Nobody becomes a landlord because they love paperwork. You bought the flat in Streatham, or inherited Auntie Margaret’s terrace in Tooting, or scraped together a deposit for a buy-to-let — and suddenly working out how to report rental income to HMRC has become a Sunday-evening anxiety, complete with a mug of cold tea and that unopened brown envelope on the kitchen counter. SA105. UTR. MTD. The HMRC alphabet soup.

Here’s the awkward truth: HMRC already knows. Your name’s on Land Registry, deposit protection schemes get cross-referenced, and since 2024 they’ve been pulling data from letting agents and short-term rental platforms with the enthusiasm of a Labrador at dinner time. So “I’ll deal with it later” is not, as strategies go, a particularly clever one.

This guide walks you through how to report rental income to HMRC properly — what counts as income, what you can deduct, when the deadlines bite, and where the new Making Tax Digital rules sit in the picture. I’ve tried to keep the jargon to a minimum. Where it sneaks in, I’ll explain it.

Who actually has to declare rental income to HMRC?

Short answer: most people who let property. Longer answer needs a quick maths check.

If your gross rental income (that’s everything before you subtract anything) is £1,000 or less for the tax year, you don’t have to declare it at all. This is the property allowance — a quiet little exemption that HMRC introduced to spare itself (and you) the admin of trivial amounts. Renting your driveway out for a tenner a week during football season? Probably fine. A parking space let to your neighbour for £80 a month? Still fine.

Cross that £1,000 threshold, though, and the rules switch on:

- If gross income sits between £1,001 and £2,500 after deducting expenses, HMRC can sometimes collect through your tax code via PAYE — but you need to ring them and ask. They won’t volunteer it.

- Over £2,500 in profit (income minus allowable expenses), or over £10,000 gross regardless of profit — you’re filing a Self Assessment return. No way around it.

The Rent a Room Scheme is the one genuinely generous exception. Let a furnished room in your own home and the first £7,500 of rent is tax-free. Pop someone in your spare bedroom and you can take in a lodger without HMRC sniffing around — provided you don’t exceed the limit.

⚠️ A small warning that’s saved a lot of headaches: Even if you’ve made a loss, you should still tell HMRC. Losses carry forward against future rental profits, which means you can offset them later. Skip declaring a loss-making year and you might discover, five years on, that you’ve forfeited thousands in potential relief. Daft. Don’t do it.

Registering for Self Assessment — the bit everyone leaves too late

Right. So you’ve worked out you need to file. Now what?

If you’ve never filed a tax return before, you need to register with HMRC. You’re chasing a thing called a UTR — Unique Taxpayer Reference — a ten-digit number that’s basically your tax fingerprint. The deadline is 5 October following the tax year in which you first earned the rental income. So if you started renting out in October 2024, registration should’ve been done by 5 October 2025.

Miss that and HMRC won’t necessarily fine you straight away, but they will if your tax ends up paid late as a consequence. Registration itself takes about ten working days, and your UTR arrives by post (yes, an actual letter — HMRC has its quirks). Allow a fortnight, don’t leave it until late January, and you’ll be fine.

You can register through the HMRC online services portal or have an accountant do it for you. If you’d rather not wrestle with the website, that’s where firms like Ask Accountants UK Ltd come in handy — we handle the registration as part of our self-assessment service, and you get to skip the back-and-forth phone queues.

How to report rental income to HMRC using the SA105 form

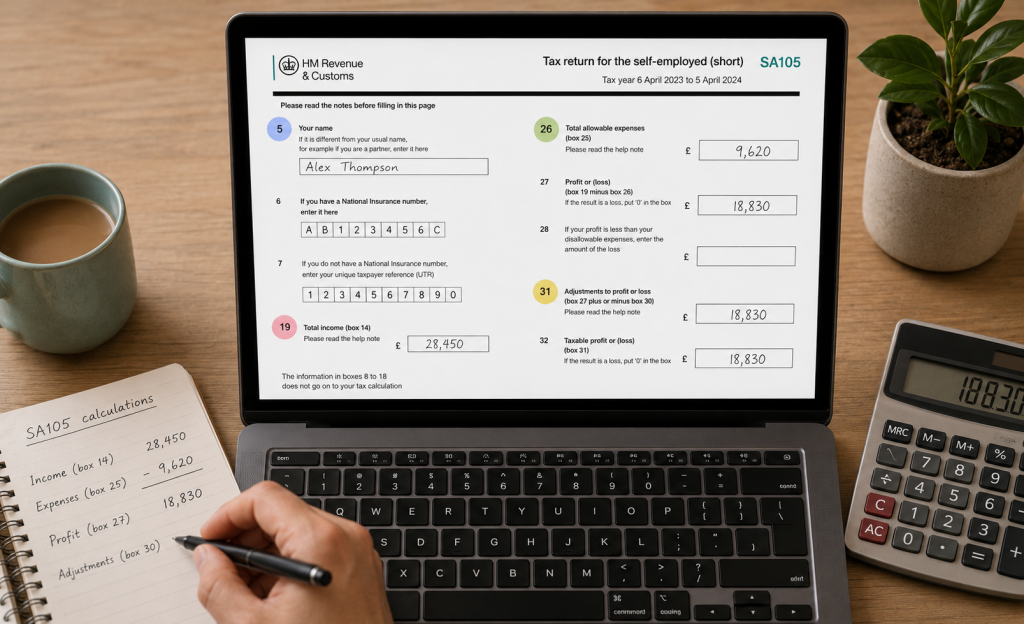

Here’s where the actual mechanics get specific. The main Self Assessment form is the SA100 — that’s the catch-all return covering employment, self-employment, dividends, the lot. Property income gets its own supplementary page: the SA105.

File online and you won’t physically see the SA105 — it’s baked into the digital return as a section you tick on. Paper filers download the form from gov.uk and post it in with the SA100. Either way, the same boxes need filling.

The numbers that matter most:

- Box 5 — Total rents received (everything before deductions)

- Box 19 — Total allowable expenses (excluding mortgage interest)

- Box 26 — Residential property finance costs (this is where mortgage interest goes — but not as an expense, more on that in a moment)

- Box 31 — Profit or loss

One form per type of property income. Got a buy-to-let and a holiday let? That’s potentially separate forms. UK property only — overseas rentals go on SA106.

The deadlines you cannot afford to forget

| What’s due | When for 2024/25 tax year | When for 2025/26 tax year | Penalty for missing |

|---|---|---|---|

| Register for Self Assessment | 5 October 2025 | 5 October 2026 | Tied to late tax — no fixed fine |

| Paper tax return | 31 October 2025 | 31 October 2026 | £100 instant fine |

| Online tax return + pay tax owed | 31 January 2026 | 31 January 2027 | £100 + daily £10 fines after 3 months |

| First payment on account | 31 January 2026 | 31 January 2027 | Interest from due date |

| Second payment on account | 31 July 2026 | 31 July 2027 | Interest from due date |

Late filing penalties stack up the way overdue library books did before libraries gave up: £100 the moment you’re a day late, then £10 per day from three months in (capped at 90 days, so up to £900), then 5% of tax owed or £300 (whichever’s higher) at six months, and another helping at twelve. Add interest on the unpaid tax itself and you can quickly be staring at four figures of pure faff money.

A useful piece on the 2025/26 Self Assessment key dates breaks it all down properly.

What you can actually deduct (and what you absolutely cannot)

This is where most landlords leave money on the table. The expenses below are deductible against rental income, provided they’re wholly and exclusively for the rental business:

- Letting agent fees and management charges — fully allowable

- Property repairs and maintenance — like-for-like only; replacing a broken boiler, yes; installing your first ever loft conversion, no (that’s capital)

- Insurance premiums — buildings, contents, landlord-specific cover

- Utility bills — only if you pay them, not the tenant

- Council tax and ground rent — when you’re liable

- Accountancy fees — yes, including the cost of preparing the tax return itself

- Travel costs to the property — keep a mileage log

- Service charges, gardening, cleaning between tenants

- Advertising for new tenants

- Replacement of domestic items (sofas, beds, white goods) — but only replacements, not the original kit

Improvements that change the character of the property — extensions, new kitchens that are noticeably better than the old one, conversions — they’re capital expenses. You can’t deduct them now, but they reduce your Capital Gains Tax bill when you sell.

Here’s a comparison most people find useful when choosing between claiming actual expenses or just taking the property allowance:

| Scenario | Gross rent | Actual expenses | Better option | Taxable profit |

|---|---|---|---|---|

| Spare room, very few costs | £3,500 | £200 | Property allowance (£1,000) | £2,500 |

| Buy-to-let, agent managed | £14,400 | £4,200 | Actual expenses | £10,200 |

| Small flat, self-managed | £8,400 | £750 | Property allowance | £7,400 |

| Lodger via Rent a Room | £7,200 | n/a | Rent a Room Scheme | £0 |

(You can claim the property allowance OR actual expenses — not both. And it isn’t available if you let through your own limited company.)

The mortgage interest thing that catches everybody out

Until 2017, landlords could deduct mortgage interest from rental income before calculating tax. Lovely. Then George Osborne dropped Section 24 on us, and it’s been phased in ever since.

Here’s the current position: mortgage interest is no longer an allowable expense. Instead, you get a 20% tax credit on the interest you’ve paid. Sounds similar — it really isn’t.

For a basic-rate taxpayer it works out roughly the same. Higher-rate (40%) and additional-rate (45%) taxpayers feel a meaningful tax hike, because your rental profit (and therefore your headline taxable income) goes up. That can push you into the next tax bracket, reduce your personal allowance if you cross £100,000, and play merry with child benefit if you’ve got kids.

This is one of the reasons many landlords now ask whether holding property through a limited company makes more sense — companies can still deduct mortgage interest as an expense. It’s not the right answer for everyone, but if you’re in the higher-rate bracket and growing a portfolio, it’s a conversation worth having with someone who knows property accounting properly.

Joint owners, spouses, and the 50/50 default

Owning a property with your spouse or civil partner? HMRC assumes you each receive 50% of the income, regardless of who actually owns what share. Even if the deeds say one of you owns 80%.

To change that split, you both file Form 17 and prove the actual beneficial ownership. This is genuinely useful where one partner pays a lot more tax than the other — shifting income to the lower earner can save real money.

Unmarried co-owners? Income gets split according to actual ownership shares unless you’ve agreed otherwise in writing.

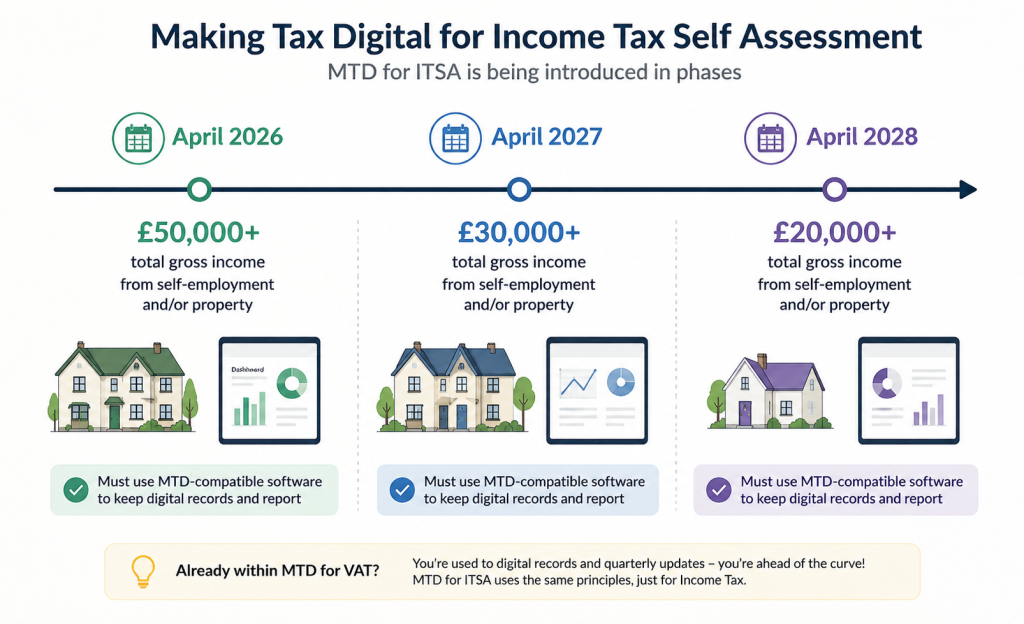

How Making Tax Digital changes the way you’ll report rental income to HMRC

Here’s where 2026 gets interesting. From 6 April 2026, landlords with combined gross self-employment and property income above £50,000 must use Making Tax Digital (MTD) compatible software, keep digital records, and submit quarterly updates to HMRC.

It’s not a different amount of tax. It’s a different way of telling HMRC about it.

The phasing looks like this:

- April 2026 — £50,000+ gross income

- April 2027 — £30,000+ gross income

- April 2028 — £20,000+ gross income

Got gross rent over £50,000 and still using a shoebox of receipts and a notebook? You’re already non-compliant. Cloud software like QuickBooks for landlords handles MTD submissions natively, and the Ask Accountants UK Ltd cloud accounting team can get you set up in an afternoon. Quarterly updates aren’t optional, and penalties for non-compliance are coming.

Worth flagging too: the abolition of the Furnished Holiday Lettings regime from April 2025. Ran Airbnbs or short-stay lets? Those special rules (FHL capital allowances, mortgage interest deductibility, advantageous CGT treatment) are gone. You’re now just a regular landlord in HMRC’s eyes.

What to do if you haven’t been declaring — the Let Property Campaign

This bit’s important, so I’ll be blunt. Letting property and not telling HMRC? You’ve got a problem that’s getting bigger, not smaller. HMRC’s Let Property Campaign is a voluntary disclosure route — come forward, pay what you owe (with reduced penalties), and avoid criminal investigation.

Compare that to what happens when HMRC opens an enquiry first. Penalties of up to 100% of the unpaid tax. Up to 20 years of back-tax recovery for deliberate behaviour. Public naming under the deliberate defaulter scheme. None of it’s fun.

Please don’t bury your head if this is you. Get advice. Discreet, professional, and yes — confidential. The team at Ask Accountants UK Ltd has handled plenty of HMRC investigations and disclosures, and the conversation is always easier than people expect.

Common mistakes when learning how to report rental income to HMRC

💡 The five errors that cost landlords the most money:

- Treating mortgage interest as a deductible expense (it isn’t, since 2020 — it’s a 20% credit)

- Claiming improvements as repairs (HMRC will spot a new kitchen masquerading as a “repair”)

- Not declaring losses (which means losing the right to offset them later)

- Forgetting the £1,000 property allowance exists, and missing the chance to choose

- Splitting joint property income 50/50 when one partner pays much less tax (Form 17 fixes this)

Two more, while we’re here. Many landlords forget that deposits kept for damages are taxable income in the year you keep them. And anyone using letting agents should double-check whether agent fees have been deducted before or after the figure that lands in your bank — you need the gross rent, not the net.

When to throw your hands up and call someone

You can absolutely file a property tax return yourself. Plenty of landlords do, and HMRC’s online portal is functional enough. But there are a few situations where the cost of professional help pays for itself many times over:

- You own three or more properties

- You’re a higher-rate or additional-rate taxpayer

- You’ve got mortgage interest and want to model the Section 24 impact

- You’re considering moving properties into a company

- You haven’t filed and need to come forward via the Let Property Campaign

- You’ve had a letter from HMRC opening an enquiry

- You’re crossing the MTD threshold and need to digitise

Working out exactly how to report rental income to HMRC for complex portfolios is what property-focused accountants do every day. Based at 178 Merton High Street in Wimbledon, Ask Accountants UK Ltd works with landlords across London on everything from one-off SA105 filings to full portfolio management — including bookkeeping, MTD-ready cloud accounting, personal tax planning, and HMRC compliance. For a quick chat about your situation, give us a ring on 020 8543 1991 or drop a message through the contact form.

No hard sell — half the people who call end up filing themselves with a bit of reassurance, which is fine by us.

Frequently Asked Questions

Reporting basics

Do I need to declare rental income if I make a loss? Technically no, if your gross income is under £1,000. But yes if it’s over — and you should want to, because declared losses can be carried forward to offset profits in future tax years. Skipping the return forfeits that right.

How do I report rental income to HMRC if I only let out one room in my house? With gross rental income from the room at £7,500 or less, you use the Rent a Room Scheme and pay no tax — no Self Assessment return needed unless HMRC has asked you for one. Above £7,500, Self Assessment kicks in and you choose whether to declare the excess over £7,500 as taxable, or report the room income normally with expenses.

Does HMRC actually know about my rental property? Almost certainly, yes. They pull data from Land Registry, deposit protection schemes, letting agents, Airbnb and similar platforms, and council tax records. Whether they’ve acted on it is a different question — but assuming they don’t know is the kind of optimism that ends in penalties.

Deadlines and registration

Can I report rental income through PAYE instead of Self Assessment? Only if your profit (income minus allowable expenses) is under £2,500 and you already pay tax through PAYE on a salary or pension. Ring HMRC and ask them to adjust your tax code. Above £2,500 profit, Self Assessment becomes mandatory.

What’s the deadline to register if this is my first year as a landlord? Registration for Self Assessment must happen by 5 October following the end of the tax year in which you started receiving rental income. For income earned during 2025/26, that’s 5 October 2026.

What happens if I miss the 31 January deadline? A £100 instant penalty applies even if you owe no tax. After three months, £10 per day for up to 90 days kicks in. After six months, another 5% of unpaid tax or £300, whichever is higher and after twelve months, the same again. Plus interest on the tax itself. Don’t.

Tax rates and calculations

How much tax will I pay on rental income? Rental profit gets added to your other taxable income and taxed at your marginal rate: 0% up to your personal allowance (£12,570), 20% basic rate to £50,270, 40% higher rate to £125,140, then 45%. From April 2027, property income will have its own slightly higher rates (basic 22%, higher 42%) following the Autumn 2025 budget.

Getting professional help

Do I need an accountant to report rental income to HMRC? No, but it often pays for itself. For straightforward single-property situations, DIY filing through the HMRC portal works fine. For multiple properties, higher-rate taxpayers, mortgage-heavy portfolios, or anyone worried about the new MTD quarterly reporting, an accountant typically saves more than they cost.