Right, let’s get something out of the way immediately: a director’s loan account is not a secret piggy bank. I wish someone had told me that plainly the first time I sat across from a client who’d “borrowed” £22,000 from his own company to fix a leaky roof and had absolutely no idea he’d just triggered a tax charge. He wasn’t uninformed by choice — he just didn’t know the rules. Most directors don’t, until the accountant’s letter arrives with a number on it they weren’t expecting.

A director’s loan account, or DLA if you want to sound like you’ve been doing this for years, is simply the running ledger of money moving between you and your limited company that isn’t salary, dividends, or a legitimate expense claim. Take more out than you’ve put in, and you’re overdrawn. Sounds harmless. It rarely stays that way.

This piece walks through what a director’s loan account actually is, when HMRC starts paying attention, what Section 455 tax will cost you, and how to keep the whole thing tidy enough that nobody at Ask Accountants UK Ltd has to deliver you bad news at year-end.

So What Actually Counts as a Director’s Loan?

Here’s the bit people get wrong constantly. A director’s loan account records every transaction between you and the company that doesn’t fit neatly into payroll. That includes:

- Cash withdrawals that aren’t salary or a declared dividend

- Personal expenses the company happened to pay for

- Money you put into the business informally (this credits your account, which is the good direction)

- Anything paid on your behalf that isn’t a genuine, receipted business cost

Note what’s not on that list — proper expense reimbursements, salary through PAYE, and dividends voted through the books correctly. Those live elsewhere. A director’s loan account only tracks the grey area in between, and that grey area usually grows quietly.

When Does a Director’s Loan Account Tip Into Overdrawn Territory?

The moment your withdrawals outpace what you’ve contributed or earned, the account flips negative — you owe the company, not the other way round. This happens more easily than you’d think. A few personal Amazon orders on the company card in November, a “just this once” cash withdrawal before Christmas, and by March you’ve quietly built an overdrawn director’s loan account without any single transaction feeling like a big deal.

It’s the accumulation that catches people out, not any one decision.

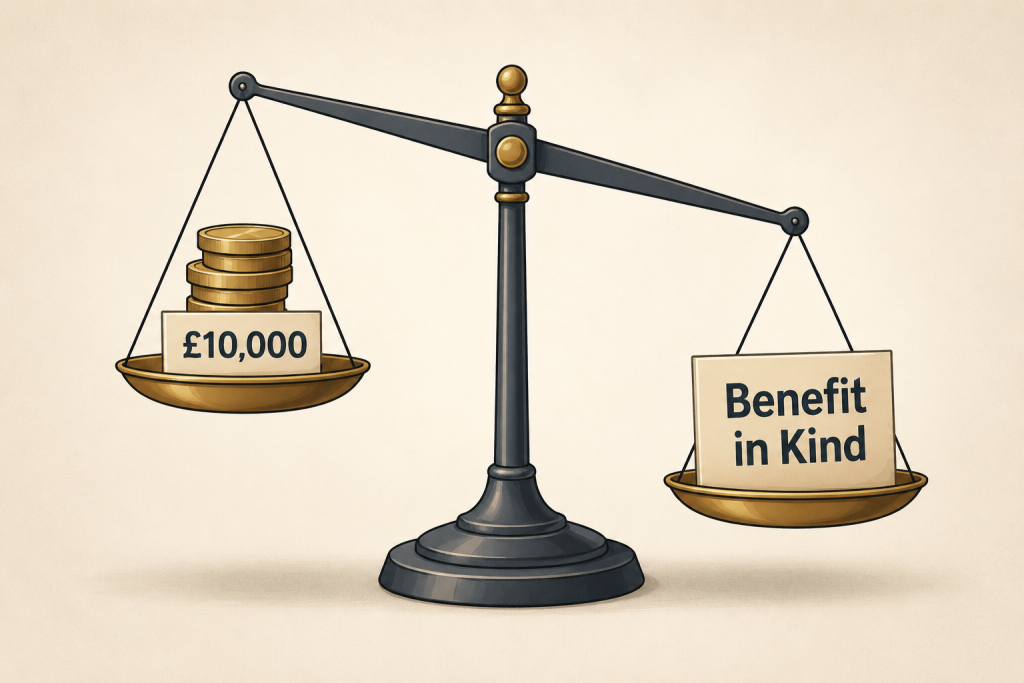

The £10,000 Line HMRC Actually Cares About

There’s a threshold worth tattooing on the inside of your eyelids: £10,000. If your overdrawn director’s loan account exceeds that at any point during the tax year — even for a single day — HMRC treats it as a benefit in kind, assuming you’re not charging yourself proper interest.

HMRC uses something called the “official rate of interest” to judge what “proper” means. That rate currently sits at 3.75% (reviewed quarterly since HMRC dropped its old promise not to move it mid-year — a change that’s tripped up plenty of otherwise switched-on directors). Charge yourself less than that, or nothing at all, and the shortfall becomes taxable.

| Loan Balance | Interest Charged? | Benefit in Kind Applies? | Who Pays What |

|---|---|---|---|

| Under £10,000 | No | No | Nothing extra |

| £20,000 | None | Yes | Director: Income Tax on ~£750 benefit / Company: Class 1A NIC via P11D |

| £30,000 | At or above 3.75% | No | Nothing extra, provided interest is genuinely paid |

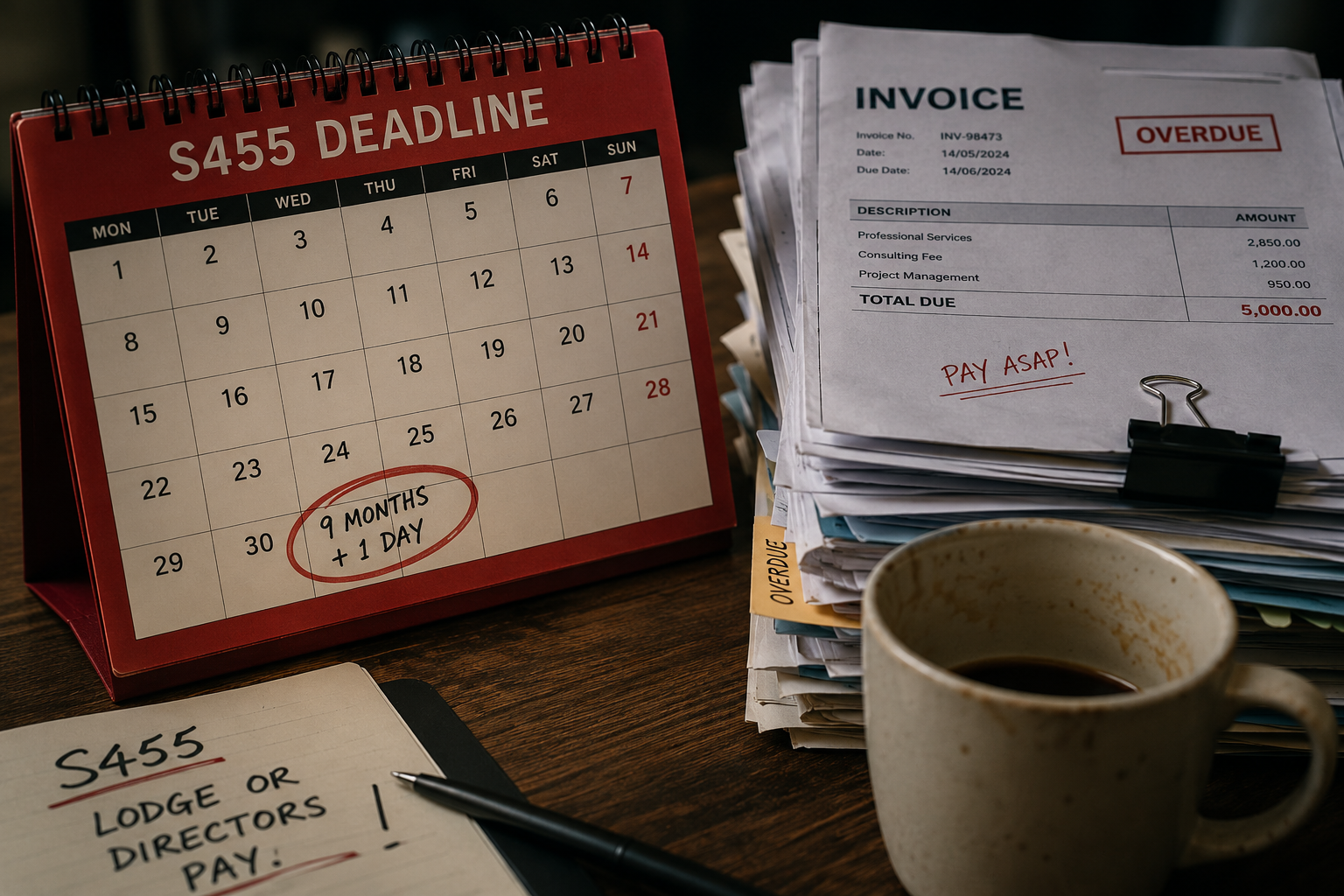

Section 455: The Sting in the Tail for an Overdrawn Director’s Loan Account

This is the part that genuinely stings, and it’s why I keep banging on about it to anyone who’ll listen. If a director’s loan account is still overdrawn nine months and one day after the company’s accounting period ends, the company — not you personally — pays a corporation tax charge under Section 455 of the Corporation Tax Act 2010.

The rate tracks the dividend upper rate, which is why it keeps creeping up. It sat at 33.75% for years. Then, following the Autumn Budget 2025, it rose to 35.75% for any loan made or benefit conferred on or after 6 April 2026. Two percentage points doesn’t sound dramatic until you’re staring at the invoice.

Here’s a rough table showing what that means in cash terms — and I’ll be honest, I’ve deliberately left this one a bit rough round the edges, because real working papers rarely line up perfectly either:

| Outstanding Balance | Old Rate (33.75%) | New Rate — from 6 April 2026 |

| £10,000 | £3,375 | 35.75% → £3,575 |

| £20,000 loan | £6,750 | £7,150 |

| £50k | £16,875.00 | £17,875 |

Getting the Section 455 Tax Back

The good news, such as it is: you can reclaim Section 455 tax once you repay the loan — but not quickly. The company has to wait until nine months and one day after the end of the accounting period in which the repayment happened, then claim it back via form L2P or the CT600A supplementary pages if it’s still within two years. In practice, that money can sit with HMRC for well over a year. Effectively an interest-free loan running in the wrong direction.

Nine Months and One Day — Mark It in Red

Why nine months and one day, specifically? Because that’s the standard Corporation Tax payment deadline, and Parliament decided to hang the director’s loan account rules off exactly the same date. Tidy, in a bureaucratic sort of way.

Practically, this means:

- Know your company’s accounting period end date cold.

- Review the director’s loan account balance quarterly, not just when the accountant asks.

- If it’s overdrawn close to year-end, plan the fix — a dividend (if reserves allow), a bonus, or an actual bank transfer — well before the deadline, not two days before.

Bed and Breakfasting: HMRC’s Least Favourite Trick

Someone, somewhere, once thought: “What if I repay the loan the day before year-end, then borrow it straight back the day after?” HMRC thought of this decades ago and built anti-avoidance rules specifically to kill it — informally nicknamed “bed and breakfasting.” Repay and re-borrow within 30 days, or arrange to do so before repayment, and HMRC will look straight through it and charge Section 455 anyway, on the original loan, as if you’d repaid nothing at all.

Don’t try it. Genuinely, don’t.

What Happens If a Director’s Loan Is Never Repaid?

Sometimes a loan just… stays. The director can’t or won’t repay it, and eventually the company writes it off. Careful here, because writing off a director’s loan account balance isn’t a clean exit — HMRC generally treats the written-off amount as a distribution, taxable on the director broadly like a dividend, on top of whatever Section 455 history already exists.

Director’s Loans and Inheritance Tax: The Overlap Nobody Mentions

There’s a knock-on angle people rarely think about, too. If a director dies with an outstanding loan owed to the company, that loan counts as an asset of their estate, and the executor must deal with it as part of probate and estate administration — worth understanding alongside general inheritance tax planning. Conversely, if the company (or the remaining directors) chooses to write the loan off after death, HMRC can treat that release as a gift for Inheritance Tax purposes, potentially falling under the seven year rule for gifts. It’s a genuinely awkward overlap between corporate tax and personal estate planning that catches executors off guard — anyone handling an executor’s inheritance tax forms after a director’s death should flag any outstanding DLA balance early, ideally alongside broader estate administration work.

Keeping Records Straight (Because HMRC Will Ask)

I’ll admit — bookkeeping is the boring bit. Nobody starts a business dreaming of ledger entries. But an untidy director’s loan account is one of the fastest ways to invite scrutiny, because it’s exactly the kind of thing HMRC’s risk-profiling software flags automatically. Round numbers, vague descriptions, transactions dated suspiciously close to year-end — all of it stands out.

Good practice, briefly:

- Log every transaction as it happens, not from memory three months later

- Separate personal and business spending completely (yes, get the second card)

- Reconcile the DLA at least quarterly

- Keep receipts and board minutes for anything unusual

If HMRC Opens an Investigation Into a Director’s Loan Account

Overdrawn director’s loan accounts are a genuinely common trigger for closer HMRC attention, particularly where balances swing wildly or write-offs appear without explanation. Understanding what happens during a tax investigation helps take some of the panic out of an already unpleasant letter. Broadly, HMRC will request the DLA ledger, bank statements, and board minutes covering the period in question, and work through the tax investigation process methodically — it’s rarely instant, and the tax investigation timeline can run for months. Getting proper tax investigation support early on, before you’ve responded to HMRC yourself, tends to save both money and sleep.

Frequently Asked Questions

What is a director’s loan account, in plain English? It’s the record of money moving between a director and their company outside of salary, dividends, and legitimate expenses. If you take out more than you’ve put in, the account is overdrawn and you owe the company.

How much tax will I pay on an overdrawn director’s loan account? The company pays Section 455 tax — currently 35.75% of the outstanding balance for loans taken out from 6 April 2026 — if you don’t clear the loan within nine months and one day of the accounting period end. Separately, the director may face a personal benefit-in-kind charge if the balance exceeds £10,000 and the company doesn’t charge proper interest.

Can I just write off my director’s loan account? You can, but it isn’t tax-free. HMRC normally treats a written-off loan as a distribution and taxes it on the director broadly like a dividend, and it can carry Inheritance Tax implications if it happens as part of an estate.

Does Section 455 tax come back eventually? Yes, once you repay the loan — but the company has to wait until nine months and one day after the end of the accounting period in which you made the repayment before it can claim the refund.

What’s the safest balance to keep a director’s loan account at? Zero, or in credit, is the genuinely stress-free answer. If that’s not realistic, keeping any overdrawn balance under £10,000 and clearing it well before the nine-month deadline avoids both the benefit-in-kind charge and Section 455.

If any of this sounds like your own director’s loan account — overdrawn, unclear, or quietly growing since last year’s accounts were filed — it’s worth having someone actually look at the numbers rather than guessing. At Ask Accountants UK Ltd, based at 178 Merton High St, London SW19 1AY, the team handles exactly this kind of thing daily, alongside broader Accounts and Tax, Bookkeeping, Self Assessment, Personal Tax Planning, and HMRC Investigations support. A quick call — 020 8543 1991 — is usually enough to find out whether you’ve got a problem or just a bit of tidying up to do.

(External reference: for the government’s own guidance, see gov.uk on Director’s Loans and the current HMRC official rate of interest for beneficial loans.)