There’s a particular look I’ve come to recognise on the faces of contractors who walk into our office for the first time, usually after their first proper run-in with construction accounting. Equal parts exhausted and slightly cornered. Usually they’ve just had a letter. Sometimes a phone call. Almost always a number — a number that doesn’t quite match what they thought they owed, or what they thought they were owed, or what they remember signing for back in February when the world was simpler and the boiler at home wasn’t broken.

If you build things in the UK for a living, you already know the deal: the actual building is the easy part. The paperwork is the bit that makes grown adults stare into their tea.

This guide is my attempt to clear some of that fog before April 2026 lands and changes a fair chunk of what you thought you knew. Construction accounting isn’t normal accounting. It just looks like it from a distance.

Why generic bookkeeping templates fail at construction accounting

Most generic small-business accounting assumes a fairly polite cycle: do the work, send the invoice, get paid in 30 days, pay your taxes, repeat. Tidy.

Construction laughs at that.

You quote a job in March. You start in April. You pay for materials in May. You submit the first valuation at the end of June. Retention sits there until the next ice age. Meanwhile your subbie wants paying on Friday, the diesel bill came in Tuesday, and HMRC would like a word about last month’s CIS return. By the time you “finish” the job, the financial year has rolled over twice and nobody’s quite sure whether the project actually made money.

That’s construction accounting in one paragraph. Costs run ahead of revenue. Revenue trails the work. Tax obligations don’t politely wait for your cash to arrive.

Real talk: A profitable construction project on paper can simultaneously bankrupt you. Profit and cash are different animals. Anyone who tells you otherwise has never watched a contractor sweat through a 90-day retention.

The Construction Industry Scheme — and why April 2026 matters more than you think

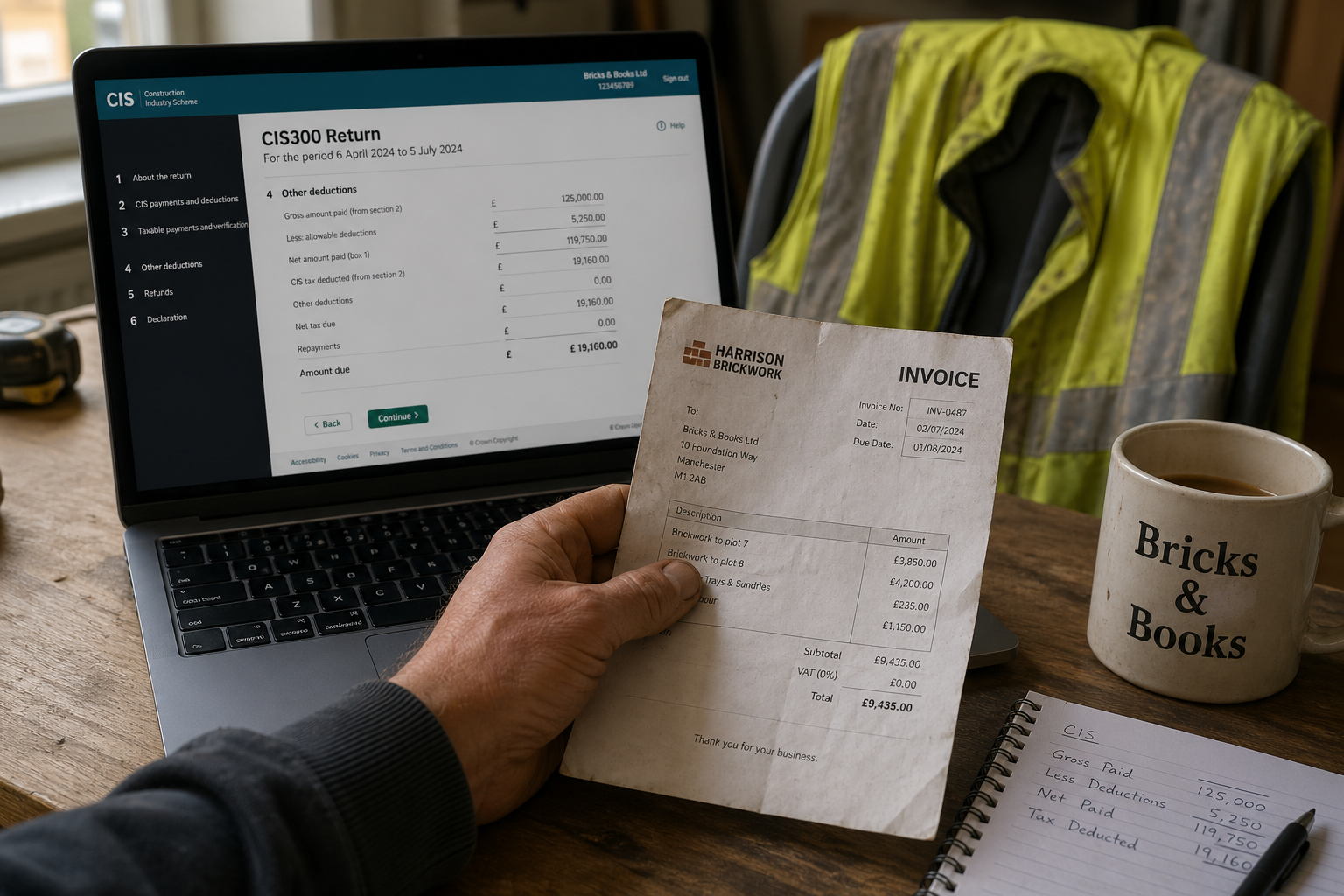

CIS. Three letters. A surprising amount of grief. And the single biggest pillar of construction accounting for anyone who pays subcontractors.

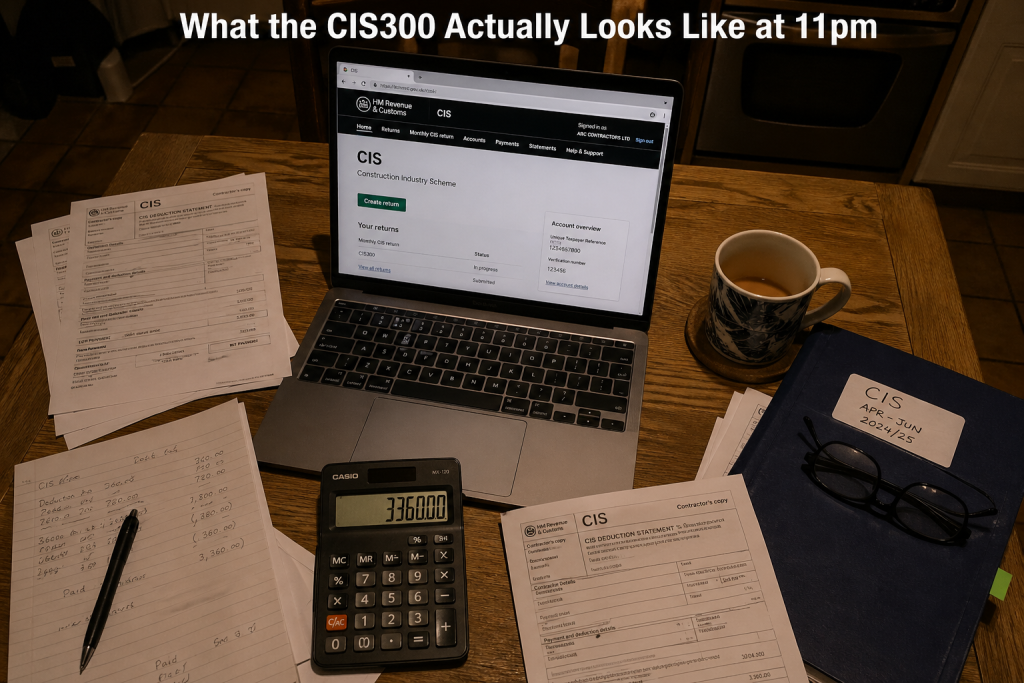

If you’re a contractor, you deduct tax from payments to subcontractors and hand it to HMRC. 20% if they’re registered. 30% if they’re not. Nothing if they’ve got Gross Payment Status. You verify them before they start, you give them a deduction statement, you file a CIS300 every month by the 19th, and you keep the records for at least three years. The full mechanics live in HMRC’s CIS340 guide if you fancy a long read.

That bit hasn’t changed. What is changing — and changing fast — is everything sitting around it.

What’s actually changing on 6 April 2026

From 6 April 2026, three significant shifts arrive:

1. Nil returns become mandatory again. Between 2015 and now, you didn’t have to file a CIS return in months where you paid no subcontractors. From April 2026, you do — unless you tell HMRC in advance that you’re going inactive (the inactivity request gets you a six-month break). Miss it and the old penalty regime kicks back in: £100 the moment you’re late, £200 once it’s two months overdue, £300 (or 5% of the liability, whichever is bigger) at six months, and a further £300 or 5% beyond that. Stack a few of those across a quiet winter and the number stops being trivial.

2. Local authority and certain public body payments leave CIS entirely. If you sub-contract to a council or qualifying public body, those payments come out of scope. No deductions, no reporting, no fuss. This actually simplifies things — finally, a change moving in the right direction.

3. The fraud powers get genuinely sharp. Where HMRC can show that a business “knew or should have known” a payment connects to fraud, they can cancel Gross Payment Status on the spot, transfer the tax liability up the chain, and slap on a 30% penalty. The reapplication ban for GPS jumps from one year to five. That’s not a technical tweak. That’s a shotgun aimed at supply chain due diligence.

The takeaway? If you’ve been casual about who you bring onto a job — verifying once, never checking again, taking the lowest quote without questions — that approach has a sell-by date. April 2026.

CIS deduction rates at a glance

| Subcontractor type / payment | Deduction rate |

|---|---|

| Registered subcontractor (standard) | 20% |

| Unregistered subcontractor | 30% |

| Subcontractor with Gross Payment Status | 0% |

| Materials portion of an invoice | 0% (always — but the materials must be reasonable and verifiable) |

| Payments to a Local Authority (post April 2026) | Outside CIS |

If you’re sitting on overpaid CIS from previous tax years, that’s recoverable — our walkthrough on how to claim a CIS refund covers the process end to end.

The VAT reverse charge: construction accounting’s quiet headache

Right. The domestic reverse charge.

HMRC introduced it in March 2021, mostly to stop “missing trader” fraud where suppliers charged VAT, pocketed it, and vanished before HMRC could ask any questions. Reasonable goal. Painful execution. The full government guidance lives at GOV.UK’s VAT domestic reverse charge page.

The mechanic itself is straightforward enough. If you’re a VAT-registered subcontractor invoicing a VAT-registered contractor for work that falls under CIS, you don’t charge VAT. You write “Reverse charge: customer to pay VAT to HMRC” on the invoice and keep moving. The contractor accounts for the VAT on their own return — both as output and input tax, which usually nets to zero.

Where it bites is the cash flow. As a subbie, you used to invoice £10,000 + £2,000 VAT and bank £12,000 until the next quarter. Now you invoice £10,000 net. That two grand isn’t yours, and it never was — but for years it sat in your account acting like it was. Plenty of small subcontractors didn’t realise how much that VAT float was bankrolling their week-to-week trading until it disappeared.

When the reverse charge does NOT apply

The exceptions matter. The reverse charge does not apply when:

- the customer isn’t VAT or CIS registered

- the customer gives you written end-user notification (and they have to give it in writing, before you invoice)

- the supply is zero-rated (new residential builds being the big one)

- the parties are connected landlords and tenants or group companies with proper notification

That end-user notification is where I see contractors come unstuck. HMRC’s compliance teams have moved well past the “light touch” they promised in 2021 — they now actively review developer VAT returns, ask for end-user notifications, and where the paperwork is missing or dated wrong, they issue assessments. Penalties of 30% of the input VAT recovered. Interest at 2.5% over base. None of which gets offset by the contractor’s matching output VAT, which is the part that really stings.

⚠️ Awkward warning, written in plain English: If you’re a developer or end user and you can’t produce a written end-user notification dated before the contractor’s first VAT-charged invoice, you have a problem. Find your file. Find it now. Better to find the gap yourself than have HMRC find it for you. If something has already gone wrong, our HMRC investigations support handles exactly this kind of unpicking.

Work-in-progress and the construction accounting profit illusion

Construction is one of the only industries where the question “did this job make money?” doesn’t have a same-day answer. Proper construction accounting forces you to look harder.

Under FRS 102, you account for long-term contracts using a method that recognises revenue as the work is performed — typically based on costs incurred relative to total expected costs (the percentage-of-completion approach, more or less). The point being: your accounts should reflect the economic reality of where the project is, not just what you’ve invoiced.

In practice, this means three things working at once:

- Costs to date — every subbie payment, material purchase, plant hire, site cost, indirectly attributable overhead.

- Estimate to complete — your honest projection of what’s left to spend. This is the bit that gets fudged.

- Stage of completion — usually expressed as a percentage, applied to the contract value to give you recognised revenue.

The illusion this exposes is something I see constantly: a contractor looks at the bank balance, sees money, and assumes the business is doing well. It might be. Or it might run on subcontractor invoices that haven’t yet been paid, retentions that won’t crystallise for 18 months, and an estimate-to-complete that was wishful thinking when someone first wrote it down.

Proper job costing — actual figures, updated weekly, tracked against the original quote — separates contractors who grow from contractors who limp from project to project wondering where the year went. A clean bookkeeping setup is the difference between knowing where you stand and guessing.

The retention problem (and the cash flow truth)

Retention. The 5% (sometimes 3%, occasionally more) the customer holds back on every certificate, half released at practical completion and the rest after the defects period.

On a £400,000 job, that’s £20,000 sat with someone else’s bank earning interest, while you’ve already paid your suppliers, your team, and your VAT. The Housing Grants, Construction and Regeneration Act 1996 (and the amendments brought by the Local Democracy, Economic Development and Construction Act 2009) gives you statutory rights around payment timetables — but those rights only matter if you know about them and have the contract paperwork to back them up.

A surprising number of contractors I’ve worked with simply accept late payment because they don’t know they have legal recourse. The Pay Less Notice mechanism, the right to suspend performance for non-payment, adjudication under the Scheme — these aren’t theoretical. They’re tools.

Software, MTD, and the spreadsheet problem in construction accounting

Most contractors I meet still run their books on some combination of:

- a battered Excel sheet maintained by the boss’s spouse

- a shoebox of receipts in the van

- WhatsApp messages saying “did we pay him for the Tuesday?”

If that’s you, no judgement. It’s how the trade has worked for decades. But Making Tax Digital has been quietly tightening for years, and from April 2026 it expands further into Income Tax for self-employed individuals and landlords with qualifying income above £50,000 (the threshold drops to £30,000 from April 2027 and £20,000 from April 2028). For most subcontractors operating as sole traders, that means quarterly digital submissions to HMRC through compatible software — not annual self-assessment as it used to be.

Cloud accounting platforms — Xero, QuickBooks, Sage, FreeAgent — all handle CIS, the reverse charge, and MTD reporting reasonably well now. They’re not magic. They still need someone telling them which subbies are verified, what the materials split is on a mixed invoice, whether the customer is an end user. But they remove the worst of the manual error.

At Ask Accountants UK Ltd, the contractors we work with on Cloud Accounting setups generally find that the genuine value isn’t the software itself — it’s having a single source of truth where job costs, subbie deductions, VAT treatment and bank movements all reconcile. The spreadsheet equivalent of that exists, technically. It just demands inhuman discipline.

What separates a decent construction accounting specialist from a generic one

I’ll be direct here, because I think it matters.

Plenty of accountants are perfectly competent. They’ll file your accounts on time, your tax return won’t be late, and your annual confirmation statement will be in. That’s a baseline service and it has its place.

A construction accounting specialist should know — without you having to explain it — what a CIS300 looks like, when the reverse charge applies, why your retention figures matter for revenue recognition, and how to structure a subcontractor refund claim so it actually goes through first time. We’ve written more about this in our longer construction accounting explainer if you want the deeper version.

Things to look for in a construction accountant

- They ask about your contracts before quoting fees. A contractor with three live JCT contracts has very different needs from a kitchen fitter doing private domestic work.

- They’re proactive about CIS refunds. Subbies routinely overpay tax through CIS deductions. A single annual refund claim handled properly often pays for the year’s accountancy fees and then some.

- They flag compliance risks before HMRC does. This is the bit that earns its keep. Anyone can clean up after a problem; you want someone who sees it coming.

- They understand the cash flow gap. Generic advice (“just bill faster”) doesn’t survive contact with retention clauses.

Ask Accountants UK Ltd, based at 178 Merton High St, London SW19 1AY, has worked with construction businesses across South West London for a long stretch — handling CIS Claims and Refunds, Bookkeeping, VAT, Self Assessment, and the harder corners of HMRC Investigations when something goes sideways. The full service list runs through Business Advice, Business Plans, Tax Compliance, Personal Tax Planning, Company Secretarial Work, and Automatic Enrolment. If you’d rather have a chat than read another guide, the number is 020 8543 1991 — or drop us a line here.

Construction accounting in motion: a typical contractor’s month

Here’s how the moving parts actually fit together on a typical contractor’s month. (Numbers are illustrative — the shape is what to pay attention to.)

| Activity | Cash Impact | Tax/Reporting Impact | When |

|---|---|---|---|

| Pay registered subbie £5,000 (labour only) | £4,000 leaves bank to subbie + £1,000 deducted | £1,000 owed to HMRC via CIS, deduction statement issued | Within 14 days of payment |

| File CIS300 for the month | Pay over £1,000 to HMRC | By 19th of following month (22nd if paying electronically) | Monthly |

| Issue invoice to main contractor (you’re the subbie) | £10,000 net invoiced — no VAT charged (reverse charge) | VAT return shows £10,000 in Box 6 only | Per project valuation |

| Receive payment with 20% CIS deducted | £8,000 banked — £2,000 already with HMRC | £2,000 credit accruing for year-end refund claim | Per certificate |

| Year-end self-assessment / corp tax return | Refund claim submitted | CIS deductions offset against tax liability — overpayment refunded | Following tax year |

You’ll notice the columns aren’t perfectly tidy. Neither is real-life construction accounting. That’s sort of the point.

Common construction accounting mistakes I see, in roughly the order they cause damage

A short, opinionated list:

- Treating CIS deductions as “lost money.” They aren’t. They’re prepaid tax. Your accountant should reclaim any overpayment every single year. If they don’t, ask why.

- Forgetting to verify subbies before paying them. A new HMRC verification number is required every two tax years per subcontractor. Skip this and the default rate is 30% — and you’re personally on the hook for the missing 10%.

- Mixing labour and materials in a single line on the invoice. Always split them. Materials don’t attract CIS deduction; labour does. Lazy invoicing costs subbies money every month.

- Operating without a written subcontractor agreement. When something goes wrong — disputed work, abandoned project, tools missing — the contract is what saves you. A signed one-pager beats a WhatsApp thread every time.

- Believing that “I’m the small guy in the chain” protects you from the new fraud powers. It doesn’t. Joint and several liability under the April 2026 rules can land on anyone HMRC can argue “should have known.” Due diligence is the only shield.

Construction accounting FAQs

Do I need to register for CIS if I only do small jobs?

If you’re a contractor (you pay subcontractors for construction work), you must register regardless of size. If you’re a subcontractor, registration isn’t strictly mandatory, but unregistered subbies face 30% deductions instead of 20% — registering nearly always pays for itself in cash flow alone.

What counts as “construction” for CIS purposes?

Broadly: site preparation, alterations, dismantling, repairs, installation, painting, decorating. The full list in HMRC’s CIS340 guidance is long. Architects, surveyors, and pure equipment hire (without an operator) generally fall outside.

Can I run construction accounting on a spreadsheet?

Technically yes. Practically, with MTD expanding through 2026 and 2028, and given how easily CIS and reverse charge errors compound, cloud accounting software with a competent bookkeeper behind it is dramatically less stressful.

What’s the most common reason contractors get a CIS penalty?

Forgetting to file a nil return when no subbies were paid. From April 2026 this becomes a much sharper risk.

When should I bring in a construction accounting specialist rather than DIY?

Honestly? The moment you take on your first subcontractor, or when your turnover passes the VAT registration threshold, or the second you get an HMRC letter you don’t fully understand. The cost of professional construction accounting support is almost always less than the cost of fixing what gets missed.

A few last words on construction accounting in 2026

Construction accounting isn’t going to get simpler in 2026. The opposite, really — more reporting obligations, sharper enforcement, less patience from HMRC, and supply chain rules that force every contractor to think harder about who they work with.

But it’s manageable. It just rewards preparation in a way that other industries don’t quite demand.

If you’re sitting with a stack of paperwork and a vague sense that something’s not right — or you’re staring down April 2026 wondering what to do about your subbie verification process — the conversation is usually shorter than you’d expect. Ask Accountants UK Ltd on 020 8543 1991 has been having that conversation with London contractors for years. Sometimes that’s all it takes to stop the small thing becoming the expensive thing.

The boots, the dust, the early starts — that’s your bit. The construction accounting numbers don’t have to be.