Nobody wakes up excited to fill in an HMRC schedule. Especially not one that asks you to reconstruct seven years of someone’s gifting history while you’re still grieving them. Yet here we are — the IHT403 sits quietly inside the inheritance tax pile, and ignoring it (or fudging it) can cost an estate tens of thousands.

I’ve watched executors stare at this form like it’s written in Aramaic. The boxes look harmless. The questions read plainly enough. Then you hit the income-and-expenditure schedule on page 6 and suddenly you’re trawling through bank statements from 2019 trying to remember if Aunt Marjorie’s “small Christmas top-up” was £200 or £2,000.

So let’s pull the IHT403 apart, slowly, and make it make sense.

What this form actually does (and why HMRC cares so much)

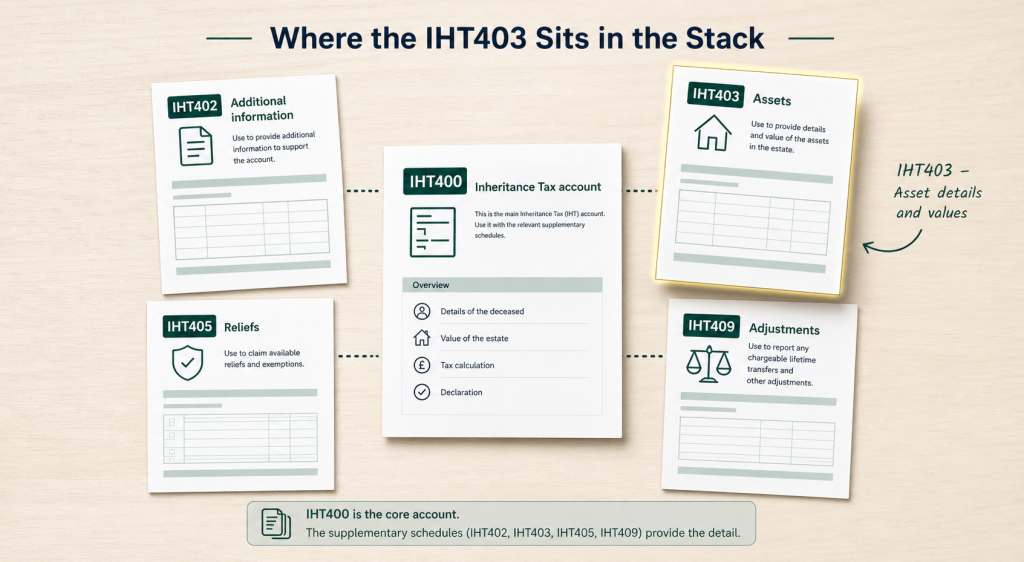

The IHT403 is a schedule — a supplementary page that bolts onto the main IHT400 inheritance tax return. Its job is narrow but important: it tells HMRC about every meaningful gift the deceased made in their lifetime, with particular focus on the seven years before they died.

Why seven years? Because that’s the magic window. Gifts made and survived by seven years generally drop out of the estate altogether. Die sooner, and the taxman wants a chat. The IHT403 is where that chat begins.

You’ll also use this form to flag:

- Gifts with reservation of benefit — the classic “I gave my house to the kids but kept living in it rent-free” scenario, which HMRC famously dislikes

- Pre-owned assets caught by the POAT rules

- Chargeable lifetime transfers (think gifts into discretionary trusts)

- Regular gifts made out of surplus income — possibly the most argued-about part of the whole document

Now, a slightly uncomfortable truth: executors are personally liable if HMRC later discovers gifts that weren’t declared. A year after death, that liability shifts and grows teeth. So the IHT403 isn’t a “best efforts” form. It’s a duty.

When you actually need to fill one in

You need the IHT403 alongside an IHT400 if the deceased — at any point on or after 18 March 1986 — gave away assets, made transfers into trust, or kept benefiting from something they’d “given” to someone else. That’s a wide net. Most estates above the nil-rate band end up needing it.

If the estate is excepted (small, simple, no substantial gifting), you might escape with just the lighter forms. But the moment gifts are in the picture, the IHT403 walks in with them.

For a wider primer on which inheritance tax forms apply to which situations, our help filling in inheritance tax forms page lays it out without the jargon.

What counts as a “gift” — and what people get wrong

This trips up almost every first-time executor I’ve spoken with. HMRC’s definition is broader than the everyday one. A gift, for IHT403 purposes, includes:

- Cash transfers (obvious)

- Selling property to a relative for less than market value (the discount is the gift)

- Setting up trusts

- Forgiving a debt

- Paying someone’s school fees, mortgage, or rent regularly

- Adding a name to a property title

- Transferring shares or investments

What it does not include — and this is where you reclaim some sanity — are gifts covered by automatic exemptions. The £3,000 annual allowance. Small gifts of up to £250 per person per tax year. Wedding gifts within the published limits. Gifts between UK-domiciled spouses (unlimited). Gifts to qualifying charities and political parties.

These still get listed on the IHT403, mind you. You just claim the exemption against them. The form has a column for that.

| Type of gift / exemption | Annual limit | Goes on IHT403? |

|---|---|---|

| Annual exemption | £3,000 per donor | Yes — listed and offset |

| Small gifts | £250 per recipient | Usually no, unless contested |

| Wedding gifts (parent → child) | £5,000 | Yes, with exemption claim |

| Wedding gifts (grandparent) | £2,500 | Yes |

| Spouse/civil partner gifts (UK domiciled) | No limit | Generally no |

| Normal expenditure out of income | No fixed limit — must be from surplus | Yes — full schedule required |

| Charity / political party | Unlimited (qualifying) | Yes, with reference details |

Quick warning, said as plainly as possible: if you “forget” gifts and HMRC later finds them through their Connect database (which cross-references bank transfers, Land Registry records, and trust returns), penalties run from 0% to 100% of the extra tax. Deliberate concealment? You’re at the top of that scale. Don’t risk it.

Walking through the form, page by page

The IHT403 is currently eight pages on the HMRC version. It looks intimidating because it tries to capture five different types of transfer in one document. Once you know which questions apply to your situation, two-thirds of the form becomes irrelevant.

Page 1 — the gateway questions

Boxes 1 to 6 are yes/no triage. Did the deceased make gifts in the seven years before death? Did they give anything they kept benefiting from? Were there pre-owned assets? Any chargeable transfers earlier than seven years? Did they regularly give from surplus income?

Tick honestly. Each “yes” routes you to a different section deeper in the form. Tick “no” to all of them and the IHT403 finishes itself, which would be lovely but rarely happens for estates large enough to need an IHT400 in the first place.

Pages 2–4 — the gifts schedule

This is the heart of the IHT403. Every gift made within seven years of death gets its own row. You’ll need:

- Date of gift — exact, not approximate. HMRC will ask.

- Name and relationship of recipient — who got it

- Description — cash, shares, property, jewellery, “interest-free loan written off”, etc.

- Value at the date of gift — not today’s value, the value when given

- Type of exemption or relief — annual allowance, marriage gift, BPR, APR, charity, etc.

- Net value after exemption

A common error here: people forget that when HMRC updated the form in April 2026, the “Type of exemption or relief” column was reformatted to align with the new agricultural and business relief rules. If you’re working from an older saved PDF, you might be using an outdated layout. Always pull a fresh copy.

Pages 5–6 — the income and expenditure schedule

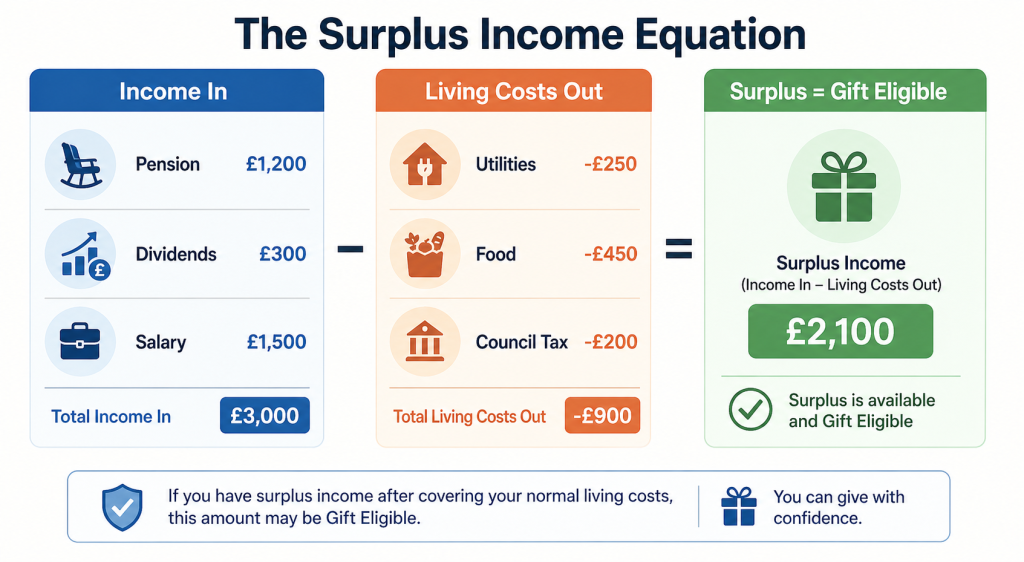

This is where executors lose entire weekends. If the deceased was making regular gifts and you want HMRC to accept them as “normal expenditure out of income” (which makes them immediately exempt — no seven-year wait), you need to reconstruct their finances year by year.

The columns ask for income, broken down into salary, pensions, dividends, interest, rental income, business profits. Then expenditure — the everyday cost of living. Mortgage, council tax, utilities, food, holidays, clothing, insurance, transport, healthcare, household goods, “other”.

Whatever’s left is surplus. The argument is: gifts made out of that surplus, on a regular pattern, didn’t reduce the donor’s standard of living, so they should escape IHT entirely.

Three things HMRC really wants to see here:

- A pattern. Three or four years of similar gifts is the unofficial benchmark.

- Genuine surplus. Not income they were going to spend anyway.

- No erosion of capital. If the “surplus” was actually being topped up from savings, the exemption fails.

The case of McDowall and others established that gifts from accumulated income (income that’s been sitting in a bank account for too long) can lose their character as income and become capital. HMRC generally treats anything older than two years as capital. So timing matters.

Pages 7–8 — gifts with reservation, pre-owned assets, chargeable transfers

The tail end of the form catches edge cases. Reservation of benefit is the big one. If the deceased gave away their home but continued to live in it rent-free, the gift was never really a gift in HMRC’s eyes. The full value comes back into the estate. Period.

If they later started paying market rent, or moved out (say into a care home), the reservation may have ended. You’d record the date of that change here and it becomes a potentially exempt transfer from that point forward.

The bit that confuses everyone: taper relief

Almost every conversation I have about lifetime gifts on the IHT403 includes someone confidently telling me about taper relief — and getting it wrong.

Here’s the truth, plainly: taper relief reduces the tax, not the gift.

If a gift is fully covered by the £325,000 nil-rate band, taper relief gives you exactly nothing. Zero benefit. The relief only kicks in on the excess value above the nil-rate band, on gifts made between three and seven years before death.

| Years between gift and death | Taper reduction | Effective tax rate on excess |

|---|---|---|

| 0–3 years | None | 40% |

| 3–4 years | 20% | 32% |

| 4–5 yrs | 40% | 24% |

| 5 to 6 | 60% | 16% |

| 6–7 years | 80 % | 8% |

| 7+ years | Full exemption | 0% |

When you fill in the IHT403, don’t try to apply taper yourself. The form calculates tax at the headline rate first. HMRC then applies taper at the assessment stage. If the on-screen calculation looks scary, that’s why — keep going.

Records: the executor’s secret weapon (or worst nightmare)

Here’s something I wish more people understood while they were alive: the IHT403 is much, much easier to complete if the donor kept records.

Page 6 of the form is essentially a template. You can use it as a living document. Note each gift as you make it — date, recipient, amount, exemption claimed. Track income and expenditure annually. Keep a folder, digital or paper, doesn’t matter.

When you die, your executor doesn’t have to guess. They open the folder. They copy the figures across. The whole thing is done in an afternoon instead of three months of detective work.

If you’re already advising older people or thinking about your own legacy, our team often helps families set up gifting logs alongside their broader personal tax planning — it’s the kind of small admin task that pays back enormously down the line.

A real-world tangle (and how it got untangled)

Couple of years ago, a client came to us mid-panic. Father had passed. Estate worth roughly £1.2m. He’d been giving each of his three grandchildren £400 a month for the last six years out of his pension income — about £86,400 in total across all three. The family assumed those gifts would all be added back as failed PETs and taxed at 40%.

They wouldn’t have been. Those gifts were a textbook case of normal expenditure out of income. Regular. Modest relative to his £55,000 annual pension. Surplus to his (very frugal) outgoings.

But there were no records. No spreadsheet. No annual income statement. Just a vague memory and some bank statements going back four years.

We rebuilt the schedule from those statements, his SA302s, his utility direct debits, and a pretty creative reconstruction of his weekly shopping habits. HMRC accepted the exemption. The estate saved roughly £34,000 in IHT.

It worked because we caught it early and because there was some paper trail. With nothing at all, we’d have lost.

Common mistakes that delay the IHT400 process

A few patterns keep cropping up. In rough order of frequency:

- Listing gifts at today’s value rather than the value on the date given

- Forgetting “favours” — paying for a kitchen renovation, covering a deposit, writing off a loan

- Claiming the £3,000 annual exemption twice in the same year

- Treating school fees as exempt automatically (they’re not — they need to qualify under either a settlement for the child or normal expenditure rules)

- Missing reservation of benefit on jointly held assets

- Skipping page 6 entirely because it “looked optional” — it isn’t, if you’re claiming surplus income exemption

- Submitting outdated versions of the IHT403

Mistakes like these often surface when HMRC compares your numbers against their internal cross-references and writes back asking awkward questions. Which is the slow, expensive route to the same answer you could’ve reached first time.

If you’re already mid-form and stuck, our IHT400 form complete guide walks through how the whole inheritance tax return fits together, with the IHT403 as one critical schedule among several.

A few questions people keep asking

Can I fill in the IHT403 online? Not as a standalone digital form right now. You download the PDF from gov.uk, complete it (you can type into it before printing), and submit it as part of the IHT400 paper bundle. HMRC has been gradually digitising parts of the inheritance tax process, so this may change — worth checking the GOV.UK IHT403 page for the latest version.

Do I need to list gifts going back further than seven years? Generally no, with one exception: chargeable lifetime transfers (typically gifts into trust) made in the seven years before any failed PET. These can affect the available nil-rate band and need to go on the form even if they’re older than seven years from death.

What if I genuinely don’t know what gifts were made? You make reasonable enquiries — bank statements, Christmas card mentions, conversations with family. Document what you’ve checked. HMRC understands that perfect records aren’t always possible. They’ll be considerably less understanding if you didn’t even try.

Are wedding gifts always exempt? Up to the limits, yes — but they need to be made before the wedding and conditional on it taking place. A gift given at the reception is timed correctly; one given six months later isn’t a wedding gift in HMRC’s eyes.

What happens to the IHT403 if the estate is below the nil-rate band? You may not need a full IHT400 at all. Excepted estates can use the simpler IHT205 process (now largely replaced by the online “tell us once” route for deaths since 2022). But the moment lifetime gifts push the picture closer to the threshold, the IHT403 becomes relevant again.

Can the IHT403 be amended after submission? Yes. If you discover gifts later, write to HMRC’s Trusts and Estates office with the corrected information. Doing this voluntarily, before they ask, hugely reduces any penalty exposure.

When it’s time to call someone in

Plenty of estates can be handled by competent, patient executors with a calculator and a cup of tea. Plenty can’t. The IHT403 starts to feel genuinely treacherous when:

- The deceased ran a business or owned shares in a private company (BPR, APR — different forms entirely)

- There’s a property gifted with continued occupation

- Trusts are involved

- Gifts cross several jurisdictions

- Family members disagree about what was a loan vs a gift

- HMRC has already opened correspondence and started asking pointed questions

That’s where having an accountant in your corner stops being optional. Ask Accountants UK Ltd has been working with families across South West London on inheritance tax matters for years — alongside the broader bread-and-butter work of accounts and tax, self assessment, bookkeeping, HMRC investigations and personal tax planning. The phone number, if you’d rather just talk it through with someone who’s seen all this before, is 020 8543 1991, and we’re based at 178 Merton High St, London SW19 1AY.

You don’t have to take it on alone. The IHT403 is one of those forms that rewards experience disproportionately — a couple of hours with someone who’s filled in fifty of them can save you thirty hours of fumbling and possibly a five-figure tax bill that didn’t need to exist.

For wider context on reducing the tax bill itself rather than just reporting it, our notes on strategies for reducing inheritance tax on family property and our IHT tax planning guide are worth a read.

The IHT403 isn’t really a form. It’s a story — the financial story of someone’s later years, told in numbers and dates and the names of people they loved enough to give things to. Telling that story properly is the last quiet kindness an executor performs. Worth getting right.