of everything else you earn — your salary, your dividends, your pension drawdown — and then taxed at whatever band the total lands in. That’s the whole game, really.

For the 2025/26 tax year (running 6 April 2025 to 5 April 2026), the English, Welsh, and Northern Irish bands look like this:

| Band | Income range | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | Over £125,140 | 45% |

Scotland plays by its own rules — five bands, slightly different thresholds — and that catches out a lot of cross-border investors who own a flat in Edinburgh while paying PAYE from a Manchester employer. If that’s you, check the HMRC guidance before assuming the figures above apply.

Now, the calculation itself goes:

- Add up the rent you received in the tax year.

- Subtract your allowable expenses.

- The leftover is your taxable rental profit.

- Add it to your other income.

- Pay tax at whatever rate the total lands in.

Simple in theory. The devil — predictably — lives in step 2.

Cutting your tax on rental income UK with allowable expenses

Allowable expenses are anything “wholly and exclusively” for the letting. Phrase that bit aloud a few times, because that’s the test. A leaking radiator? Yes. A new kitchen with quartz worktops that wasn’t there before? That’s an improvement, not a repair — and HMRC treats improvements as capital, not deductible against income.

The everyday list of legitimate deductions includes:

- Letting agent and management fees

- Buildings and contents insurance

- Repairs and maintenance (genuine like-for-like restoration)

- Ground rent and service charges

- Council tax and utility bills when you, the landlord, pay them

- Accountancy fees for preparing the rental accounts

- Legal fees on tenancy agreements (not on buying the property)

- Cleaning and gardening between tenancies

- Advertising for new tenants

Things landlords routinely try to slip through that HMRC will gleefully refuse: clothing for the property visits, the petrol from a holiday during which you “happened” to pop in, your own labour valued at £40 an hour. Don’t. Just don’t.

A note from the trenches: keeping receipts in a shoebox until January is the single most expensive habit in landlord-land. Every receipt you can’t find is a deduction you can’t claim, and a deduction you can’t claim is tax you needn’t have paid.

If you’d rather not wrestle with the spreadsheet yourself, this is the sort of thing a bookkeeping service or cloud accounting setup quietly handles in the background — receipts photographed on the phone, categorised, ready by April.

Section 24: the rule that quietly reshaped buy-to-let

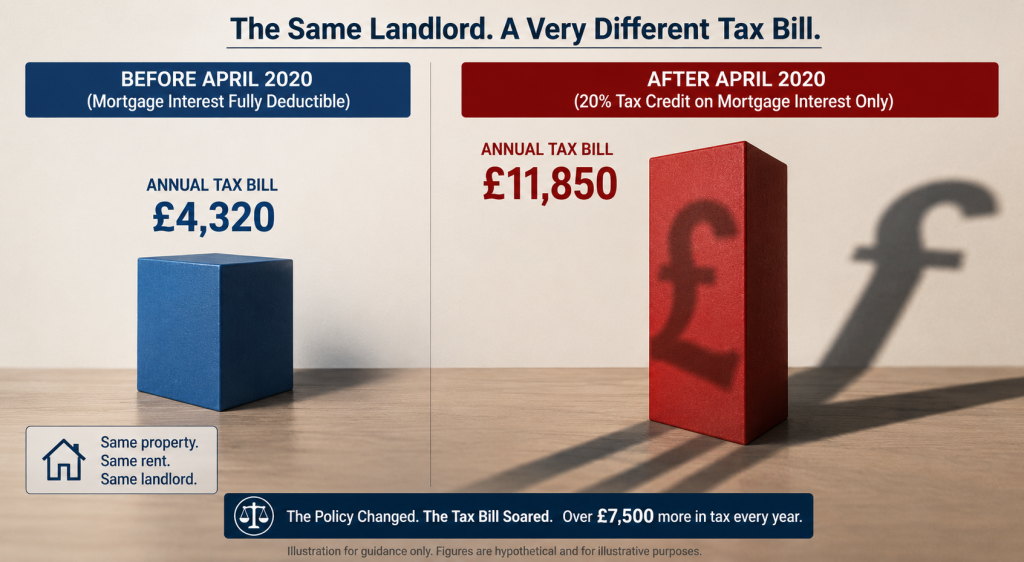

Right. If there’s one thing that genuinely changed the maths of being a landlord in this country, it’s Section 24 of the Finance (No. 2) Act 2015. Phased in from 2017, fully in force since April 2020.

Before Section 24, mortgage interest came off your rental income as a normal expense. A higher-rate taxpayer paying £8,000 in interest effectively got £3,200 back via the tax system. That world is gone.

Now? You can’t deduct mortgage interest from rental income at all. Instead, you receive a basic-rate (20%) tax credit applied against your overall tax bill. For a 20% taxpayer this often nets out roughly the same. For a 40% or 45% taxpayer it stings — quite badly, in some cases. Worse, the credit doesn’t reduce your gross income for band calculations. That’s why some landlords find themselves shoved into higher-rate territory on paper despite their real-world cash position barely moving.

Here’s a quick worked snapshot of how the tax on rental income UK landlords pay differs by tax band — and yes, the formatting on this one is a touch rough around the edges; I built it from a real client conversation:

| Item | Basic-rate landlord | Higher-rate landlord |

|---|---|---|

| Rental income | £14,400 | £14,400 a year |

| Allowable expenses (not interest) | £2,000 | 2,000 |

| Mortgage interest paid | £6,000 | £6,000 |

| Taxable rental profit | £12,400 | £12,400 |

| Tax before credit | £2,480 (20%) | £4,960 (40%) |

| 20% mortgage interest credit | −£1,200 | −£1,200 |

| Final tax due | £1,280 | £3,760 |

The higher-rate landlord pays nearly three times the tax for the same property. That’s the bit nobody told you when buy-to-let was being pitched as a retirement plan in 2014.

When £1,000 lets you off the hook

If your gross rental receipts are under £1,000 a year — perhaps you let a single room on Airbnb a handful of weekends — the property allowance kicks in automatically. No tax. No return needed (assuming no other reason to file). HMRC’s gift to the casual landlord.

Between £1,000 and roughly £2,500, you can sometimes settle things via PAYE coding. Above that, you’re firmly in self-assessment territory.

Also worth knowing: the Rent a Room scheme allows up to £7,500 tax-free if you let a furnished room in your own home. Two distinct schemes; people mix them up constantly.

Self-assessment: where the tax on rental income UK gets reported

Every landlord earning above the £1,000 property allowance must register for self-assessment by 5 October following the end of the tax year in which the rental income first arose. Miss that, and HMRC views it as “failure to notify” — which carries penalties up to 100% of the unpaid tax in the nastier cases.

Then the deadlines themselves:

- 31 October for paper returns

- 31 January following the tax year end for online returns and payment

- 31 July for the second payment on account, if you’re caught by the rules

The penalty escalator is unkind: £100 the day you’re late, daily £10 charges kicking in at three months, then percentages of unpaid tax at six and twelve months. I’ve seen landlords rack up £1,600 in penalties on a £200 tax bill simply because they ignored the brown envelopes.

Need the full timeline? We keep an updated self-assessment key dates page that’s worth bookmarking.

What’s changing — and why 2026 is the year to actually pay attention

A few things on the horizon are worth flagging now rather than discovering in a panic later.

Making Tax Digital for Income Tax Self-Assessment becomes mandatory from 6 April 2026 for landlords (and the self-employed) with combined qualifying income above £50,000. That means quarterly updates to HMRC via approved software — not annual returns. The threshold steps down to £30,000 from April 2027, and £20,000 from April 2028. If you’ve been managing things on a notepad, that approach has a sell-by date. Our QuickBooks for landlords setup guide walks through one of the simpler routes to compliance.

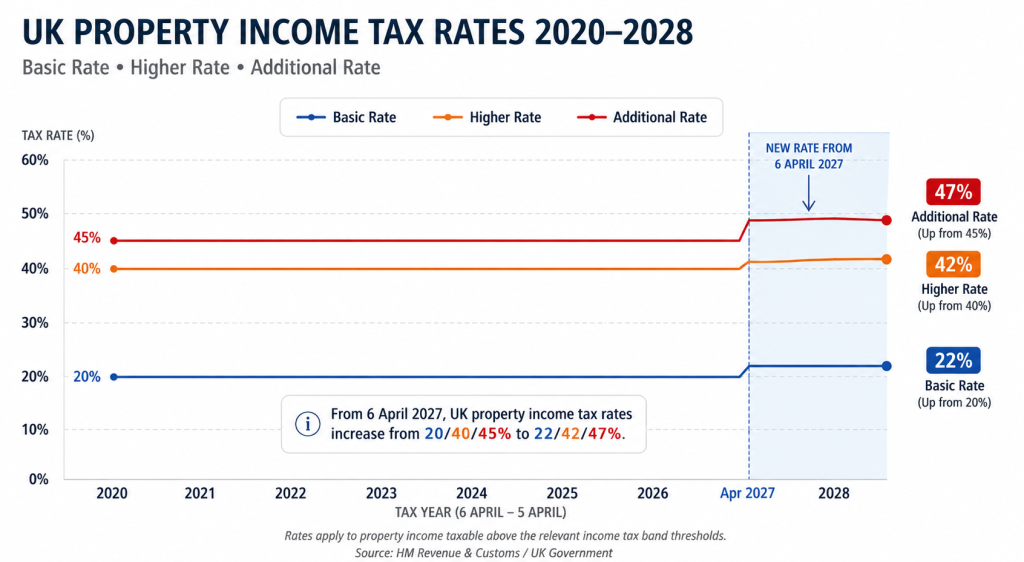

Property income tax rates rise by 2 percentage points from April 2027. Announced in the Autumn 2025 Budget. The new property-specific rates will be 22% basic, 42% higher, 47% additional — meaning the tax on rental income UK property owners pay will be slightly harsher than tax on other income for the first time in modern memory. The mortgage interest credit also moves to 22% from the same date, which softens the blow marginally but doesn’t undo it.

Furnished Holiday Lettings lost their special tax status from 6 April 2025. If you ran a cottage in Cornwall under the old FHL regime, the capital allowances, the pension contribution treatment, and the business asset disposal relief — all gone. Now treated like any other residential let.

⚠️ Heads up if you’re sitting on a portfolio: The combination of the 2027 rate rise, the 5% additional-property SDLT surcharge introduced in 2024, and the now-£3,000 capital gains tax annual exemption means the maths of selling versus holding has shifted significantly. Before you make any move, the right personal tax planning conversation could be worth thousands.

Should you put your rental into a limited company?

The eternal question. Limited companies aren’t caught by Section 24 — they still deduct mortgage interest as a normal business expense. They pay corporation tax (19–25% depending on profits) rather than income tax at up to 45%. Sounds great. Until you try to move the property in, at which point Stamp Duty and CGT make a noisy entrance.

For someone buying their first buy-to-let with a long horizon and higher-rate income, a limited company often makes sense. For an established landlord with one or two properties bought years ago at a low base cost, the incorporation costs frequently outweigh the savings. There is no universal answer here, which I find genuinely refreshing in an industry that loves blanket advice.

Walk through the actual numbers with someone who’ll model both scenarios. The Wimbledon team at Ask Accountants UK Ltd does this regularly through our property accounting and corporate tax planning services.

Capital Gains Tax: the parting gift when you sell

When you eventually sell, CGT applies to the gain. For residential property in 2025/26:

- Annual exempt amount: just £3,000 (down from £12,300 a few years ago)

- Basic-rate taxpayers: 18%

- Higher and additional rate: 24%

- Reporting deadline: 60 days from completion via the UK Property Account

Sixty days. That trips up more sellers than any other rule. The solicitor doesn’t always remind you. The estate agent definitely won’t.

FAQ on tax on rental income UK landlords keep asking

Do I need to declare rental income if I make a loss? Yes, if your gross rent exceeds the £1,000 property allowance. The loss itself gets carried forward against future rental profits — you can’t usually set it against your salary.

Is rental income from abroad taxed in the UK? If you’re UK tax-resident, generally yes — on the SA106 supplementary pages. Double-taxation treaties may reduce the bill if you’re paying tax in the source country too.

What about joint ownership? Income is normally split in line with the beneficial ownership. Married couples and civil partners default to 50/50 unless they file a Form 17 to declare a different split, backed up by actual unequal ownership.

Can I claim the cost of replacing white goods? Yes — under the replacement of domestic items relief, the like-for-like cost of replacing furniture, white goods, kitchenware, and similar items in a residential let is deductible. The first-time purchase of those items isn’t.

Will HMRC really find out if I don’t declare? Almost certainly. HMRC’s Let Property Campaign has been running for over a decade, and they now cross-reference data from letting agents, the Land Registry, deposit schemes, and even online platforms. Voluntary disclosure carries far lighter penalties than getting caught — which is why HMRC investigations involving undeclared rent often end with significant back-tax demands plus interest.

How many times can I claim before HMRC starts asking questions? Claims aren’t the issue — disproportionate claims are. A landlord claiming £15,000 of repairs on a flat that rents for £14,000 is going to attract attention. Reasonable, documented, consistent — that’s the trio.

Bringing it home

The tax on rental income UK landlords face has become one of those topics where the rules genuinely matter and the cost of getting them wrong is rising every year. Section 24 reshaped the maths. MTD is about to reshape the admin. The 2027 rate hike will reshape your net yield. Trying to manage all three with goodwill and a calculator? Brave. Expensive, usually.

If you’d rather hand the worry to someone who lives in this material — including the tax compliance side and the year-round bookkeeping — the team at Ask Accountants UK Ltd has been quietly looking after London landlords for years. We’re at 178 Merton High St, London SW19 1AY, reachable on 020 8543 1991, and happy to talk through your specific situation before you commit to anything. Most first conversations cost nothing but half an hour of your time, which is the smallest investment in this whole article.

Get the structure right early. The compounded saving over a decade of letting is usually worth far more than the fee.