Nobody wakes up excited to pay HMRC. Yet every year, thousands of perfectly profitable UK companies hand over more corporation tax than they actually owe — not through fraud, not through carelessness, but because they never got round to using the reliefs Parliament wrote into law specifically for them. This guide is about how to reduce corporation tax legally in the UK, using the actual rules HMRC publishes, the allowances the Treasury actively wants you to claim, and a bit of joined-up thinking your competitors probably haven’t bothered with.

Here’s the slightly awkward bit. The phrase “tax avoidance” makes people flinch. It shouldn’t. Avoidance — staying within the rules to pay less — is legal, encouraged in many cases, and entirely different from evasion (which is the kind that ends with a knock on the door from HMRC and a stay at His Majesty’s pleasure). Everything in this article sits firmly on the legal side of that line.

Quick note before we dive in: This is general guidance, not personalised advice. Your numbers, your trade, your structure all matter. When you’re ready to apply this properly, our team at Ask Accountants UK Ltd handles the awkward bits.

The Lay of the Land — What You’re Actually Being Charged

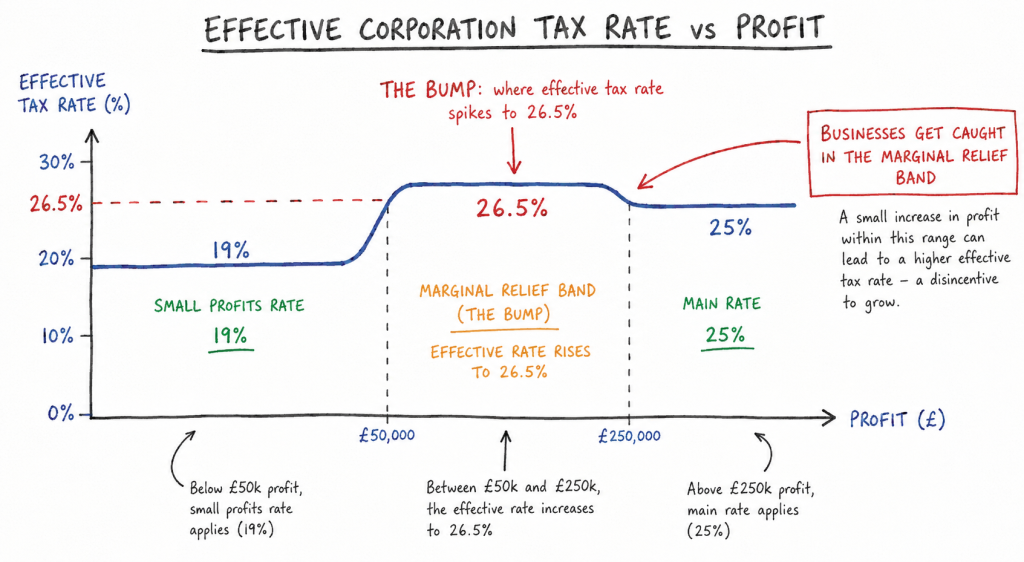

Before anyone starts hunting reliefs, it’s worth knowing what your bill should look like under the current dual-rate regime. The rates haven’t budged since April 2023, and the Autumn Budget 2025 confirmed they’re holding steady through 2026/27 too.

| Profit Band | Rate | What’s Going On |

|---|---|---|

| Up to £50,000 | 19% (Small Profits Rate) | Around 70% of UK companies sit here |

| £50,001 – £250,000 | Marginal Relief band — effective 26.5% on the slice in this band | Yes, the marginal rate is *higher* than the main rate. Quirky, isn’t it? |

| Over £250,000 | 25% (Main Rate) | Standard headline rate |

That marginal band catches a lot of growing businesses by surprise. A pound earned between £50k and £250k of profit is taxed harder than a pound earned at £300k. Bizarre, yes — but it shapes a lot of the planning that follows. (And those £50k/£250k thresholds get carved up between associated companies, which trips up family-run groups all the time.)

You can read HMRC’s official rates here: GOV.UK Corporation Tax rates.

Squeeze Every Penny Out of Allowable Expenses

I’ll be blunt. The single biggest reason small companies overpay is that they never bother writing down the small stuff.

Allowable expenses are costs incurred wholly and exclusively for the trade. Each one reduces your taxable profit pound-for-pound. Most directors remember rent, salaries, software, stock. They forget:

- Mobile phone contracts in the company’s name

- Use-of-home costs (a flat rate or a fair apportionment)

- Trade subscriptions, professional body fees, industry magazines

- Training that maintains or updates existing skills

- Bank charges and finance costs

- Mileage for genuine business journeys (45p per mile for the first 10,000 miles in a personal car)

- Eye tests for VDU users, certain medical screenings, first-aid kits

- Christmas parties up to £150 per head (yes, really — annual function exemption)

- Trivial benefits at £50 a pop for staff and directors (more on that in a minute)

A decent bookkeeping system catches the lot. A shoebox of receipts does not. If yours leans more shoebox than software, our bookkeeping service and cloud accounting setup will plug the leak.

Capital Allowances — The Quiet Workhorse

If your company buys equipment, vehicles (the right kind), machinery, computers, fixtures — anything with a useful life beyond a year — you’re in capital allowance territory. Done well, this is where serious tax can disappear.

Full Expensing: Buy It, Deduct It, Done

Full expensing gives UK limited companies a 100% first-year deduction on qualifying new plant and machinery. No spreading over years, no fiddly reducing-balance maths. A £200,000 server farm purchase? You drop your taxable profit by the full £200,000 in the year you buy it.

It was made permanent. That matters — because most reliefs come with sunset clauses, and this one no longer does.

Annual Investment Allowance (AIA)

The AIA gives £1 million of immediate relief per year on qualifying expenditure, and unlike full expensing, it covers second-hand kit. For most SMEs, AIA does the job nicely. It also extends to fixtures within commercial property — fire alarms, lifts, certain electrical systems — which a property accounting specialist can carve out of a building purchase you didn’t realise was tax-relievable.

What’s Changing in 2026

Pay attention here, because this one matters. From 1 April 2026, the writing-down allowance on the main pool drops from 18% to 14%. To soften that, the Chancellor introduced a new 40% First-Year Allowance for main rate expenditure, available to companies, sole traders and even leasing providers (which is the genuinely novel bit).

Translation? If you’ve got capital spend coming up and your full expensing/AIA capacity is already used up, the new 40% FYA gives you accelerated relief that didn’t exist last year. Time your purchases.

R&D Tax Relief — Still Generous, Just Different Now

Plenty of business owners hear “R&D” and picture lab coats and pipettes. Wrong picture. HMRC’s definition is broader: any project seeking an advance in science or technology by resolving real uncertainty. A bespoke software build that solves a genuinely tricky integration problem can qualify. So can a manufacturing process tweak that nobody else has cracked.

The schemes were merged from 1 April 2024 into a single regime. Two flavours to know about:

- Merged Scheme RDEC — a 20% taxable above-the-line credit. After 25% corporation tax on the credit, that’s an effective benefit of roughly 15p per £1 of qualifying R&D spend for profitable companies.

- Enhanced R&D Intensive Support (ERIS) — for loss-making SMEs spending 30% or more of total expenditure on R&D. Effective cash benefit lands around 27% of qualifying spend — one of the most generous innovation incentives anywhere.

⚠️ Watch this carefully: Since April 2023, you must notify HMRC in advance of intent to claim if you’re a first-time claimant (or haven’t claimed in three years). Miss that window and the entire claim is dead. No appeal, no second chances. It’s caught out more companies than I’d like to admit.

HMRC’s guidance on the merged scheme lives here.

Pensions: The Director’s Best-Kept Secret

Employer pension contributions are an allowable expense — for the company and for the director receiving them, within annual allowance limits. Pump £40,000 from company funds into a director’s SIPP and you’ve shifted £40,000 from taxed retained profit into a tax-sheltered pension wrapper. No NIC, no income tax, no dividend tax. Just a clean deduction.

The wholly-and-exclusively test still applies — the contribution needs to be justifiable as remuneration for the work done — but for most owner-directors, it is. This is one of the cleanest ways to reduce corporation tax legally while genuinely improving your own future. Two wins, same cheque.

Read more about our personal tax planning approach, which ties this together with director extractions.

Salary, Dividends, and the Art of Mixing the Two

This isn’t strictly a corporation tax reduction — it’s a total tax burden play that affects what you keep. Most owner-directors pay themselves a modest salary (often the NI threshold) and top up with dividends. The salary is a corporation-tax-deductible expense; the dividend isn’t, but dividend tax rates are gentler than income tax + NI on the same money.

The sweet spot moves each year. Take advice — what worked in 2022/23 doesn’t necessarily fit 2025/26.

Trivial Benefits, Staff Perks, and the Little Stuff That Adds Up

Section 323A ITEPA 2003 lets you give staff (and directors of close companies, capped at £300 a year) gifts of up to £50 that are tax-free, NIC-free, and corporation-tax-deductible. Birthday vouchers. Christmas hampers. A bottle of something nice when a deal closes. The rules are pernickety — it can’t be cash, can’t be a reward for work, can’t be contractual — but used properly, this is free money flowing past HMRC.

The annual function exemption (up to £150 per head, inclusive of VAT, covering one or more annual events) is similar. Many small companies forget it exists.

Electric Vehicles — Genuinely a Tax Win

Buy an electric company car and you’re looking at:

- 100% first-year allowance on the purchase price (extended to April 2027 in the Autumn Budget 2025)

- A benefit-in-kind rate of just 3% in 2025/26 (rising gently — still vastly lower than a petrol equivalent at 30%+)

- Free VAT recovery rules on commercial vans

- Charge points at the workplace: 100% FYA available too

For directors, the combination of a low BIK on the car and the company getting an immediate tax deduction makes electric vehicles one of the rare cases where the tax tail genuinely wags the commercial dog in a sensible direction.

Losses Don’t Have to Be Wasted

Trading losses can be:

- Set against the same year’s other profits

- Carried back against the previous 12 months (sometimes longer in extended periods)

- Carried forward indefinitely against future trading profits

For a company that’s had a rough year, the carry-back is often the most cash-positive move — you literally get a refund of tax already paid. Worth checking before just writing the year off.

Other Levers Worth Knowing About

A few that don’t always make the headlines:

- Patent Box — profits derived from patented inventions can be taxed at an effective rate of 10% rather than 25%. Underused. Massively.

- Creative Industry Tax Reliefs — for video games, film, TV, theatre, museums and orchestras. Specialist territory.

- Group Relief — losses in one group company offset against profits in another. Only relevant if you’ve got the right structure.

- Charitable donations — Gift Aid donations from the company are deductible against profits.

- Family on payroll — paying a spouse or adult child a genuine market wage for genuine work shifts income to a lower-rate (or zero-rate) taxpayer. Has to be real work, real pay. HMRC will check.

Common Mistakes That Cost Real Money

| Mistake | What It Costs | Fix |

|---|---|---|

| Missing the R&D advance notification deadline | The entire R&D claim — often tens of thousands | Diary it the moment you suspect you might qualify |

| Buying capital kit in March instead of April | A full year’s delay on tax relief | Time year-end purchases deliberately |

| Not using AIA or full expensing at all | Up to 25% of the asset’s cost — paid as tax | Audit your fixed asset register annually |

| Treating dividends as a salary substitute without modelling NI | Could be paying 8.75% dividend tax when 0% salary was available | Re-run your extraction plan each April |

| Forgetting that associated companies share thresholds | A nasty marginal rate surprise | Map your group properly before year-end |

(That table’s a touch wonky on the padding in places. Left it that way because — honestly — so are the rules.)

The Compliance Side Nobody Wants to Talk About

Reducing tax legally only works if your records survive scrutiny. HMRC’s compliance activity has stepped up noticeably since 2024 — particularly around R&D, marginal relief calculations, and capital allowance claims. If a letter does land on your mat, our HMRC investigations team handles those start to finish. Proper tax compliance work upfront makes investigations rarer, shorter and usually cheaper.

For the deadlines side of things, our corporate tax return deadlines guide walks through the calendar in detail.

Putting It All Together — A Realistic Path Forward

So, how to reduce corporation tax legally without descending into the kind of contrived schemes HMRC tears apart at tribunal? Three habits separate the companies that pay roughly what they should from the ones that quietly overpay year after year:

- Plan before year-end, not after. Once 31 March (or whatever your year-end is) passes, your options shrink dramatically. Capital purchases, pension contributions, R&D documentation — these need to be in place before the line in the sand.

- Document everything. A relief you can’t evidence is a relief you’ll lose if questioned. Cloud accounting plus a clear paper trail is non-negotiable.

- Get a second pair of eyes. Not because DIY is impossible, but because the rules move every Budget, and what was clever last year might be neutral or harmful this year. A proper business advice and accounts and tax review picks up things you’ll genuinely miss.

If you’re sitting in London or the South East and want a conversation that isn’t full of jargon and disclaimers, that’s what we do. Ask Accountants UK Ltd, 178 Merton High St, London SW19 1AY — 020 8543 1991. Or book through our contact page. One call usually reveals a few thousand quid sitting on the table.

Frequently Asked Questions

Is it really legal to reduce corporation tax?

Yes — completely. Using reliefs Parliament wrote into legislation (full expensing, R&D relief, capital allowances, pension contributions, the AIA, etc.) is the textbook definition of tax planning. It’s the contrived, artificial schemes — disguised remuneration, marketed avoidance arrangements with DOTAS numbers — that HMRC pursues. Everything in this guide is on the right side of that line.

What’s the difference between tax avoidance and tax evasion?

Avoidance is arranging your affairs within the law to pay less tax. Evasion is concealing income, falsifying records, or otherwise breaking the law. The first is legal (though aggressive avoidance attracts HMRC challenge). The second is criminal.

Can I reduce corporation tax to zero?

If your company has a loss, made qualifying R&D claims, used all its capital allowances and pension contributions effectively — possibly, yes, for a given year. But “zero forever” usually means something’s wrong with the structure or you’re not actually trading profitably. The goal should be paying what you owe, not nothing.

Do small companies need an accountant for tax planning?

Strictly, no — you can file your own CT600. Practically, almost always yes. The savings a competent accountant unlocks routinely exceed their fee by a substantial multiple, especially when capital allowances, R&D and director extraction are involved. We’ve covered the cost question in detail here.

When is corporation tax due?

Nine months and one day after your accounting period ends. For a 31 March year-end, that’s 1 January. Larger companies (profits over £1.5 million) pay in quarterly instalments — different rules apply.

How far back can I claim missed reliefs?

Generally up to two years from the end of the accounting period for most reliefs, including R&D and capital allowances. Older than that and the window’s closed. Worth auditing the last two filed returns now if you suspect things were missed.