Every December, there’s a particular type of panic that settles over British boardrooms. It’s not the Christmas party budget—though that’s stressful enough—it’s the dawning realisation that Companies House filing deadlines are approaching faster than a London bus in rush hour traffic.

Here’s what nobody tells you about corporate accounting: it’s not just about ticking boxes. The difference between a company that thrives and one that merely survives often lies in how they handle their year-end obligations. I’ve watched brilliant entrepreneurs stumble at this hurdle, not because they lack business acumen, but because they treat accounting for a corporation as an afterthought rather than a strategic tool.

The truth is, modern accounting for a corporation has evolved far beyond simple bookkeeping. UK businesses face a labyrinth of compliance requirements, tax optimisation opportunities, and reporting standards that would make even seasoned accountants reach for their second coffee of the morning.

The Hidden Costs of DIY Corporate Accounting

Let me paint you a picture: Sarah runs a successful tech consultancy in Manchester. Last year, she decided to handle her company’s year-end filing herself. “How hard could it be?” she thought. Three months, two HMRC penalties, and one very expensive correction later, she had her answer.

The problem isn’t that business owners are incompetent—far from it. The issue is that accounting for a corporation requires a specific skill set that doesn’t naturally overlap with running a business. Consider the sheer volume of requirements: Corporation Tax returns, annual accounts, confirmation statements, dividend vouchers, and that’s before we even touch on sector-specific regulations.

What Sarah discovered (the hard way) is that modern corporate accounting involves multiple moving parts that must work in harmony. Miss one component, and the entire system becomes unstable. Professional accounting for a corporation services can prevent these costly mistakes whilst providing strategic insights for business growth.

Decoding the Corporation Tax Puzzle

Corporation Tax isn’t just about calculating 19% or 25% of your profits—though the recent rate changes have certainly added complexity. The real challenge lies in understanding what counts as profit in the first place.

| Profit Band | Tax Rate | Key Considerations |

| Up to £50,000 | 19% | Small profits rate – straightforward calculation |

| £50,001 – £250,000 | Marginal rate | Tapered relief applies – complex calculation |

| Above £250,000 | 25% | Main rate – but watch for group relief opportunities |

The devil, as they say, is in the details. Pre-trading expenses, capital allowances, research and development credits—each represents both an opportunity and a potential pitfall. Get it right with proper accounting for a corporation expertise, and you could save thousands. Get it wrong, and you’ll be explaining discrepancies to HMRC for months.

Take capital allowances, for instance. Most business owners know they can claim for equipment, but how many realise that integral features of buildings—air conditioning, lifts, even certain flooring—qualify for enhanced capital allowances? These aren’t just tax technicalities; they’re legitimate ways to reduce your corporation tax liability through strategic accounting for a corporation planning.

The Annual Accounts Minefield

Annual accounts feel like they should be straightforward: income minus expenses equals profit. If only it were that simple.

The reality is that professional accounting for a corporation requires adherence to specific reporting standards that can transform a seemingly profitable year into a loss (or vice versa). Depreciation methods, stock valuation, accruals versus cash accounting—each decision cascades through your entire financial picture.

I’ve seen companies accidentally overstate their profits by treating capital expenditure as revenue costs, leading to inflated tax bills and confused stakeholders. Conversely, conservative accounting practices can sometimes mask genuine business success, making it harder to secure funding or attract investors.

The experience here matters tremendously. When you’re dealing with complex accounting for a corporation requirements, having someone who understands both the technical requirements and business implications becomes invaluable.

Why Timing Matters More Than You Think

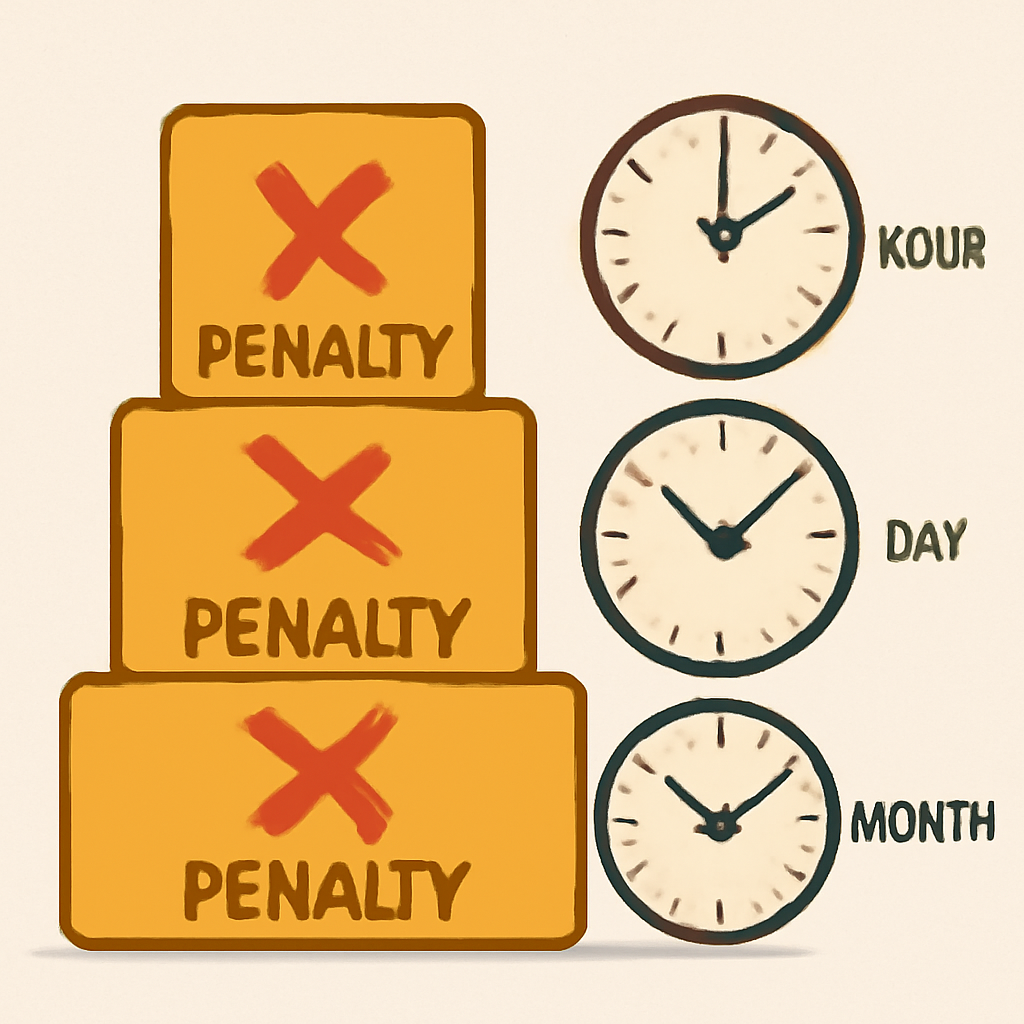

Here’s something that catches many business owners off-guard: when you file matters almost as much as what you file. Miss your filing deadline, and you’re looking at automatic penalties starting at £150 for small companies, scaling up to £1,500 for larger operations.

But the real kicker? These penalties apply even if you don’t owe any tax. Companies House doesn’t care about your circumstances—they care about compliance.

| Filing Delay | Penalty Amount | Additional Consequences |

| 1 day late | £150 | Warning letters commence |

| 3 months late | £375 | Credit rating impact begins |

| 6 months late | £750 | Strike-off proceedings possible |

| 12 months late | £1,500 | Compulsory dissolution likely |

The financial penalties are just the beginning. Late filing can trigger HMRC enquiries, damage your credit rating, and in extreme cases, lead to compulsory strike-off proceedings. For directors, this can mean personal liability for company debts—a prospect that keeps many business owners awake at night.

Proper accounting for a corporation services ensure deadlines are never missed, protecting both your business and personal interests.

The Digital Revolution in Corporate Accounting

Making Tax Digital (MTD) has fundamentally changed how UK businesses approach accounting for a corporation. What started as a VAT requirement is gradually expanding to cover Corporation Tax, and the implications are significant.

Digital record-keeping isn’t just about using accounting software—it’s about creating an audit trail that HMRC can follow from transaction to tax return. This means your accounting processes need to be more robust, more transparent, and more integrated than ever before.

The businesses that are thriving under MTD are those that embraced digital accounting for a corporation early. They’re using cloud-based systems that automatically categorise transactions, flag potential issues, and generate real-time reports. More importantly, they’re making decisions based on current data rather than historical snapshots.

Strategic Tax Planning vs. Compliance

There’s a crucial distinction between tax compliance and tax planning that many business owners miss. Compliance is about meeting your legal obligations—filing returns on time, paying what you owe, keeping proper records. Tax planning is about minimising your tax liability through legitimate strategies within your accounting for a corporation framework.

Smart tax planning for corporations might include:

- Timing strategies: Accelerating expenses or deferring income to optimise your tax position across multiple years. This isn’t about creative accounting—it’s about understanding the tax implications of business decisions through expert accounting for a corporation guidance.

- Pension contributions: Corporate pension schemes offer some of the most tax-efficient ways to extract profits from your business. The interaction between corporation tax relief and personal tax benefits can be complex, but the savings are substantial.

- Group relief: If you operate multiple companies, group relief can help offset losses in one entity against profits in another. This requires careful planning and proper documentation within your accounting for a corporation strategy, but the tax savings can be significant.

The Human Element in Corporate Accounting

Behind every set of accounts lies a human story. The entrepreneur who mortgaged their house to fund the business. The family company navigating succession planning. The startup burning through investor cash while chasing product-market fit.

This is where services like those offered by Ask Accountant become invaluable. Located at 178 Merton High St, London SW19 1AY, they understand that accounting for a corporation isn’t just about number-crunching—it’s about understanding the business context behind the figures. Their comprehensive approach includes inheritance tax planning, business advice, CIS claims and refunds, and proactive tax advisory solutions that align with your long-term objectives.

Their bookkeeping and auto-enrolment services ensure your day-to-day operations run smoothly, whilst their business growth planning helps you make strategic decisions based on solid financial foundations. You can reach them at +44(0)20 8543 1991 to discuss how their expertise in accounting for a corporation can support your specific business needs.

Red Flags That Signal Accounting Problems

Certain warning signs indicate that your corporate accounting might be heading for trouble:

- Inconsistent monthly results: If your profit margins vary wildly from month to month without clear business reasons, it suggests underlying issues with your accounting for a corporation processes.

- Cash flow versus profit discrepancies: Profitable companies can still struggle with cash flow, but if the gap between reported profits and available cash is widening, you need to investigate your accounting practices.

- Delayed management accounts: If you’re consistently waiting weeks or months for financial reports, your accounting for a corporation system isn’t serving your business needs effectively.

- High error rates: Frequent corrections, amendments, or disputed figures suggest systemic problems that need addressing through professional accounting for a corporation support.

These aren’t just accounting issues—they’re business issues that can undermine decision-making and strategic planning.

The Technology Factor

Modern accounting for a corporation is impossible without appropriate technology. But technology alone isn’t the answer—it’s how you use it within your overall accounting strategy that matters.

The most successful businesses are those that integrate their accounting software with other business systems. Customer relationship management, inventory control, payroll processing—when these systems talk to each other, they create a comprehensive view of business performance that goes far beyond traditional accounting for a corporation approaches.

Cloud-based accounting platforms have democratised access to sophisticated financial tools. Small businesses can now access the same level of reporting and analysis that was once reserved for large corporations. The challenge is choosing the right tools and implementing them effectively within your accounting for a corporation framework.

Practical Steps for Better Corporate Accounting

If you’re struggling with accounting for a corporation, here are some practical steps to consider:

- Monthly management accounts: Don’t wait until year-end to understand your financial position. Monthly accounts help you identify trends, spot problems early, and make informed decisions about your business direction.

- Regular reconciliations: Bank reconciliations, VAT reconciliations, and balance sheet reconciliations should be routine, not year-end exercises. This forms the backbone of reliable accounting for a corporation.

- Documentation standards: Maintain clear records of all transactions, including supporting documentation. This makes year-end much smoother and reduces the risk of errors in your accounting for a corporation processes.

- Professional support: Consider whether you have the right level of professional support. For many businesses, the cost of expert accounting for a corporation advice is more than offset by the savings in tax, penalties, and management time.

Looking Forward: The Future of Corporate Accounting

The landscape of accounting for a corporation continues to evolve rapidly. Artificial intelligence is beginning to automate routine tasks, freeing up time for strategic analysis. Real-time reporting is becoming the norm rather than the exception. Environmental, social, and governance (ESG) reporting is moving from nice-to-have to essential.

But perhaps the most significant change is the shift from reactive to proactive accounting for a corporation. Instead of simply recording what happened, modern corporate accounting helps predict what might happen and guides decision-making accordingly.

This requires a different mindset—one that views accounting for a corporation as a strategic tool rather than a compliance burden. It means investing in systems, processes, and people who can deliver insights, not just information.

The Bottom Line

Accounting for a corporation isn’t just about compliance—it’s about creating a foundation for sustainable business growth. The companies that get this right are those that view accounting as a strategic investment rather than a necessary evil.

The complexity of modern corporate accounting means that trying to handle everything in-house is often a false economy. The time you spend wrestling with tax codes and filing requirements is time you’re not spending on growing your business.

Whether you’re a startup founder filing your first accounts or an established business owner looking to optimise your tax position, the key is to approach accounting for a corporation with the seriousness it deserves. Your future self will thank you for the investment.

For businesses ready to take their financial management to the next level, professional support makes all the difference. Expert accounting for a corporation services provide the technical expertise, strategic insights, and peace of mind that allow you to focus on what you do best—running your business.

Remember: good accounting doesn’t just keep you compliant—it gives you the insights you need to build a better business.

Frequently Asked Questions

Q: How often should I review my corporation’s accounting position?

A: Monthly reviews are ideal for most businesses. This allows you to spot trends, address issues early, and make informed decisions based on current data rather than historical information. Professional accounting for a corporation services often include monthly management reporting as standard.

Q: What’s the difference between management accounts and statutory accounts?

A: Management accounts are internal reports designed to help you run your business, whilst statutory accounts are formal documents required by law. Management accounts can be more detailed and tailored to your specific needs within your accounting for a corporation framework.

Q: Can I handle corporation tax myself?

A: Whilst legally possible, corporation tax involves complex calculations and numerous opportunities for optimisation that require expertise. The cost of professional accounting for a corporation help is often offset by tax savings and reduced compliance risks.

Q: What happens if I miss my filing deadline?

A: Automatic penalties start at £150 and increase with time. Beyond financial penalties, late filing can trigger HMRC enquiries and damage your business credit rating. Professional accounting for a corporation services ensure deadlines are never missed.

Q: How do I know if my accounting software is suitable for my business?

A: Your software should handle your transaction volume, integrate with other business systems, provide the reports you need, and comply with Making Tax Digital requirements. If you’re constantly working around limitations, it’s time to upgrade your accounting for a corporation technology stack.