Let’s be honest about something. Most self-employed people and landlords in the UK have been quietly ignoring the words “Making Tax Digital” for the better part of a decade. HMRC announced it, delayed it, announced it again, and delayed it again. Twice. And after the third announcement, you’d be forgiven for thinking it would just never actually happen.

It’s happening.

The Making Tax Digital deadline 2026 — specifically 6 April 2026 — is now confirmed and, more importantly, has already arrived for hundreds of thousands of sole traders and landlords earning above £50,000. If that includes you and you’re reading this wondering whether you’ve already missed something or whether there’s still time to sort things out, keep reading. There’s a fair amount to unpack here.

Who Got That HMRC Letter in February?

HMRC began writing to affected taxpayers in February and March 2026 — not an automated nudge, an actual you need to act letter. If you received one, it wasn’t junk. If you didn’t receive one but your combined gross income from self-employment and/or property exceeded £50,000 on your 2024/25 tax return, you’re still in scope. The letter doesn’t exempt you from anything; it’s just a heads-up.

The Making Tax Digital 2026 rules apply to you if:

- You’re a sole trader, freelancer, or self-employed individual

- You’re a landlord receiving UK or overseas rental income

- Your combined gross income from these sources — before expenses, mind you — exceeded £50,000 on the 2024/25 return filed by 31 January 2026

That last point trips people up. It’s gross income, not profit. A landlord with £55,000 rental income but only £8,000 actual profit after mortgage interest, repairs, and letting agent fees is still in scope. A freelance designer billing £52,000 but keeping £30,000 after costs? Also in scope.

What doesn’t count toward the threshold: wages from employment, dividends, pensions, savings interest. HMRC is only looking at business and property income for this calculation.

The Three-Phase Rollout — And Why Phase One Is Now

| Phase | Start Date | Income Threshold | Assessed From | Estimated Taxpayers |

|---|---|---|---|---|

| Phase 1 | 6 April 2026 | Over £50,000 gross | 2024/25 tax return | ~780,000 |

| Phase 2 | 6 April 2027 | £30,000 – £50,000 gross | 2025/26 tax return | ~900,000 additional |

| Phase 3 | 6 April 2028 | £20,000 – £30,000 gross | 2026/27 tax return | ~900,000 additional |

Note: Partnerships are not currently included in any phase. MTD for Corporation Tax has also been officially shelved.

One scenario that catches people out: a landlord with £29,000 rental income and a side business turning over £22,000. Combined, that’s £51,000 — Phase 1 territory, even though neither income stream individually crossed the threshold. HMRC aggregates everything.

What “Making Tax Digital” Actually Requires You To Do

Here’s where the real change sits. Under the old Self Assessment system, most people gathered their records once a year, handed them to an accountant (or wrestled with HMRC’s website in January), filed a return, and paid their tax. Annual. One submission.

Under Making Tax Digital for income tax, that rhythm is gone. From April 2026, affected taxpayers must:

1. Keep digital records continuously Paper receipts in a shoebox will no longer cut it — at least not on their own. Every income and expense item needs to be recorded digitally, with the date, amount, and category logged in MTD-compatible software. Spreadsheets can still be used, but they must be digitally linked to your submission software. That means no copy-and-pasting data across; the transfer between systems has to happen digitally. It’s a specific technical requirement, not just a preference.

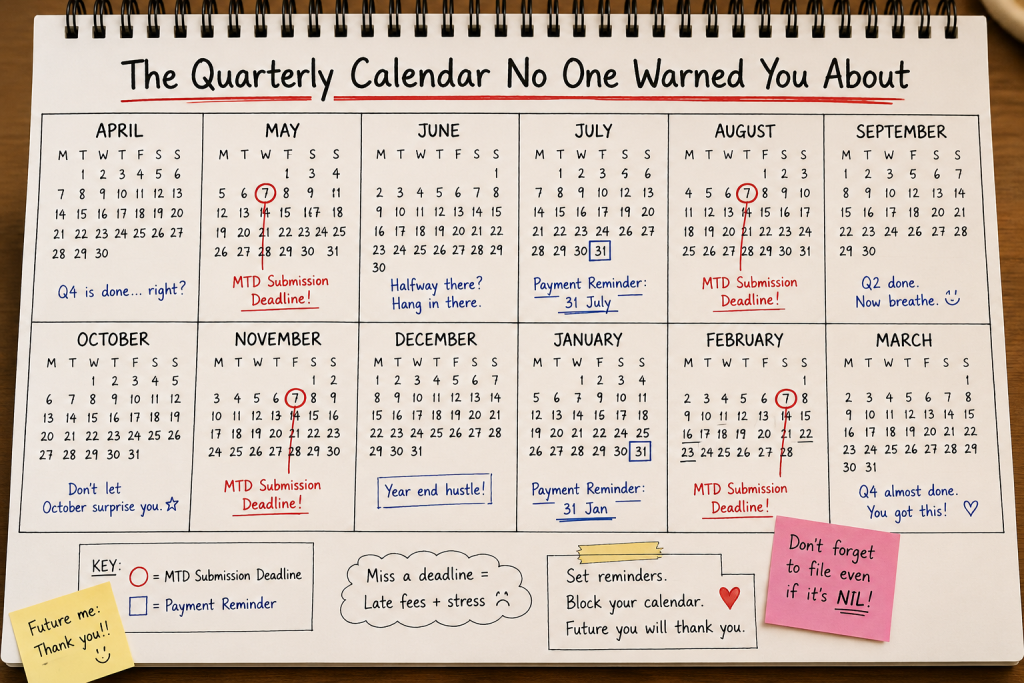

2. Submit quarterly updates to HMRC Four times a year, you’ll push a summary of income and expenses to HMRC through your software. The quarterly deadlines are:

- 7 August — for the quarter ending 5 July (or 30 June on calendar quarters)

- 7 November — for the quarter ending 5 October (or 30 September)

- 7 February — for the quarter ending 5 January (or 31 December)

- 7 May — for the quarter ending 5 April (or 31 March)

These aren’t tax payment dates. They’re reporting dates. Your actual tax payments still follow the familiar Self Assessment schedule — 31 January and 31 July.

3. Submit a Final Declaration by 31 January each year This replaces the traditional Self Assessment return. After your four quarterly updates, the Final Declaration pulls together all your income sources (employment, dividends, savings — everything) to establish your actual tax liability for the year. For the 2026/27 tax year, that Final Declaration is due by 31 January 2028.

The Soft Landing: HMRC’s Unexpectedly Generous Gesture

Here’s something that got lost in the noise. For the 2026/27 tax year only — meaning the first year of Phase 1 — HMRC has confirmed a soft landing on late submission penalties. If you’re newly in scope and you miss one of your first four quarterly deadlines, you won’t receive a penalty point.

⚠️ Important: This soft landing only covers submission penalties for quarterly updates. It does not protect you from late payment penalties. If you owe tax and miss the 31 January or 31 July payment deadline, the normal interest and penalty charges still apply immediately.

The penalty structure itself works on a points system — miss a submission, get a point; accumulate four points, receive a £200 fine. After the soft landing period ends on 5 April 2027, those points will start accumulating properly.

So there’s a window. But using that window as an excuse to do nothing is, frankly, the classic mistake.

Choosing Your Software — And Why This Decision Matters More Than You Think

HMRC maintains a list of approved MTD-compatible software products. The big names — QuickBooks, Xero, FreeAgent, Sage — are all on it. But the choice isn’t just about brand preference.

A few things genuinely matter here:

- Bank feed integration. Software that connects directly to your business bank account and automatically pulls in transactions saves a staggering amount of time. Manually categorising every transaction quarterly is nobody’s idea of a good morning.

- Multiple income streams. If you have a sole trade and a rental property, you need software that handles both within the same MTD submission. Not all products do this elegantly.

- Bridging software. If you’re committed to using spreadsheets for your bookkeeping, bridging software creates the required digital link between your spreadsheet and HMRC’s API. It works, but it adds a step.

- Cost vs. complexity. Sole traders with one income stream and simple expenses can often manage with lighter, cheaper tools. Landlords with multiple properties or those running VAT-registered businesses alongside their rental portfolio will need something more capable.

The team at Ask Accountants UK Ltd works extensively with cloud accounting platforms including QuickBooks and Xero, and can help you identify which software suits your specific income structure rather than just recommending what happens to be cheapest.

Exemptions — Because There Are Some, And They’re Specific

Not everyone earning over £50,000 is automatically pulled into the Making Tax Digital 2026 regime. HMRC has confirmed exemptions and deferrals for:

- Individuals under a Power of Attorney or Court of Protection deputyship

- Those who can demonstrate genuine digital exclusion — not just a preference for paper, but a genuine inability to use software due to disability, age, or remote location with no reliable internet

- Recipients of trust and estate income — deferred at least until April 2027

- Those using averaging adjustments (common in farming and creative industries)

- Qualifying care providers (foster carers, shared lives carers)

- Non-UK resident foreign entertainers or sportspeople

- Individuals completing the SA109 residence and remittance basis pages — also deferred to at least April 2027

If you believe you qualify for an exemption, applications can be made from 29 January 2026 by contacting HMRC directly by phone or in writing. An authorised agent can also make the application on your behalf. The exemption is not automatic — you have to request it.

Worth noting: if you were already exempt from MTD for VAT on digital exclusion grounds, that exemption does not automatically carry over to MTD for income tax. You need to apply separately.

The Landlord Complication

Landlords — particularly those with portfolios, HMO properties, or mixed UK/overseas holdings — face some additional complexity under MTD income tax 2026 that pure sole traders don’t.

Separate digital records are required for each property income source. A landlord with three buy-to-lets and a furnished holiday let technically has four distinct income streams to track. The software choice matters here: not all MTD tools handle property income records at this level of granularity without significant manual workaround.

There’s also the question of year-end calculations. Finance costs (mortgage interest, after Section 24 restrictions), capital allowances on furnished holiday lettings, and HMRC’s sometimes arcane rules on allowable expenses for property don’t disappear just because you’re now filing quarterly. They just have to be accounted for correctly within the digital records you’re keeping.

The practical advice — get your business banking genuinely separated from personal banking now, if you haven’t. During an HMRC review or spot-check, mixed accounts are the first thing that creates problems.

For landlords specifically, Ask Accountants UK Ltd’s property accounting services and bookkeeping support can take much of the quarterly administration off your plate.

What Happens If You Just… Don’t?

A fair question. The answer is: a points-based penalty system with a £200 fine once you accumulate four points, with additional penalties escalating from there. Beyond the soft landing period, missing a single quarterly submission earns one point. Four points means a £200 charge. Points reset over time (generally after 24 months of full compliance), but they don’t vanish quickly.

Late payment penalties operate separately and haven’t changed from the existing Self Assessment model. Interest accrues daily on unpaid tax from the due date.

And here’s the quiet part that doesn’t get much coverage: HMRC’s data-matching capabilities are considerably better in the MTD environment. The architecture of quarterly digital reporting means HMRC can compare what you’ve submitted against third-party data — bank feeds, rental platform reports, contractor payment records — far more easily than under the annual return system. The risk of an HMRC investigation for taxpayers whose records don’t hold up under scrutiny is realistically higher in a quarterly digital environment, not lower.

The Quarterly Reporting Rhythm in Practice

One thing people don’t fully grasp until they’re doing it: quarterly reporting is not meant to be a mini-tax-return. The quarterly updates are summaries — your software pushes the totals of income and expenses across the standard categories to HMRC. You’re not recalculating your tax liability four times a year; you’re giving HMRC a running picture.

HMRC’s systems will use that data to provide an estimated in-year tax position, potentially reducing payment shocks at the January deadline for some taxpayers. That’s the theory. In practice, the estimate is only as accurate as the records being submitted, which is why good categorisation from the start matters.

The Final Declaration in January is where everything gets locked in — all income sources, personal allowances, reliefs, and adjustments. It’s the moment that actually fixes your liability. Until that’s filed, quarterly updates don’t set anything in stone.

MTD Quarterly Submission Deadlines — At a Glance

| Quarter Period (Tax Year) | Quarter Period (Calendar) | Submission Deadline |

|---|---|---|

| 6 April – 5 July | 1 April – 30 June | 7 August |

| 6 July – 5 October | 1 July – 30 September | 7 November |

| 6 October – 5 January | 1 October – 31 December | 7 February |

| 6 January – 5 April | 1 January – 31 March | 7 May |

| Final Declaration (replaces Self Assessment) | 31 January | |

Tax payments remain unchanged: 31 January (balancing payment + first payment on account) and 31 July (second payment on account).

Your Action Checklist for the Making Tax Digital 2026 Transition

Rather than a vague “get prepared” message, here are the specific steps that actually move the needle:

- Check your 2024/25 gross income figures. This is the number HMRC is using to determine your Phase 1 mandate. If you’re unsure whether you’re over £50,000, your accountant can confirm this.

- Register for MTD ITSA with HMRC. If you haven’t done this yet, it needs to happen. Your agent can do this on your behalf.

- Choose and set up your software. Don’t just download something and leave it disconnected. Set up bank feeds, test the connection to HMRC’s sandbox environment if possible, and get familiar with how quarterly updates work before the first real deadline.

- Separate your business and personal banking. This one is non-negotiable for clean digital records.

- Review your record-keeping categories. MTD submissions use standard HMRC income and expense categories. Make sure your existing bookkeeping aligns — or get someone to help you restructure it.

- Consider professional support. Not because you can’t manage the software yourself, but because the interpretation of which records are kept, how transactions are categorised, and how the Final Declaration is assembled has real tax consequences. Getting the quarterly data wrong doesn’t just create a compliance problem — it can result in overpaid or underpaid tax that HMRC will want to resolve.

The team at Ask Accountants UK Ltd — based at 178 Merton High St, London SW19 1AY — handles self assessment, tax compliance, and cloud accounting setup for sole traders and landlords across London. If you’re trying to work out whether you’re in scope, which software fits your situation, or simply want someone to handle the quarterly submissions on your behalf, they’re reachable on 020 8543 1991 or through the contact page.

Frequently Asked Questions About the Making Tax Digital Deadline 2026

Does MTD 2026 apply to me if I’m employed but also have rental income? Yes, potentially. PAYE employment income doesn’t count toward the MTD threshold, but if your rental income alone — or combined with any self-employment — exceeds £50,000 gross, you’re in Phase 1.

What if my income dropped below £50,000 this year? The mandate is assessed based on the 2024/25 tax return. If your income has since dropped, you may exit MTD in a future year — but HMRC determines this based on the relevant reference period. You can’t simply opt out. Speak to an accountant about the specific exit criteria.

Can I still use a spreadsheet? Yes, but it must be digitally linked to MTD-compliant software for the HMRC submission. You cannot manually copy data across. Bridging software handles this link.

What is a Final Declaration and how is it different from Self Assessment? The Final Declaration replaces the Self Assessment tax return. It’s submitted by 31 January, includes all income sources (not just business income), and finalises your tax liability for the year. The mechanics are similar to the current SA return, but it’s submitted through MTD-compatible software rather than HMRC’s online portal.

What if I genuinely cannot use digital software? Apply for a digital exclusion exemption directly with HMRC. This requires a genuine reason — disability, remote location without internet access, or demonstrable inability to use the technology. It’s not available simply because you’d prefer not to change.

I missed the April 2026 start date. What happens now? Your first practical priority is getting software set up and submitting your Q1 update (April–June/July) before 7 August 2026. Contact an accountant or HMRC directly if you’re unsure of your current status.

For further official guidance, see HMRC’s MTD for Income Tax overview and the ICAEW Tax Faculty’s detailed MTD guide.

Also relevant from Ask Accountants UK Ltd: Making Tax Digital for VAT | Cloud Accounting Services | Personal Tax Planning | HMRC Investigations Support | Self Assessment

Ask Accountants UK Ltd | 178 Merton High St, London SW19 1AY | 020 8543 1991