You finish a job. The plastering’s done, the invoice goes out, the client says “lovely, thanks.” And then the money lands in your account — short. Noticeably short. A chunk has vanished before you’ve even had a chance to spend it. So why is CIS tax deducted from payments before the cash even reaches you? Because HMRC collects the construction industry’s income tax at the source, and that missing slice is the proof.

If you’ve ever stared at a remittance and wondered who picked your pocket, welcome. The short answer to why is CIS tax deducted from your payments is this: HMRC doesn’t trust the construction industry to pay its own tax bill on time. That sounds harsh. It’s also, historically, fairly accurate.

Let me explain properly, because the missing money isn’t lost — and understanding the mechanics behind it can genuinely change how much ends up back in your pocket come January.

So, why is CIS tax deducted from payments before you even get paid?

The Construction Industry Scheme — CIS to its friends, and to everyone who’s ever filled out a monthly return and lost an evening to it — is HMRC’s way of collecting income tax up front from subcontractors. Rather than waiting until the end of the tax year and hoping a self-employed bricklayer has diligently squirrelled away enough to cover his bill, the taxman gets the contractor to skim a slice off the top of every labour payment and hand it over directly.

Think of it as tax on layaway. These deductions count as advance payments towards the subcontractor’s tax and National Insurance obligations. You’re not paying extra. You’re paying early, whether you fancied it or not.

The scheme exists because construction has always been a cash-heavy, contractor-heavy, here-today-gone-to-a-different-site-tomorrow kind of world. Decades ago the government grew tired of self-employed tradespeople vanishing before the tax was collected. So they built a system that grabs the money at source. Decidedly unsentimental, but effective.

Here’s the part people miss, though, and it’s the bit that matters most: the amount deducted depends entirely on whether you bothered to register.

The three numbers that decide everything

CIS gives you one of three deduction rates, and which one lands on your payments comes down to your status with HMRC.

| Your CIS status | Deduction rate | What it means for you |

|---|---|---|

| Registered subcontractor | 20% | The standard rate. The one most subbies see. |

| Not registered (or can’t be verified) | 30% | The “you couldn’t be bothered to register” penalty. |

| Gross payment status | 0% | Paid in full. You sort your own tax later. |

Read that again. If you register as a subcontractor, you pay 10% less in tax deductions. An extra ten pence in every pound, just for filling in a free form. I’ve genuinely seen tradespeople leave thousands sitting with HMRC for a year because nobody told them registering was worth the bother. It is. Always.

Quick gut-check: Unregistered and watching 30% disappear? You’re effectively giving HMRC an interest-free loan of money you’ll mostly get back anyway. Register. Today. It costs nothing and the rate drops to 20% the moment HMRC can verify you.

What actually gets taxed (hint: less than you fear)

This trips people up constantly, and it’s the difference between a fair deduction and a robbery.

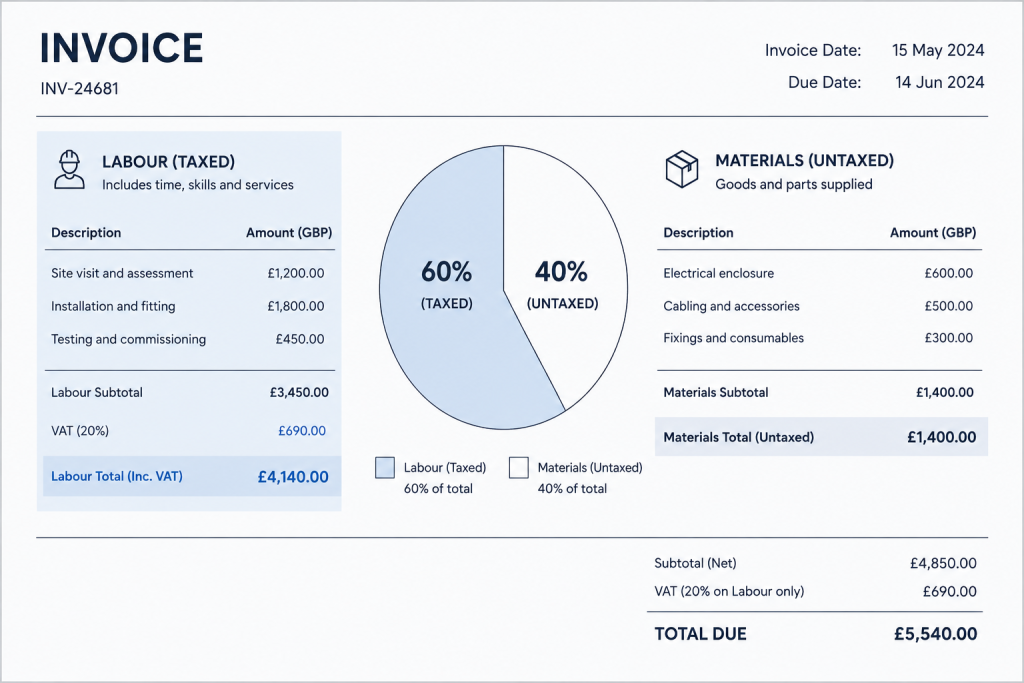

CIS only bites on the labour portion of your invoice. Materials? Untouched. VAT? Excluded. Plant hire and certain other costs? Generally left alone. So if you’ve billed £18,000 with a big slug of that being timber, tiles and rented kit, the 20% doesn’t come off the whole £18,000 — only the labour element.

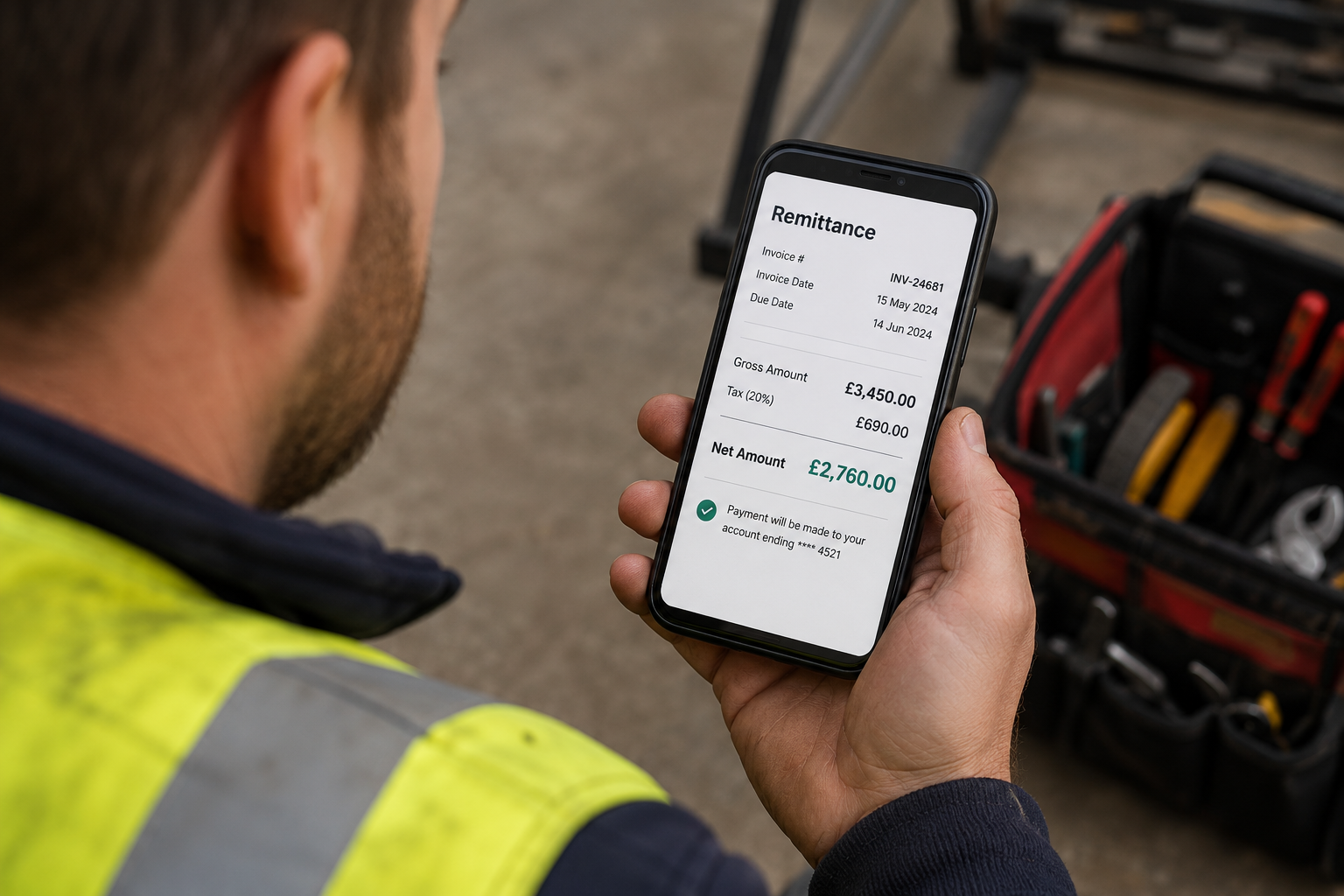

A real-world shape of it: a self-employed decorator invoices £18,000 of labour, registered for CIS. The contractor withholds 20%, which is £3,600, and she’s paid £14,400. Her materials get paid in full, no deduction. Come the tax return, that £3,600 isn’t gone — it’s sitting against her liability, and more often than not it tips her into a refund.

Which raises the obvious, slightly maddening question…

Why is CIS tax deducted from payments if you might not even owe it?

Ah. This is where the scheme feels almost personal.

Because CIS is a blunt instrument. It deducts a flat 20% from labour regardless of your actual circumstances — your personal allowance, your expenses, your van, your tools, your overheads, the lot. None of that gets factored in at the point of deduction. HMRC takes its cut first and reconciles the maths later.

So a subcontractor with modest earnings and a healthy pile of allowable expenses can easily have more deducted across the year than they actually owe. The result? A refund. Quite often a sizeable one. This is precisely why so many construction workers end up owed money — the system overcharges by design and trusts you to come and ask for the difference back.

And plenty never do, which is the part that quietly frustrates me. That’s your money sat in a government account.

The status that makes deductions disappear

Gross payment status is the holy grail. Pass HMRC’s tests and contractors pay you the full invoice — no 20%, no waiting, vastly better cash flow. For these subbies, the question of why is CIS tax deducted from payments simply stops applying. You then handle your own tax through Self Assessment or Corporation Tax once a year, like a grown-up.

Getting it isn’t a formality, mind. You have to clear three hurdles:

- The business test — you genuinely do construction work in the UK and operate through a proper business bank account.

- The turnover test — your net turnover (excluding VAT and materials) hits the threshold. For sole traders that threshold remains £30,000. For partnerships and companies it’s £30,000 per partner or director, or £100,000 across the whole entity.

- The compliance test — every relevant return and payment filed on time over the past 12 months.

That third one is the killer. And it got harder.

The bit nobody warned the industry about

Here’s a slightly imperfect timeline of how the rules tightened — I’ve kept it rough because, frankly, that’s how it landed on most subbies: in fragments.

| When | What changed | Why it stings |

| 6 April 2024 | VAT compliance added to the gross payment status tests | One late VAT return can now cost you your status |

| April 2026 | HMRC can remove gross status immediately where fraud is suspected | No 90-day notice — and a five-year wait to reapply |

From 6 April 2024, the criteria for obtaining and retaining Gross Payment Status have been tightened. A significant update is the integration of VAT compliance into the CIS compliance tests. Miss a VAT deadline, and the status you spent years earning can evaporate.

The 2026 reforms went further. HMRC can now remove gross payment status with immediate effect — bypassing the usual 90-day notice period — where it believes a business knew or should have known that a payment was connected to fraud. Where that happens, the wait to reapply jumps from one year to five, with penalties of up to 30% on top.

Translation: gross status is brilliant, but it’s now a privilege you have to keep earning every single quarter.

⚠️ A warning I wish more subbies heard: Treating your VAT returns as an afterthought used to be merely annoying. Since April 2024 it can knock out your gross payment status and drag you straight back to 20% deductions on every job. Sloppy admin now has a price tag.

Getting your money back (the good news)

So we’ve established the deduction isn’t a fine — it’s a prepayment. Which means the natural sequel to why is CIS tax deducted from payments is how do I get the overpayment back?

For sole traders and partnerships, it flows through your annual Self Assessment return. You declare your income, claim your expenses, and the CIS already deducted gets offset against your final bill. Overpaid? Refund. For limited companies it’s a touch fiddlier — deductions are reclaimed through the payroll system and set against PAYE and other liabilities.

The catch, and it’s a real one: you can only reclaim what you can prove. That means hoarding every CIS payment and deduction statement your contractor sends you. Lose those and you’re trying to reconstruct a year of deductions from memory. Don’t.

This is also where the right paperwork habits — proper bookkeeping, clean records, deadlines met — quietly determine whether your refund is smooth or a slow-motion headache.

Where a good accountant earns their fee

I’ll be honest about something. CIS is one of those areas where DIY works fine right up until it doesn’t — a mis-verified subcontractor, a return filed late, materials and labour split wrong on an invoice, and suddenly you’re explaining yourself to HMRC.

At Ask Accountants UK Ltd in Wimbledon, we spend a fair chunk of our time on exactly this: handling CIS claims and refunds so subcontractors actually get back what they’re owed, running CIS returns filing and payroll for contractors who’d rather build than file, and keeping the wider picture tidy through accounts and tax, bookkeeping and tax compliance. When HMRC come knocking — and in construction they sometimes do — our HMRC investigations support is there too.

If you’ve read this far and quietly realised you’ve never claimed a CIS refund, or you’re not sure your gross payment status is safe under the new VAT rules, that’s worth a conversation. We’ve also written a plain-English guide on how to claim a CIS refund and a piece on the CIS compliance mistakes that catch contractors out if you’d rather read first and ring later.

You’ll find us at 178 Merton High St, London SW19 1AY, or on 020 8543 1991. No jargon, no judgement about that shoebox of receipts.

Frequently asked questions

Is CIS an extra tax on top of income tax? No. It’s a prepayment of your income tax and National Insurance, not a separate charge. Whatever’s deducted gets offset against your final bill — and frequently leaves you due a refund.

Why is CIS tax deducted from payments at 30% instead of 20%? Because you’re not registered for CIS, or the contractor couldn’t verify you with HMRC. Register and the rate drops to 20% almost immediately. There’s rarely a good reason not to.

Does CIS apply to the materials I buy? No. CIS is deducted from the labour portion only. Materials, VAT and certain costs like plant hire are paid in full, which is why splitting your invoice correctly matters.

How long do I wait for a CIS refund? For sole traders it’s tied to your Self Assessment — file promptly after the tax year ends (6 April) and refunds often arrive within a few weeks, though HMRC timescales vary. Limited companies reclaim via payroll, which can take longer.

Do contractors have to deduct CIS, or is it optional? Mandatory. Contractors are legally required to register, verify every subcontractor, deduct at the correct rate and file monthly returns. Getting it wrong invites penalties.

Can I avoid CIS deductions entirely? Yes — by securing gross payment status. But you’ll need to pass the turnover, business and (since April 2024) VAT compliance tests, and keep your filing spotless to hold onto it.

For the official rules straight from the source, HMRC’s Construction Industry Scheme guidance and the subcontractor pages are worth a bookmark.