There’s a particular kind of dread that comes with a letter from HMRC. You know the one — stiff envelope, official font, the word “investigation” sitting there on the page like a small explosion. Most people’s first instinct is to either phone someone in a panic or shove the letter in a drawer and pretend it didn’t arrive. Neither approach, unfortunately, is especially useful.

The truth is, a tax investigation doesn’t have to be a catastrophe. It can feel like one. It often starts like one. But the people who come through these processes with the least damage — financially and emotionally — tend to be the ones who understood what was happening at each stage and responded with something resembling a plan rather than a pulse-raising scramble.

So, here’s the honest, unvarnished breakdown of the 5 stages of a tax investigation, what HMRC is actually doing at each point, and — crucially — what you should be doing about it.

Why HMRC Opens an Investigation in the First Place

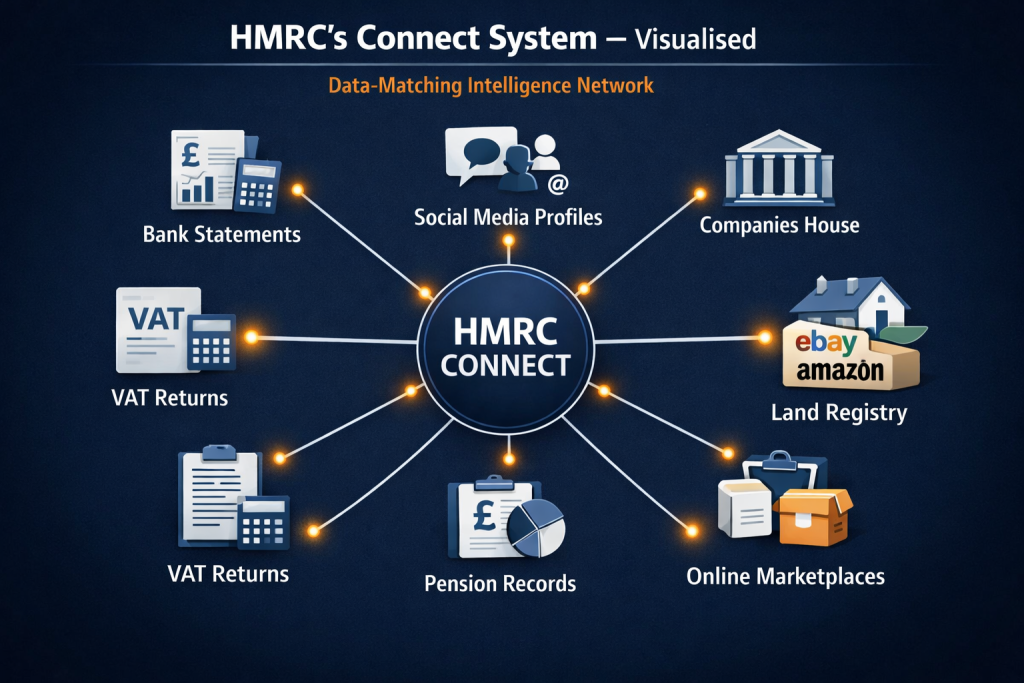

Before we get into the stages themselves, it helps to understand the mechanics of why these things happen. HMRC doesn’t randomly select people out of spite (though it can feel that way). Their Connect system — a frankly formidable data-matching tool — cross-references your tax returns against bank records, Land Registry data, Companies House filings, social media, and even online marketplace sales. If something doesn’t add up, a flag gets raised.

Common triggers include:

- Unusually large or sudden drops in declared income

- Inconsistencies between lifestyle indicators and reported earnings

- Late or amended tax returns filed repeatedly

- Tips or information received from third parties

- Industries HMRC considers “high risk” (construction, hospitality, cash-heavy trades)

- Random selection — yes, this genuinely happens

Worth noting: being investigated doesn’t automatically mean HMRC thinks you’ve committed fraud. Many investigations are triggered by honest mistakes, system anomalies, or just bad timing. The process is the same either way.

Stage 1: The Opening Letter — What It Actually Means

The first stage of a tax investigation begins when HMRC sends you an enquiry notice. This is typically issued under Section 9A of the Taxes Management Act 1970 for personal returns, or Section 12AC for partnerships. The letter will tell you:

- Which tax year(s) are under review

- What type of investigation is being conducted

- What information or documents they’re requesting

There are broadly three types of investigation you might be dealing with: a full enquiry (HMRC wants to look at everything), an aspect enquiry (they’re interested in one specific area, like a particular expense claim), or a PAYE compliance review for employers. Full enquiries are the most intensive; aspect enquiries are more targeted but can escalate if HMRC doesn’t like what they find.

What you should do immediately:

Don’t ignore it. Don’t reply without taking advice. The clock starts ticking from receipt of this letter — HMRC will expect a response within a set timeframe, and failing to engage promptly is one of the fastest ways to make a manageable situation considerably worse. Contact a tax adviser or accountant straight away, before you send a single word back to HMRC.

⚠ Quick Reality Check: Responding to HMRC yourself, without professional guidance, is a bit like representing yourself in a court case. You’re technically allowed to. It rarely ends well.

If you’re a business owner or sole trader in London, getting specialist support quickly matters enormously. The team at Ask Accountant deals with exactly this kind of situation — and the earlier you get someone experienced in your corner, the better your position.

Stage 2: Document Requests and the Paper Trail Problem

Once the investigation is formally open, HMRC will begin requesting documentation. This is where things get genuinely stressful for most people — not because they have anything to hide, but because finding coherent financial records spanning several years is, for many small business owners, an unexpectedly chaotic experience.

They might ask for:

- Bank statements (personal and business)

- Sales records, invoices, and receipts

- Payroll records

- VAT returns and supporting documentation

- Expense claims with corresponding receipts

- Details of any assets acquired during the period

HMRC is looking for discrepancies. A £40,000 holiday abroad that doesn’t appear to match your declared income. Business expenses that look suspiciously personal. Cash deposits that don’t reconcile with your books.

What you should do:

Gather everything your adviser asks for — but don’t volunteer information beyond what’s been requested. This sounds counterintuitive; surely being forthcoming is better? Not necessarily. Providing unrequested information can open new lines of enquiry and widen the investigation’s scope. Let your accountant or tax adviser decide what’s relevant and how to present it.

Also: now is an excellent time to deeply regret any gaps in your bookkeeping. I say this without judgement because it’s an extraordinarily common issue — but it’s also why having solid, up-to-date bookkeeping services from the outset saves so much pain later. Reactive record reconstruction is miserable. Proactive record-keeping is boring. Guess which one I’d recommend.

| Stage | What HMRC Is Doing | Documents Typically Requested | Your Priority Action |

|---|---|---|---|

| 1. Opening Notice | Formally notifying you of the enquiry | Nothing yet — just acknowledgement | Contact a tax adviser immediately |

| 2. Document Request | Building an evidential picture | Bank statements, invoices, VAT records, receipts | Gather records; don’t over-disclose |

| 3. Interviews / Meetings | Clarifying discrepancies in person | Summaries, narrative explanations, business records | Never attend alone; prepare with your adviser |

| 4. Findings & Assessment | Issuing a tax assessment or formal conclusion | Final document submissions if challenged | Review assessment carefully; consider appeal |

| 5. Settlement or Tribunal | Finalising the amount owed (or disputed) | Formal representations, legal submissions | Negotiate via adviser or escalate to tribunal |

Stage 3: The Interview — HMRC Meetings and Why They’re Not Like You Imagine

Not every tax investigation includes a face-to-face meeting. But when one is requested, it’s usually because HMRC wants clarification on something they haven’t been able to resolve through documentation alone. These meetings tend to happen in more complex cases — particularly where there are significant unexplained discrepancies, or where HMRC suspects deliberate underreporting.

Here’s what many people don’t realise: you are not legally obliged to attend an informal interview. HMRC can request one, but if it’s not a formal compelled interview under their civil investigation powers, you have more control than you might think. That said, refusing without good reason can sometimes harden HMRC’s position.

If an interview does go ahead, the dynamics are worth understanding. HMRC officers are trained in interrogative techniques. They’re not necessarily trying to trick you, but they are trying to elicit information. Silences feel uncomfortable; many people fill them with helpful (for HMRC) additional details they hadn’t planned to share.

What you should do:

Always, always take a professional representative with you. A tax adviser or accountant who knows your case acts as a buffer, can interrupt to clarify questions that are ambiguous, and will prevent you from inadvertently expanding the scope of the enquiry. Prepare thoroughly: know your numbers, know the timeline, know where any anomalies came from and have a coherent explanation ready.

Stage 4: The Assessment — When HMRC Tells You What They Think You Owe

This is often the stage that hits hardest. After gathering evidence and potentially meeting with you, HMRC will issue their findings — usually in the form of a tax assessment or a closure notice explaining what additional tax they believe is due, plus interest and (in many cases) penalties.

Penalty levels vary significantly depending on HMRC’s view of your behaviour:

- Prompted disclosure with reasonable care: as low as 0% penalty

- Prompted disclosure without reasonable care: 15–30%

- Deliberate understatement (disclosed): 20–35%

- Deliberate and concealed (prompted): 30–60%

- Deliberate and concealed (unprompted): up to 100% of the tax owed

The distinction between “careless” and “deliberate” behaviour carries enormous financial consequences. This is another reason why professional representation matters — an experienced adviser can often negotiate the behaviour category downward, resulting in significantly lower penalties.

What you should do:

Don’t simply accept the assessment without scrutiny. HMRC’s calculations are not infallible. Errors occur. If you believe the assessment is incorrect — whether in the underlying figures or the penalty classification — you have the right to challenge it. Your adviser will review the assessment in detail, identify any grounds for dispute, and advise whether to negotiate directly with HMRC or prepare a formal appeal.

| Behaviour Category | Unprompted Disclosure | Prompted Disclosure | Notes |

|---|---|---|---|

| Reasonable care taken | 0% | 0% | No penalty; just unpaid tax + interest |

| Careless (lack of reasonable care) | 0–30% | 15–30% | Most common category in HMRC enquiries |

| Deliberate understatement | 20–70% | 35–70% | Serious; professional help essential |

| Deliberate and concealed | 30–100% | 50–100% | Potential criminal investigation territory |

*Figures based on HMRC published guidance. Exact rates depend on individual circumstances and cooperation levels.

Stage 5: Settlement, Appeal, or Tribunal — The Road to Resolution

The final stage of a tax investigation is reaching a conclusion — and how that conclusion looks depends heavily on what’s happened in the previous four stages.

The majority of investigations are resolved through negotiated settlement. HMRC genuinely prefers this. Tribunal proceedings are expensive, time-consuming, and uncertain for both sides. If your adviser has maintained a constructive, cooperative tone throughout the process (without being a pushover), settlement is usually achievable.

Settlement involves agreeing the amount of additional tax owed, the penalty level, and sometimes a payment plan if the total sum is substantial. HMRC will then issue a contract settlement or closure notice, and the investigation formally ends.

But what if you don’t agree?

If HMRC’s assessment is demonstrably wrong — or if their penalty calculation is disproportionate — you can appeal. The appeal route runs through the First-tier Tax Tribunal, which is an independent body. It’s a genuinely adversarial process, and while many taxpayers win tribunal cases, it requires thorough preparation, strong evidence, and almost certainly specialist legal/tax representation.

What you should do:

Be honest with yourself (and your adviser) about the merits of your position. Appealing purely as a delay tactic tends to backfire, as interest continues to accrue on unpaid tax during tribunal proceedings. A good tax adviser will tell you frankly whether your case has real grounds for appeal or whether negotiating a reasonable settlement is the smarter path.

The Hidden Sixth Stage Nobody Talks About: What Comes After

Once the investigation closes, most people just want to move on and never think about HMRC again. Understandable. But there’s a practical consideration that often gets overlooked: HMRC may mark you as a higher-risk taxpayer following an investigation. This can mean you’re more likely to be selected for future enquiries, and it may influence how HMRC treats your subsequent returns.

The sensible response — boring as it sounds — is to get your financial housekeeping genuinely in order. Better record-keeping, cleaner bookkeeping, properly structured expenses. If the investigation revealed weaknesses in your systems, address them now.

Some businesses use the experience as a catalyst to move to cloud accounting platforms like Xero or QuickBooks, which create automatic, timestamped audit trails that hold up far better under scrutiny than a collection of crumpled receipts and an overloaded spreadsheet.

How Long Does a Tax Investigation Actually Take?

This is the question everyone asks, and the answer — genuinely — is: it depends. A simple aspect enquiry might be resolved within a few months. A full investigation involving multiple years, complex business structures, or alleged deliberate behaviour can drag on for two, three, sometimes four years.

Broadly speaking:

- Aspect enquiry: 3–12 months

- Full enquiry (cooperative): 12–24 months

- Full enquiry (disputed / complex): 2–5 years

- Criminal investigation: potentially much longer

The biggest factor within your control? How promptly and professionally you engage with the process. Delays in providing documentation, disputes over scope, or unnecessary back-and-forth caused by poorly framed responses all add time — and cost — to an already expensive process.

Can You Prevent a Tax Investigation? (Sort of.)

You can’t immunise yourself against an HMRC investigation — particularly if you’re in a sector HMRC scrutinises heavily, or if you’ve had past compliance issues. But you absolutely can reduce the probability of being flagged and reduce the damage if an enquiry does land.

The practical steps are unsexy but effective:

File on time, every time. Late returns are a red flag, full stop.

Make sure your returns are consistent year on year. Sudden swings in income or profit margins attract attention, especially if they’re not explained by obvious external factors.

Keep genuinely good records. Not just “I’ll sort this out at year-end” records. Real, contemporaneous records that could withstand scrutiny on any given day.

Take professional advice on tax planning. Proactive tax advisory solutions mean fewer errors, fewer ambiguous claims, and a return that’s much harder for HMRC to find fault with.

There’s also a practical product worth knowing about: Tax Investigation Insurance (sometimes called fee protection insurance). Many accountants offer this as part of their service or as an add-on. It covers the professional fees incurred in responding to an HMRC investigation — which can run into thousands of pounds for complex cases. Given that investigations can happen entirely at random, it’s worth considering.

Frequently Asked Questions About Tax Investigations

What triggers an HMRC tax investigation?

Several things can trigger a tax investigation: inconsistencies between your return and third-party data in HMRC’s Connect system, unusual changes in declared income, operating in a high-risk industry, receiving a tip-off, or simple random selection. HMRC doesn’t always disclose the exact reason.

Do I need an accountant for a tax investigation?

You’re not legally required to use one, but handling an HMRC investigation without professional support is genuinely risky. An experienced accountant or tax adviser knows how HMRC works, how to frame responses, what to disclose and what not to, and how to negotiate penalty reductions. The fees involved almost always represent good value against the potential cost of mishandling the process.

If you’re based in South West London, Ask Accountant at 178 Merton High St, SW19 offers specialist HMRC investigation support alongside their broader tax advisory services — you can reach them on +44(0)20 8543 1991.

What happens if I just ignore an HMRC investigation letter?

HMRC will escalate. Ignoring an enquiry notice doesn’t make it go away — it results in penalties for non-cooperation, potential assessments being made without your input (almost always unfavourable), and in serious cases, HMRC applying for formal information notices which carry their own penalties for non-compliance.

Is a tax investigation the same as a tax audit?

In UK terminology, HMRC uses the term enquiry or investigation rather than “audit.” The concept is broadly similar to what other countries call an audit — a detailed review of your tax position — but in the UK, “audit” more commonly refers to the statutory audit of a company’s financial statements, which is a separate matter entirely.

The Bottom Line

A tax investigation is stressful. It’s time-consuming. It can be expensive. But it is survivable — and for the many people who get through one each year without any additional liability, it ends up being more of an administrative ordeal than a financial disaster.

What makes the difference, consistently, is preparation and professional support. Good records, honest returns, and a specialist in your corner when HMRC comes knocking. The 5 stages of a tax investigation follow a predictable enough path that anyone who understands them can navigate the process without panicking — or at least with slightly less panicking.

If HMRC has been in touch, or if you’re just trying to get your financial affairs into better shape before anything goes wrong, Ask Accountant can help. Their team provides HMRC investigation support, business accounting services, bookkeeping, personal tax planning, and business advisory — all from their office on Merton High Street, London SW19.

Sometimes, the best time to call an accountant is before anything goes wrong. But the second best time is right now.