Right. Let’s talk about the thing that’s quietly ruining accountants’ summer holidays and sending landlord WhatsApp groups into mild panic.

If you’re a sole trader or a landlord earning above a certain threshold, the way you talk to HMRC is about to change in a fairly fundamental way. Not in a “fill out a slightly different form” way. More in a “you’ll be doing this four times a year instead of one, and HMRC would quite like all of it through software, please” sort of way.

This is MTD for Income Tax — or, if you fancy the full mouthful, Making Tax Digital for Income Tax Self Assessment. It goes live on 6 April 2026. And honestly? Plenty of people aren’t ready. A recent IRIS survey reckoned roughly 45% of UK sole traders feel unprepared. I’d wager the real figure is higher, because some of the people who think they’re ready haven’t actually opened the software yet.

So here’s a proper, slightly opinionated guide — written for actual humans who’d rather not get fined £200 for forgetting a quarterly update.

Who’s Actually Getting Pulled Into This Thing?

Let’s start with the bit that catches people out, because there’s a sneaky little detail in the rules.

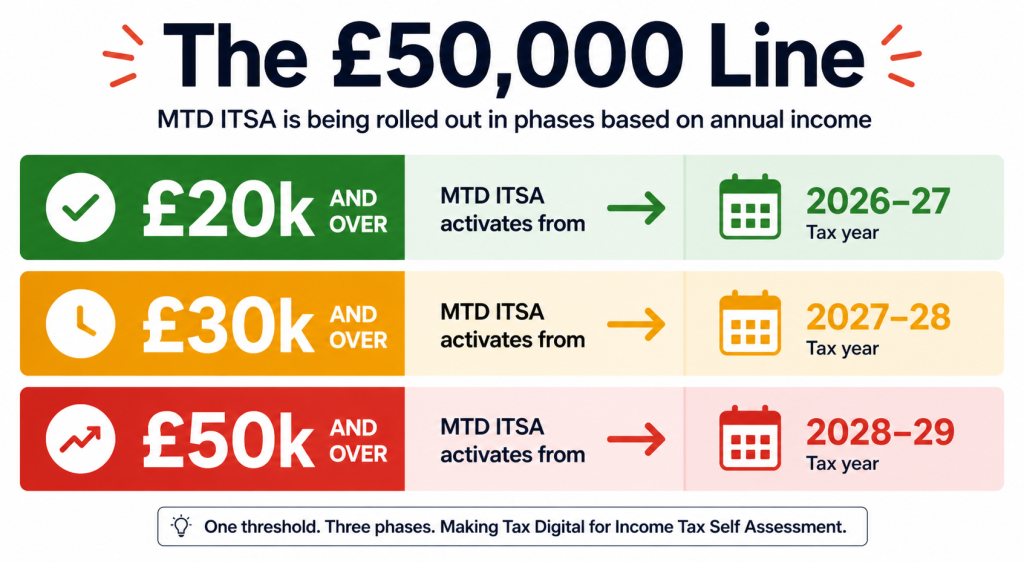

From 6 April 2026, MTD for Income Tax becomes mandatory if your gross income from self-employment plus UK property exceeded £50,000 in the 2024–25 tax year. Not your profit. Your gross. Before you take a single penny off for expenses, mortgage interest, allowable repairs, or that new boiler you grumbled about installing.

This trips people up constantly. I’ve had landlords say “but I barely break even after the mortgage” — doesn’t matter. HMRC’s looking at the top-line figure on your Self Assessment return, not the bottom one.

The phased rollout — what year you’ll join

A quick look at how the rollout works:

| Phase | Start Date | Gross Qualifying Income (looked at from) | Who’s Caught |

|---|---|---|---|

| Phase 1 | 6 April 2026 | Over £50,000 (2024–25 figures) | Roughly 780,000 sole traders and landlords |

| Phase 2 | 6 April 2027 | Over £30,000 (2025–26 figures) | A further ~970,000 people |

| Phase 3 | 6 April 2028 | Over £20,000 (2026-27 figures) | Most remaining sole traders & landlords |

Mixed income? You add it all up

Got both rental income and a side hustle as a sole trader? Add them together. £28,000 from a small consultancy and £25,000 from a flat in Croydon means you’re at £53,000 — and you’re in from April 2026.

Joint ownership? You only count your personal share. If you and your spouse own a property together 50/50 and it brings in £40,000, your slice is £20,000.

And a little curio buried in the rules: if you don’t have a National Insurance number on 31 January 2026, you’re exempt for the first year. That’s not a loophole anyone should chase — it’s there for people in genuinely unusual circumstances. HMRC has a qualifying income checker on its site if your situation is borderline.

What’s Actually Changing (Spoiler: Quite a Lot)

The headline change is this: instead of one Self Assessment return, you’ll send HMRC five filings every year. Four quarterly updates plus a Final Declaration.

Each quarterly update is essentially a running tally of your income and expenses for that three-month window — submitted through HMRC-compatible software. Cash basis is allowed by default for most people, which actually simplifies things. No fiddling with prepayments and accruals every three months. Thank goodness.

The new deadlines, all in one place

The deadlines are fixed. They don’t move with weekends or bank holidays in any helpful way:

| Quarter | Period Covered | Submission Deadline |

|---|---|---|

| Q1 | 6 April – 5 July | 7 August |

| Q2 | 6 July – 5 October | 7 November |

| Q3 | 6 Oct – 5 Jan | 7 February |

| Q4 | 6 Jan – 5 April | 7 May |

| Final Declaration | Whole tax year (replaces Self Assessment) | 31 January following |

You can opt for calendar quarters instead (March, June, September, December) — useful if you’re already MTD-registered for VAT and want everything aligned. Most people won’t bother. The standard tax-year quarters are fine.

And the Final Declaration — what it actually is

The Final Declaration is where the rest of your tax life gets reconciled. Capital gains, dividends, pension contributions, gift aid, employment income, savings interest — all the things MTD doesn’t touch — get added in here. Your software handles the income/expenses summary; the rest is bolted on at the end. It’s the new shape of Self Assessment — not a replacement for it, but a redesign of the front end.

The Software Question (and Why Spreadsheets Aren’t Quite Dead)

HMRC isn’t building its own software. They’ve outsourced that bit to the market — which means you have to choose your tool. Currently the popular MTD-compatible options include QuickBooks, Xero, FreeAgent, Hammock (which a lot of landlords seem to swear by), and Sage. There are dozens more. HMRC keeps a running list of compatible software on their site.

A common myth — spreadsheets aren’t banned

A common misconception worth flattening: spreadsheets are not banned. You can keep using Excel or Google Sheets, but they need to be linked to “bridging software” that pushes the data to HMRC through the proper digital route. You can’t just type figures from a spreadsheet into a portal — that breaks the digital-link rule.

Why I’d just go cloud anyway

Honestly though, if you’re starting fresh, a proper cloud accounting tool will save you headaches. Bank feeds, automatic categorisation, receipt capture from your phone — the time you save is the difference between dreading quarter-end and shrugging it off. We’ve covered why so many London businesses are switching to cloud accounting elsewhere on the blog if you want a deeper read on the practicalities.

For landlords specifically, QuickBooks has become a go-to — partly because it’s HMRC-recognised, partly because the property modules are decent, partly because most accountants already know their way around it.

💡 A small but loud tip: Sign up early. HMRC won’t enrol you automatically, even if they send you a letter. You have to actively register through the HMRC sign-up page. Leave it until late March 2026 and you’ll be fighting through a queue with a million other people.

The Penalty Regime — and the Year-One Mercy

Here’s where I’d usually expect a dry recital of fines. But there’s an interesting twist.

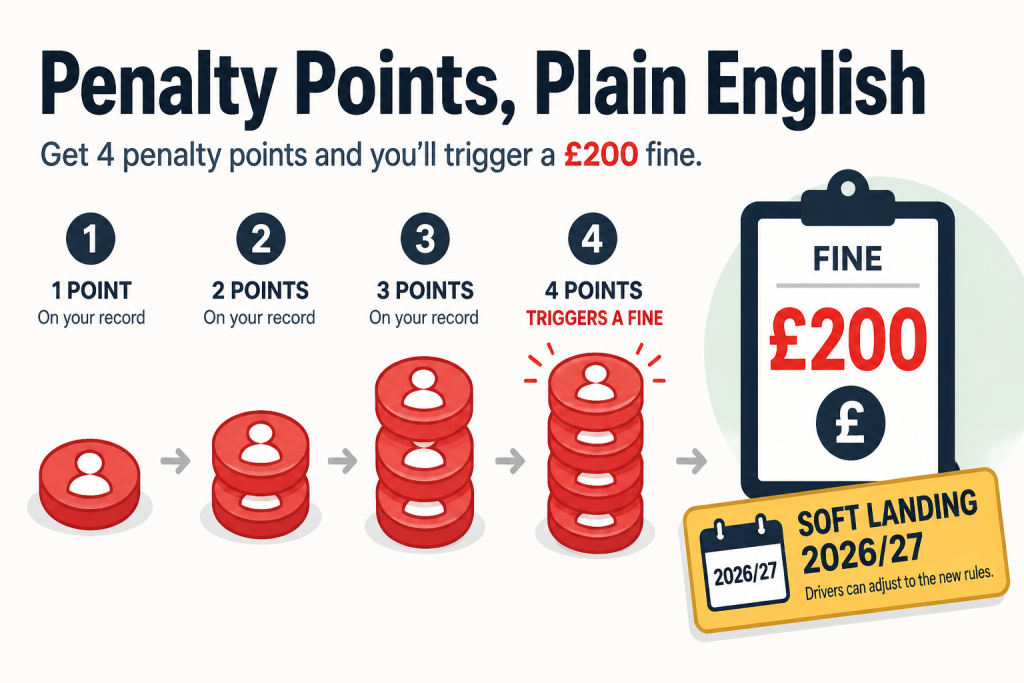

HMRC announced in the Autumn Budget 2025 that late submission penalties for quarterly updates are waived for the entire 2026–27 tax year for those mandated into MTD. This is the so-called “soft landing.” Miss a quarter? You won’t get a penalty point during year one.

But — and this is the crucial bit people skim past — the soft landing does not apply to the Final Declaration. File that one late and the points start ticking immediately. It also doesn’t cover late payment penalties, which are a totally separate beast.

How the points system actually works

After the soft landing ends, the system works like this: every late submission earns a penalty point. Hit four points within a 24-month window, and HMRC issues a £200 fine. Every subsequent late filing while you’re at the threshold? Another £200. Points expire after 24 months of clean filing.

The other (uglier) penalties lurking nearby

There are also some uglier ones lurking in the background:

- Failing to keep proper digital records: up to £3,000 per quarter

- Deliberately withholding information: minimum £300, potentially much more

- Late payment penalties: 3% of outstanding tax at day 15, plus another 3% at day 30, then 10% per annum thereafter (these rates rise from April 2027)

It adds up fast. The MoneySavingExpert team has a decent breakdown of the penalty mechanics too if you want a second perspective.

Who Doesn’t Have to Bother (Yet)

Not everyone with the income gets dragged in. Genuine exemptions exist, though they’re narrower than people hope.

You can apply for digital exclusion if you can’t reasonably use digital tools because of age, disability, religious belief, or because your internet connection is best described as “wishful thinking.” Living in a remote bit of Scotland with 0.5 Mbps? Possibly exempt. Just hate computers? Sorry, no.

Automatic carve-outs

Other automatic carve-outs:

- Limited companies (different system entirely — they were already going through their own MTD changes)

- Partnerships (not yet — they’ll be brought in later)

- Trustees, executors, and personal representatives acting in that capacity

- People with no qualifying income, obviously

- Non-UK residents without a National Insurance number

If your circumstances are genuinely complicated — multiple income streams, overseas property, a partnership and a sole trade, that sort of thing — getting a property accounting or tax compliance specialist to map out your obligations early is the cheapest insurance you’ll buy this year.

What I’d Actually Do If I Were You

Let me drop the formal voice for a second. If I were a sole trader or landlord facing this in April 2026, here’s roughly the order I’d tackle things:

- Check your 2024–25 figures. Are you over £50,000 gross? If yes, you’re in. Don’t wait for HMRC to write to you — they might, they might not, doesn’t matter either way.

- Pick software. Don’t spend three months testing every option on the market. Pick one your accountant uses. Done.

- Connect bank feeds. Day one. The whole system collapses if you’re typing transactions in by hand at 11pm on 6th August.

- Run a “fake” quarter. Pretend Q1 has happened, do the submission process, see where it breaks. Better to find out in February 2026 than August 2026.

- Sort out receipt capture. Phone apps that read receipts have got genuinely good. Use them.

- Talk to an accountant if you’re unsure. Even one consultation can save you the cost of three software subscriptions.

⚠️ A warning, not a tip: If you’ve been a bit casual with your record-keeping (we all know someone who keeps receipts in a shoebox — possibly yourself), MTD ends that era. Either get organised before April 2026 or pay someone to do it for you. There’s no third option that doesn’t involve fines.

Where Ask Accountants Fits In

This is where I’d usually expect the marketing pitch. I’ll keep it brief.

Ask Accountants UK Ltd — based at 178 Merton High St in Wimbledon — has been working with sole traders, landlords and small businesses across south west London on exactly this kind of transition. We handle the bookkeeping, the cloud accounting setup, and the quarterly submissions themselves; we also do personal tax planning for the bigger picture stuff that sits around MTD. If you’d like a chat about whether you’re in scope, what software fits your setup, or how to register without losing the will to live, 020 8543 1991 gets you to the office — or use our contact page if you’d rather drop us a message.

No high-pressure sales nonsense — just a sensible conversation about what’s coming.

Quick FAQ on MTD for Income Tax

Does MTD for Income Tax replace my Self Assessment return entirely?

Not quite. The Final Declaration replaces the Self Assessment as the vehicle for finalising your year, but you’ll still report dividends, capital gains, employment income, pensions and the rest through it. MTD only digitises the self-employment and property bits.

I have rental income and consultancy income. Do I do one set of submissions or two?

Two. HMRC treats each income source separately for MTD purposes. You’d submit four quarterly updates for the property side and four for the trade — eight quarterly filings, plus the Final Declaration. Some software handles both in one place; some doesn’t. Worth checking before you commit.

My income is below £50,000. Am I safe?

Until April 2027, yes. Then the threshold drops to £30,000. April 2028 it drops again to £20,000. So “safe” is really just “later.” Getting your records digital now means a smoother landing whenever your turn comes.

Can I still use my accountant under MTD for Income Tax?

Absolutely — and most people will. Your accountant can submit on your behalf if they’re authorised through HMRC’s agent services. Many will set up the software, manage the bank feeds, and review quarterly figures before they go.

What happens if my income drops below £50,000 after I’ve joined MTD?

You stay in. You only leave once your qualifying income has been below the threshold for three consecutive years and HMRC confirms it. Joining is one-way traffic, more or less.

Are partnerships included in MTD for Income Tax in 2026?

No. Partnerships have been deferred. The government has said they’ll be brought in later, but no firm date. If you’re a partner and have a separate sole trade or rental in your own name, that personal income is still in scope.

Do I need to keep paper receipts at all under MTD for Income Tax?

You don’t need paper — the digital record of the transaction (date, amount, category) is what’s required. But you still need to be able to evidence everything if HMRC asks, so most people end up snapping receipts into their software anyway. Belt and braces.