Somewhere between “I’ll sort my VAT out properly one day” and the panic of a looming return deadline, most small business owners in the UK stumble across the VAT Flat Rate Scheme. It gets pitched as the easy option — pay HMRC one fixed percentage, skip the receipt-hoarding, get on with your actual job. And for a good chunk of businesses, that pitch is true. For others, particularly service businesses with barely any stock cupboard to speak of, the VAT Flat Rate Scheme can quietly cost more than doing things the traditional way. So which camp are you in? That’s what this guide is here to untangle.

If you’ve never dealt with VAT before: every VAT-registered business normally charges customers VAT on sales, reclaims VAT on purchases, and pays HMRC the difference. It’s fiddly but fair. The VAT Flat Rate Scheme swaps that calculation for something blunter — you still charge customers the standard 20% VAT, but instead of working out what you’ve reclaimed, you hand over a single fixed percentage of your gross (VAT-inclusive) turnover, and whatever’s left in the gap is yours to keep. Simple in theory. In practice, the size of that gap depends entirely on your sector, your spending habits, and one HMRC rule that catches out more freelancers than it probably should.

How the VAT Flat Rate Scheme Actually Works Day to Day

Here’s the bit that trips people up: you don’t stop charging VAT normally. Your invoices still show 20%. Your clients pay exactly what they’d pay any other VAT-registered supplier. The only thing that changes is what happens on your side of the ledger.

Say you invoice a client £1,000 plus VAT — they pay you £1,200. Under standard VAT accounting, you’d hand over roughly £1,200 minus whatever VAT you’d paid on business costs that quarter. Under the Flat Rate Scheme, you apply a sector-specific percentage to that £1,200 and pay that instead, full stop. No digging through receipts for allowable input VAT (with one exception we’ll come to). No quarterly reconciliation headache.

That trade-off — simplicity for precision — is really the whole pitch of the VAT Flat Rate Scheme. Whether it’s a good trade depends on how much VAT you’d normally be reclaiming anyway.

Who Can Actually Join

Not every business gets to opt in, and not every business that joins gets to stay. The eligibility rules are fairly forgiving at the entry point:

- You must be VAT-registered (mandatory once taxable turnover passes £90,000 in a rolling 12-month period)

- Your expected VAT-taxable turnover for the next 12 months must be £150,000 or less, excluding VAT

- You mustn’t have left the Flat Rate Scheme in the previous 12 months

- You can’t be part of a VAT group, and a relevant VAT offence in your history can disqualify you too

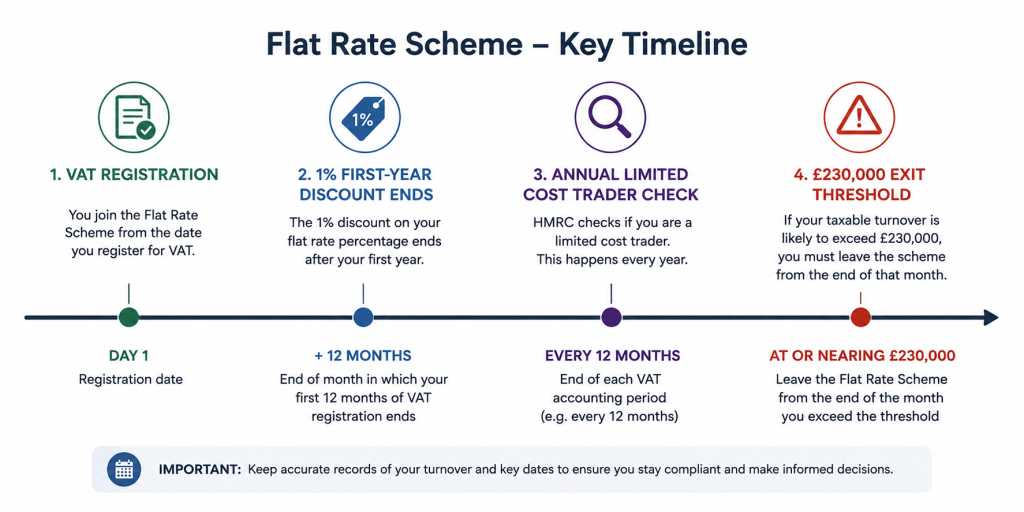

You apply either when you first register for VAT, through your Government Gateway VAT account afterwards, or by post using form VAT600 FRS. HMRC writes back to confirm your start date — usually the beginning of your next VAT accounting period, not retrospectively.

On the way out, the number to watch is £230,000. Once your total VAT-inclusive income for the year exceeds that, you generally have to leave the VAT Flat Rate Scheme (there’s a narrow exception if HMRC agrees your turnover will drop back under £191,500 the following year). Miss the notification deadline and you risk incorrect returns — and penalties nobody enjoys explaining to HMRC.

Sector Rates: Why “Flat” Doesn’t Mean “The Same for Everyone”

This is where the scheme gets its name and its complexity in equal measure. HMRC doesn’t hand every business the same percentage — there’s a published table covering more than 50 trade categories, and your rate depends on which one your business falls into (by main activity, if you cover more than one). Below is a snapshot of common categories — always check the full HMRC table before applying, as figures do get revised.

| Business type | Flat rate % | Notes |

|---|---|---|

| Accountancy or book-keeping | 14.5% | — |

| Computer and IT consultancy | 14.5% | |

| Management consultancy | 14% | watch the limited cost trader test |

| Advertising | 11% | |

| Photography | 11% | — |

| Hairdressing | 13% | |

| Catering (incl. takeaways) | 12.5% | — |

| Pubs | 6.5% | one of the lowest rates going |

| Retail (not elsewhere listed) | 7.5% | |

| Limited cost trader | 16.5% | applies regardless of sector — see below |

Notice the spread. A pub at 6.5% and an IT consultant at 14.5% are playing an entirely different game, even though both are “on the VAT Flat Rate Scheme.”

The Limited Cost Trader Rule (Or: Why the Scheme Stopped Being a Freebie)

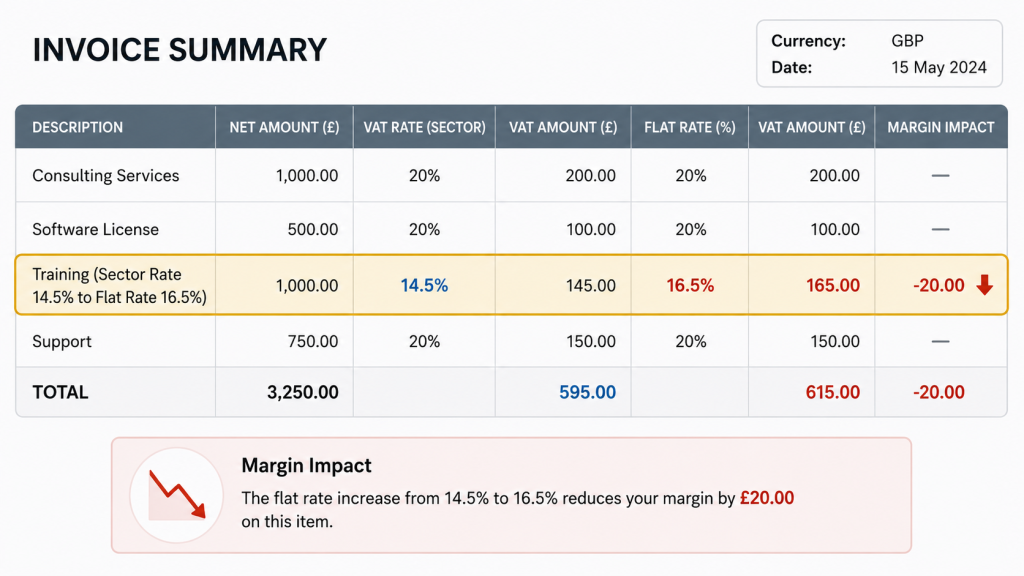

If there’s one section of this article worth reading twice, it’s this one. Back in 2017, HMRC noticed that certain service businesses — consultants, contractors, designers, anyone whose main cost is their own time — were pocketing a tidy margin on the Flat Rate Scheme simply because they barely bought anything. So HMRC introduced the limited cost trader test, and it changed the calculus for a huge swathe of small businesses.

Quick gut-check: if your biggest monthly outgoings are salaries, subcontractors, software subscriptions, rent, or professional fees, none of that counts as “goods” for this test. Only physical items used exclusively for your business count — and even then, capital assets, food, drink, and vehicle costs are specifically excluded.

You’re classed as a limited cost trader if your VAT-inclusive spending on relevant goods is either:

- Less than 2% of your VAT-inclusive turnover in that quarter, or

- Less than £1,000 a year (pro-rated for your return period) — even if that’s technically more than 2%

Fall into that bracket and your rate isn’t your sector’s rate anymore. It’s 16.5%, full stop, regardless of whether you’re a photographer, a management consultant, or an events planner. And because you’re still charging clients 20% VAT, that only leaves a wafer-thin 3.5 percentage points of headroom — which, once you factor in irrecoverable input VAT on your costs, can leave you worse off than standard VAT accounting altogether.

The test isn’t a one-off either. You have to check your position every single return period, because spending patterns shift — a quiet quarter with low costs can flip you into limited cost trader status even if last quarter you weren’t.

Running the Numbers: A Worked Comparison

Numbers convince better than adjectives, so here’s a simple side-by-side. Meet a freelance IT contractor invoicing £8,000 a month plus VAT (£9,600 gross).

| Scenario | Rate applied | Amount paid to HMRC/month | Kept in the business |

|---|---|---|---|

| Standard VAT accounting | VAT charged minus VAT reclaimed | approx. £1,600 (minimal input VAT to offset) | Very little margin |

| Flat Rate Scheme — IT consultancy rate | 14.5% of £9,600 | £1,392 | ~£208 saving |

| Flat Rate Scheme — limited cost trader | 16.5% of £9,600 | £1,584 | ~£16 saving |

That’s the whole argument in one table. Same business, same invoices — and whether the VAT Flat Rate Scheme is worth the paperwork swap comes down almost entirely to which row you land in.

Where the Scheme Genuinely Wins

I don’t want to talk this scheme down entirely — plenty of businesses do well on it, and dismissing it outright would be doing them a disservice. The VAT Flat Rate Scheme tends to suit you if:

- Your main cost is your time, but your sector rate is comfortably below 16.5% and you’re not caught by the limited cost trader test

- You’d rather spend an afternoon on client work than reconciling every purchase invoice against VAT rules

- Cash flow matters to you — the scheme runs on a cash basis, so you only pay HMRC on money you’ve actually received that quarter, not invoices still sitting unpaid

- You’re newly VAT-registered, because you get an automatic 1% discount on your sector rate for the first 12 months (drop from, say, 14.5% to 13.5%, or from 16.5% to 15.5% if you’re a limited cost trader)

Where It Quietly Costs You

On the flip side, think twice — or get a proper comparison run — if:

- You’re classified (or likely to become classified) as a limited cost trader

- Your business spends heavily on VAT-eligible goods or stock, where you’d reclaim more under standard accounting

- A large chunk of your sales are zero-rated or exempt — the flat rate still applies to your full gross turnover, VAT-free sales and all

- You regularly buy equipment or tools below £2,000 — under the Flat Rate Scheme you simply can’t reclaim VAT on those, whereas standard accounting would let you

- You’re edging toward the £230,000 exit threshold, meaning you’ll be switching schemes soon regardless

There is one carve-out worth remembering: capital purchases costing £2,000 or more (VAT included) on a single item can still have their VAT reclaimed under the Flat Rate Scheme. New laptop for £900? No reclaim. New van at £15,000? Reclaimable.

Joining, Leaving, and the Small Print Nobody Reads

A few practicalities that tend to get skipped over:

- Applying: through your VAT online account, at initial registration, or via form VAT600 FRS by post

- Leaving voluntarily: you can exit the VAT Flat Rate Scheme any time by writing to HMRC — but once you’re out, you can’t rejoin for 12 months, so don’t do it on a whim

- Making Tax Digital: the scheme is fully MTD-compatible; you still need to keep digital records and file through MTD software, same as any other VAT scheme

- Multiple activities: if your business genuinely spans two sectors, you use the rate for whichever activity makes up the bigger share of your turnover — not an average of the two

None of this is insurmountable, but it’s exactly the kind of detail that’s easy to get wrong when you’re doing your own books between client calls. It’s the sort of question we get asked fairly often at Ask Accountants UK Ltd — usually from a sole trader who joined the scheme two years ago on someone’s casual recommendation and has never actually checked whether it still makes sense.

So, Is the VAT Flat Rate Scheme Right for Your Business?

Honestly? It depends — and I know that’s an unsatisfying answer after 1,500-odd words, but it’s the true one. The VAT Flat Rate Scheme rewards businesses with genuinely low goods spending and a favourable sector rate. It punishes businesses that look low-cost on paper but get swept into the 16.5% limited cost trader bracket. The only way to know which side of that line you sit on is to actually run your own numbers — real invoices, real costs, real percentages — rather than go on what worked for someone else’s business.

If you’d rather not spend an evening cross-referencing HMRC’s sector table against your last four VAT quarters, that’s precisely the sort of accounts and tax work we handle daily. Alongside VAT scheme reviews, our bookkeeping service and cloud accounting support mean the numbers are already sitting there ready to check, rather than needing to be dug out of a shoebox first.

Frequently Asked Questions

Can I reclaim VAT on purchases under the Flat Rate Scheme? Generally, no — the flat rate percentage is calculated to already account for typical input VAT. The one exception is capital goods costing £2,000 or more including VAT.

What happens if I’m classed as a limited cost trader? You must apply the 16.5% flat rate instead of your normal sector rate, regardless of what your sector is. This test is checked every VAT return period, not just once.

How much can I earn and still join the VAT Flat Rate Scheme? Your expected VAT-taxable turnover for the next 12 months needs to be £150,000 or less, excluding VAT.

When do I have to leave the scheme? Once your total VAT-inclusive income passes £230,000 in a 12-month period, you’re generally required to leave.

Is the Flat Rate Scheme compatible with Making Tax Digital? Yes. You still need MTD-compatible software and digital record-keeping, regardless of which VAT scheme you use.

Can sole traders use the Flat Rate Scheme? Yes — the same thresholds and conditions apply whether you’re a sole trader, a partnership, or a limited company.

If any of this leaves you unsure where your own business sits, Ask Accountants UK Ltd, based at 178 Merton High St, London SW19 1AY, can talk it through — call 020 8543 1991, or read more on how HMRC handles enquiries in our guide to what happens during a tax investigation, since VAT scheme errors are a common trigger for HMRC to take a closer look. For broader questions on structuring your finances well beyond VAT, our inheritance and estate planning guidance is worth a browse too.

For the official word, HMRC’s own VAT Notice 733: Flat Rate Scheme for small businesses is the definitive source on current rates, thresholds, and the limited cost trader test — worth bookmarking, because the detail does get revised from time to time.