If you’ve been Googling how to register for VAT UK rules at 11pm on a Tuesday — turnover climbing, phone ringing, second hire on payroll — you’re in the right place. This is the working guide I wish someone had handed me the first time the £90,000 number turned up uninvited.

Here’s the thing nobody mentions when you start a business: VAT isn’t really a tax in the traditional sense. It’s more of a threshold drama. You spend years ignoring it, then suddenly it’s the only thing your accountant wants to talk about. I’ve watched this happen to florists, software contractors, sandwich shops, a wedding photographer in Wimbledon, and an actual blacksmith. Same pattern every time — the rules feel opaque until they aren’t, and then everyone wonders what the fuss was about.

This guide is the no-nonsense version. It’s not a brochure. It’s the working notes — what to do, when, and why, with the bits HMRC’s own pages quietly leave out. If at any point you’d rather hand the whole thing off to humans who do this for a living, Ask Accountants UK Ltd is in Merton — and we’ll come back to that. For now, let’s get into it.

The Magic Number Isn’t Really Magic — It’s £90,000

Let’s get the headline fact out of the way first.

The UK VAT registration threshold for the 2026/27 tax year is £90,000 of taxable turnover. It hasn’t moved since April 2024, when it crept up from £85,000. According to the House of Commons Library briefing, the Chancellor confirmed no change in either the Autumn 2024 or Autumn 2025 Budget — and the Treasury’s position, as of March 2026, is that the UK’s threshold is already the highest in the OECD.

Translation: don’t hold your breath waiting for it to rise.

The deregistration threshold — the figure that lets you cancel your VAT registration if things slow down — sits at £88,000. Yes, those two thousand pounds matter. We’ll come back to that, too.

Why the Rolling 12-Month Rule Catches People Out

Here’s where I see the most expensive misunderstanding, and I’ve seen it dozens of times.

The Window That Never Stops Moving

The £90,000 threshold is not measured against your tax year. Not your calendar year. Not your accounting period and not the date you remember to check.

It’s a rolling 12-month window, and it slides forward by one month every single time the month ends. So at the end of June, you look back at July of the previous year through June of this one. At the end of July, you shift everything along by 30 days.

What this means in practice: you can sail under the threshold from April to April based on your annual accounts and still owe HMRC a registration somewhere in August because your rolling 12-month total tipped over £90,000 in May. It’s a forensic test, not a friendly annual one.

What Happens If You’re Late

The 30-day notification window starts at the end of the month in which you crossed the threshold. Your effective registration date — the date from which you’re legally required to charge VAT — is the first day of the second month after you crossed it. So cross the line on 14 May 2026, notify HMRC by 30 June, and start charging VAT from 1 July.

Late? HMRC can backdate it. And here’s the kicker: if you didn’t charge VAT to your customers during that period, you still owe it. From your own pocket. I have watched a perfectly nice plumbing business cough up over £11,000 because they noticed their turnover six months too late.

The Forward-Look Trap Almost Nobody Talks About

There’s a second test. Quieter, sneakier, easier to miss.

If at any point you have reasonable grounds to believe your taxable turnover will exceed £90,000 in the next 30 days alone, you must register immediately. Not within 30 days — immediately. And your effective registration date is the date you formed that belief, not 30 days later.

When does this bite? Usually when someone lands a big contract. A consultant signs a £120,000 project on 1 May. Boom — registration triggered the same day, regardless of what last year’s turnover looked like.

This is sometimes called the “forward-look test” or the future test. It’s an entirely separate rule from the rolling 12-month one, and as our team at Ask Accountants UK Ltd keeps confirming, it’s the one businesses most often miss when they’re growing fast.

⚠️ A note in the margin: If you’re in negotiations about a contract that would push you over the threshold in a single month, talk to your accountant before you sign anything. Once that ink is dry, the clock starts.

What Counts as Taxable Turnover (And What Doesn’t)

This is where people undercount or overcount.

Taxable turnover means almost everything you sell — not just the things you charge 20% VAT on. It includes:

- Standard-rated sales (20%)

- Reduced-rated supplies (5%)

- Zero-rated supplies (yes, these count, even though no VAT is added)

- Goods or services you “supply” as gifts above certain limits

- Reverse-charge services bought from overseas

- Some domestic reverse-charge transactions (think construction CIS work)

What doesn’t count?

- Exempt supplies (insurance, finance, education, certain health services)

- Sales clearly outside the scope of UK VAT

- VAT itself (you measure net, not gross-with-VAT)

A surprising number of new business owners assume VAT only applies once they’re “profitable enough.” It doesn’t. VAT is a turnover test, not a profit one. You can be loss-making and still legally required to register. I’ve seen it happen with start-up SaaS businesses burning cash on hosting while billing through the roof.

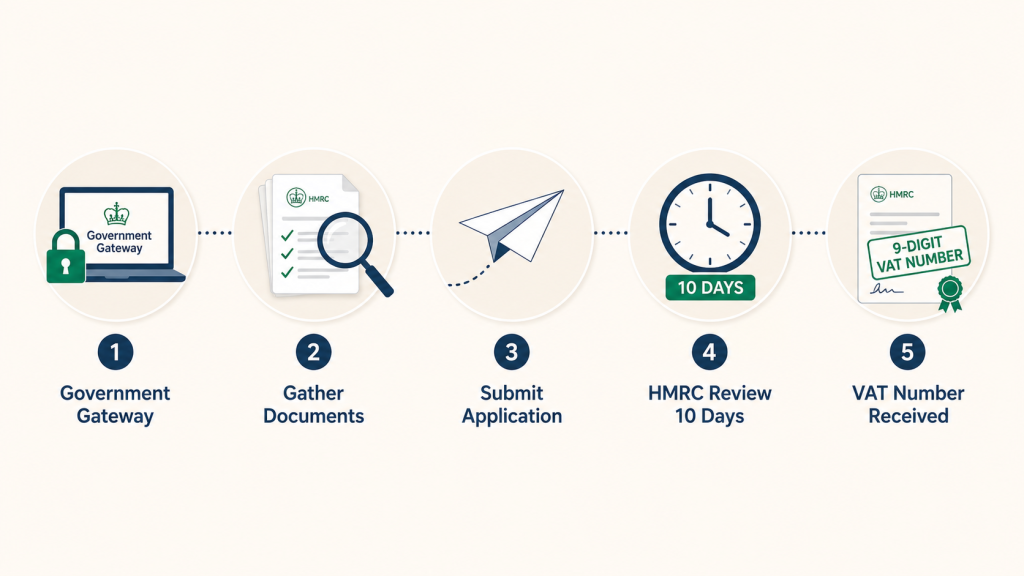

How to Register for VAT UK Online: The Step-by-Step

Right. Practicalities. Here’s the actual process for how to register for VAT UK in 2026, assuming you’re using the standard online route through HMRC. Most businesses can do this themselves — though plenty choose not to, and there are good reasons either way.

Step 1: Get a Government Gateway Account

Head to gov.uk/log-in-register-hmrc-online-services. If you already file Self Assessment, you’ve probably got one. If not, you’ll need to create one and wait for an activation code (up to 10 working days for UK addresses, up to 21 if you’re abroad).

Step 2: Gather Your Documents Before You Start

This sounds tedious. Do it anyway. You’ll save yourself the joy of restarting halfway. You’ll need:

- National Insurance number (sole traders) or Company Registration Number (limited companies)

- Your UTR (Unique Taxpayer Reference)

- Business bank account details

- Estimated turnover for the next 12 months

- Date you crossed the threshold (or expect to)

- The nature of your business activity (SIC code helps)

Step 3: Submit Your VAT Application

Go directly to the HMRC VAT registration page. The system lets you save your progress and come back to it. Take advantage of that. Don’t rush.

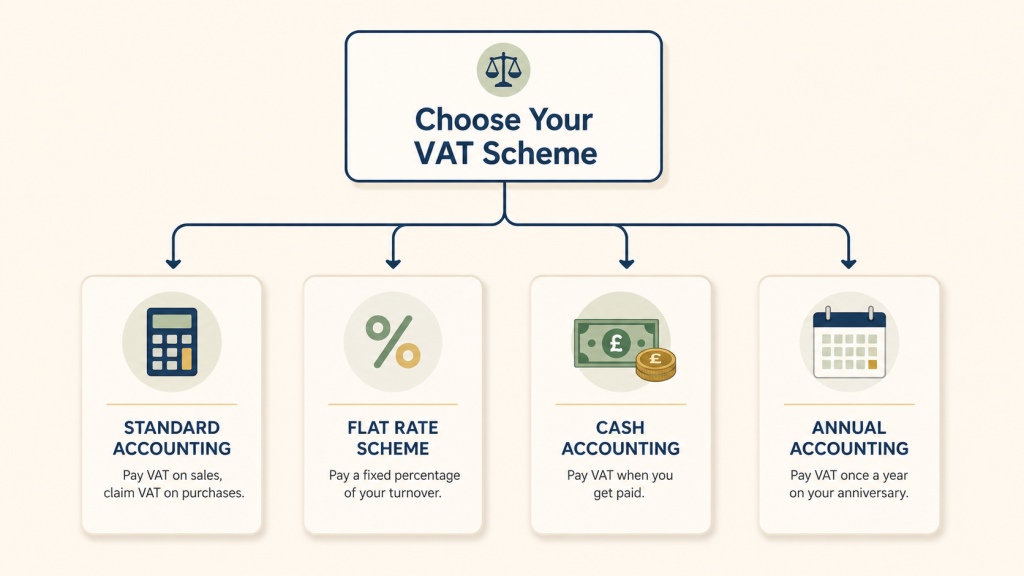

Step 4: Choose Your VAT Scheme

This matters more than people realise. Your options include the Standard Accounting Scheme, the Flat Rate Scheme, the Cash Accounting Scheme, and the Annual Accounting Scheme. We’ll get to schemes in a moment, but pick wrong and you can lose serious money over the course of a year.

Step 5: Submit and Wait for Your VAT Number

Most applications are processed in 10 working days, though it can stretch to 2–8 weeks if HMRC wants to verify your details. Voluntary registrations sometimes take longer than compulsory ones, oddly enough. Your number will be nine digits long, usually arriving by post or email. Once you have it, every invoice you issue must show it.

💡 The thing nobody mentions: Between your effective registration date and the day your VAT number arrives, you must still charge VAT — but you can’t issue a proper VAT invoice yet. The workaround is to add the VAT amount to the gross invoice total and then reissue proper VAT invoices once your number lands. Awkward. Not optional.

Quick Reference: When Do You Actually Need to Register?

| Scenario | Trigger | Deadline to Notify | Effective Date |

|---|---|---|---|

| Rolling 12-month turnover exceeds £90k | End of any month | 30 days from month-end | 1st of the 2nd month after |

| Expect to exceed £90k in next 30 days | The day you form that belief | By end of the 30-day period | The date you formed that belief |

| Voluntary registration (below threshold) | Your choice | No deadline | Date you specify (within reason) |

| Overseas business supplying UK customers | First taxable sale (NETP rules) | Immediately | Date of first supply |

Voluntary Registration: When It’s Brilliant, and When It’s a Headache

Now this is the conversation I have with clients most often.

Voluntary VAT registration — choosing to register before you cross £90,000 — isn’t free admin, but it isn’t always foolish either. Whether it’s smart depends almost entirely on who buys from you.

When Voluntary Registration Actually Pays Off

It tends to work brilliantly when:

- Your customers are mainly VAT-registered businesses (B2B). They reclaim what you charge them, so adding 20% to your invoice doesn’t sting them.

- You have significant input VAT to reclaim — equipment, software subscriptions, professional fees, vehicles.

- You want larger corporate clients to take you seriously. Some procurement departments won’t engage with an unregistered supplier full stop.

- You’re approaching the threshold anyway and want to get your bookkeeping habits sharp before compulsion kicks in.

When It Quietly Backfires

It tends to backfire when:

- Most of your customers are members of the public, who can’t reclaim VAT. You either eat the 20% from your margin or hand your competitors a pricing advantage.

- You have very low input VAT (most service businesses with thin overheads).

- You can’t face the quarterly admin or the Making Tax Digital software requirement.

There’s no universal right answer. Genuinely. We’ve seen Wimbledon-based consultants benefit hugely from voluntary registration and Wandsworth-based hair salons regret it within six months.

The MTD Wrinkle: What Changed on 1 April 2026

If you’re working out how to register for VAT UK rules in 2026, you’re walking straight into the Making Tax Digital regime — there’s no separate threshold for that anymore.

Since 1 April 2026, every VAT-registered business in the UK (no matter how small) must:

- Keep digital records using HMRC-compatible software

- Submit VAT returns through MTD-compatible software

- Maintain “digital links” between systems (no copy-pasting between spreadsheets and your filing tool)

This means the days of registering for VAT and then handling it in a desktop spreadsheet are well and truly over. You need software — QuickBooks, Xero, FreeAgent, Sage, or one of the bridging tools. We’ve covered this in detail in our Making Tax Digital for VAT guide, but the short version is: factor software cost into your VAT registration decision from day one.

For practical help getting set up with the right software (and avoiding the cost of switching later), our cloud accounting service walks new VAT registrants through the full setup.

Choosing the Right VAT Scheme Without Regret

When you register, HMRC gives you a menu. Most people pick the default and never look back. That’s often a mistake.

Here’s a rough comparison — and I’ve left one of the rows looking slightly scruffy because, honestly, real-world VAT scheme decisions are messier than tidy columns suggest.

| Scheme | Who It Suits | Main Advantage | Watch Out For |

|---|---|---|---|

| Standard Accounting | Most businesses with significant input VAT | Reclaim everything you’re entitled to | More record-keeping |

| Flat Rate Scheme | Small businesses with low input VAT, turnover < £150k | Simpler. Pay a fixed % of gross turnover. | “Limited cost trader” 16.5% rate can hurt you |

| Cash Accounting | Businesses with slow-paying customers | Account for VAT when paid, not invoiced. Cashflow lifesaver. | Must deregister if turnover above £1.35m |

| Annual Accounting | Steady, predictable businesses | One return a year, instalment payments | Less flexibility on refunds |

Choose the wrong scheme and the cost over a year or two can dwarf any saving from registering at the “right” time. This is the bit where having a chat with a real human accountant pays for itself.

Penalties for Getting It Wrong (The Unpleasant Bit)

I’m not going to dwell on this, but you should know what you’re risking.

What HMRC Can Hit You With

If HMRC works out that you should have registered earlier than you did:

- They’ll backdate the registration to the date you should have registered

- You’ll owe VAT on every taxable sale from that date — even if you never collected it from customers

- A late-registration penalty applies, scaled to how late you were

- Interest accrues on the unpaid VAT

- Under the current late payment regime, penalties of 3% kick in at 15 days overdue, rising to 6% at 30 days, with a further 10% annualised after that

A Real-World Cautionary Tale

The most painful version of this scenario I’ve seen recently was a London e-commerce seller who’d been over the threshold for nine months without realising. The backdated VAT bill was £14,200. The penalty added £1,800. The accountant fees to clean it up — another £900.

All preventable with a monthly rolling-turnover check that takes about ten minutes.

A Few Things I Wish More People Asked Me About

Disaggregation: Trying to split your business into two smaller businesses to stay under £90,000 each? HMRC is allergic to this. They have specific anti-disaggregation powers and will treat connected businesses as one for VAT purposes if there’s no genuine commercial reason for the split.

Going below £88,000 after registering: You can apply to deregister, but you don’t have to. Some businesses prefer to stay registered to keep reclaiming input VAT. Worth modelling.

Pre-registration VAT reclaim: This one’s genuinely lovely. Once registered, you can reclaim VAT on goods bought up to 4 years before registration (still in stock or use) and services bought up to 6 months before. Keep those receipts.

Overseas businesses: Different rules. For most non-established taxable persons, the £90,000 threshold doesn’t apply — you may need to register from the first taxable UK sale. Don’t assume the standard rules cover you.

When DIY Registration Stops Being Fun

I’ll be honest. You don’t need an accountant to register for VAT in the UK. The HMRC online system is reasonably clear, the forms aren’t onerous, and there’s no fee for registering yourself.

But VAT isn’t really about the registration. It’s about everything that comes after — scheme selection, invoice templates, partial exemption, MTD software, dealing with the inevitable HMRC compliance check that lands two years in. That’s where most of the value lives, and where mistakes get expensive.

At Ask Accountants UK Ltd, our VAT services cover the whole arc — from working out whether you actually need to register, through scheme selection, MTD setup, quarterly returns and the occasional HMRC investigation when things go sideways. We also handle the broader ecosystem most growing businesses need: bookkeeping, accounts and tax, self-assessment, CIS claims, automatic enrolment, business plans and the cloud accounting setup that ties it all together.

If you’d rather have a quick conversation than read another 2,000 words of HMRC guidance, we’re at 178 Merton High St, London SW19 1AY, or on 020 8543 1991. Most of our VAT consultations are free for new clients — partly because the questions are usually similar, and partly because it’s better for everyone if you get this right at the start.

FAQs About How to Register for VAT UK

How long does it take to register for VAT in the UK?

Most online applications are processed within 10 working days, though it can take 2 to 8 weeks if HMRC needs additional verification. Voluntary registrations sometimes take a bit longer than compulsory ones.

Can I register for VAT before I hit the £90,000 threshold?

Yes. This is voluntary registration, and any business can apply. It makes the most sense for B2B businesses with significant input VAT to reclaim, or those approaching the threshold who want to get their systems in order early.

What happens if I forget to register on time?

HMRC will backdate your registration, charge you the VAT you should have collected (even if you didn’t), and apply a late-registration penalty plus interest. The earlier you spot the issue, the cheaper it is to fix.

Do I need an accountant to register for VAT?

No. The HMRC online process is free and you can do it yourself. That said, scheme selection and ongoing compliance get complicated quickly, which is where professional help usually earns its keep.

Does the rolling 12-month rule reset at the end of the tax year?

No, and this is the biggest single misconception about how to register for VAT UK rules properly. The 12-month window slides forward every single month — it never resets.

Can I learn how to register for VAT UK as a sole trader?

Absolutely. VAT registration applies to any business structure: sole traders, partnerships, limited companies, even non-UK businesses supplying to the UK. The £90,000 threshold rule is identical.

What’s the cost to register for VAT?

Registration itself is completely free through HMRC. The costs come afterwards — MTD-compatible software, possibly an accountant for ongoing returns, and the time spent maintaining digital records.

Can I deregister if my turnover drops?

Yes, if your taxable turnover falls below £88,000 (the deregistration threshold), you can apply to cancel your VAT registration. You don’t have to — some businesses stay registered to keep claiming input VAT.

Final Thoughts on How to Register for VAT UK in 2026

If you take only one thing from this guide on how to register for VAT UK rules in 2026, let it be this: check your rolling 12-month turnover at the end of every single month. Not your annual figures. Not your gut feeling. The rolling total.

Stick a reminder in your calendar. Set up a turnover-tracking sheet in your accounting software. Tape a note to your monitor. Whatever it takes.

That one habit is the difference between handling how to register for VAT UK as a calm, planned event — and discovering it as an expensive surprise six months too late.

Good luck. You’ve got this. And if you’d rather not, well — you know where to find us.

📞 Ask Accountants UK Ltd | 178 Merton High St, London SW19 1AY | 020 8543 1991 | Book a free VAT consultation →