Somewhere between “we gave the sales team gym memberships” and “HMRC wants a form about it,” most business owners lose the plot entirely. That’s the P11D for you. Quietly unglamorous, easy to forget, and expensive to get wrong. Did your company hand out anything beyond straight salary this tax year? A car, private medical cover, a cheap loan to a director having a rough month. If so, there’s a decent chance HMRC expects to hear about it. The P11D is how you tell them.

This guide walks through what a P11D actually is. Which benefits land on it, which don’t, and the dates that matter for 2025/26. It also covers the penalties that creep up on employers who file late. Spoiler: they’re automatic, and HMRC doesn’t send a polite reminder first.

So what actually is a P11D?

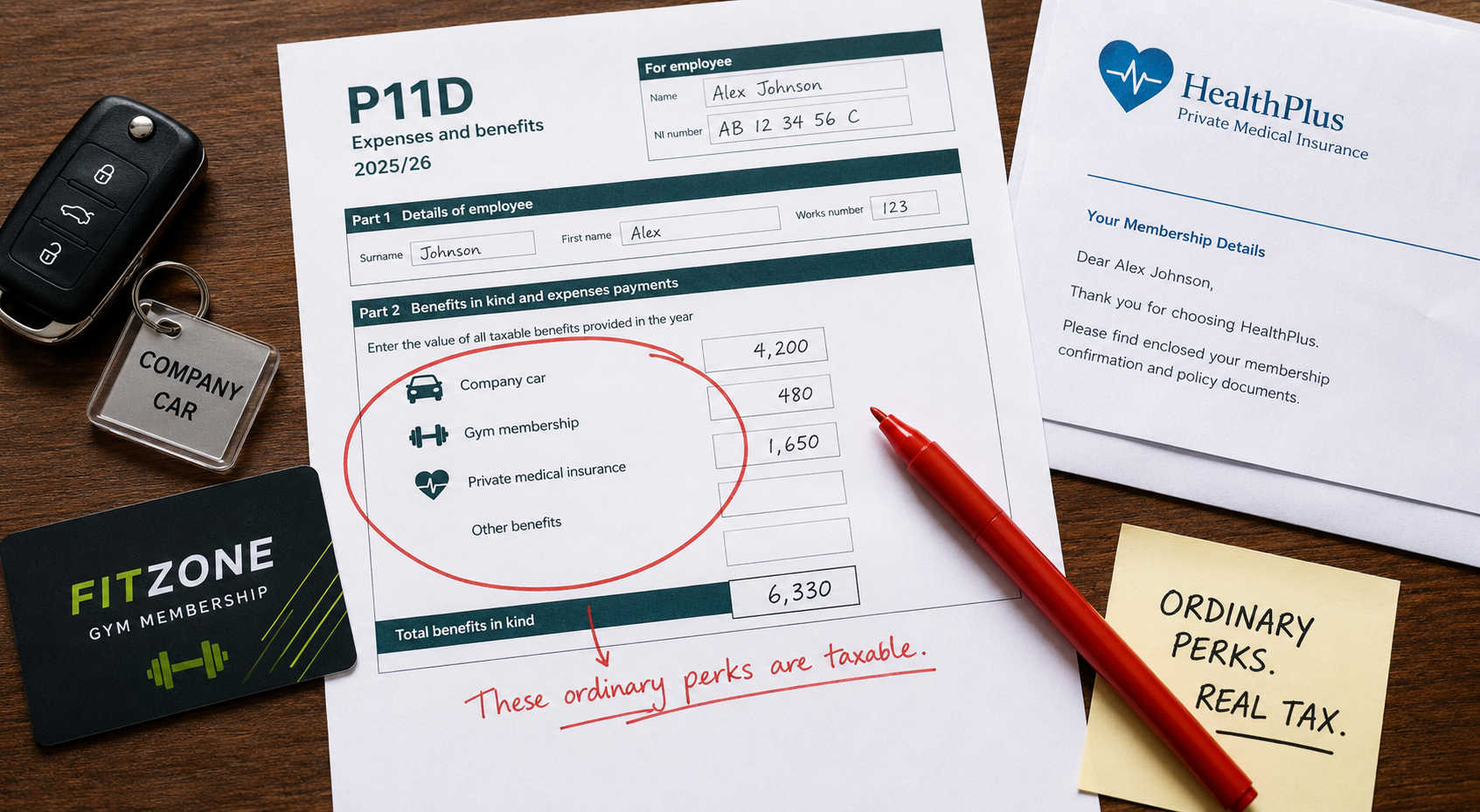

A P11D is the form employers use to report taxable expenses and benefits. Specifically, anything given to employees and directors that wasn’t already taxed through payroll. Think of it as the paperwork trail for everything that isn’t your basic salary — company cars, private health cover, interest-free loans, that sort of thing.

There’s a companion form too: the P11D(b). The P11D reports what each individual employee received. The P11D(b) is the employer’s own summary. It declares the total Class 1A National Insurance owed on all the benefits across the business. People muddle the two constantly. One rule of thumb that helps: P11D = “what did they get,” P11D(b) = “what do we owe.”

You’ll need a separate P11D for every employee or director who received a reportable benefit. No benefits to report at all? You may still need to file a nil P11D(b) if HMRC is expecting one — silence isn’t the same as compliance here.

The benefits that actually need reporting

This is where most of the confusion happens, and most of the missed deductions too. Not every perk counts, and some things people assume are exempt actually aren’t. Here’s the general shape of it:

- Company cars and any fuel provided for private use

- Private medical or dental insurance

- Interest-free or low-interest loans above the reporting threshold

- Living accommodation provided by the employer

- Assets transferred to an employee — laptops, furniture, even the odd company van nobody wanted back

- Non-business travel and entertainment expenses

- Gym memberships, unless run through a genuinely tax-exempt scheme

- Personal bills paid on the employee’s behalf

Reimbursed expenses generally don’t need to go on a P11D, provided they were incurred wholly, exclusively and necessarily for the job. A client dinner. A train fare to a site visit. That’s the line HMRC draws: business necessity versus personal benefit. It’s not always obvious which side something falls on. That grey area is exactly where a lot of businesses end up under-reporting without meaning to.

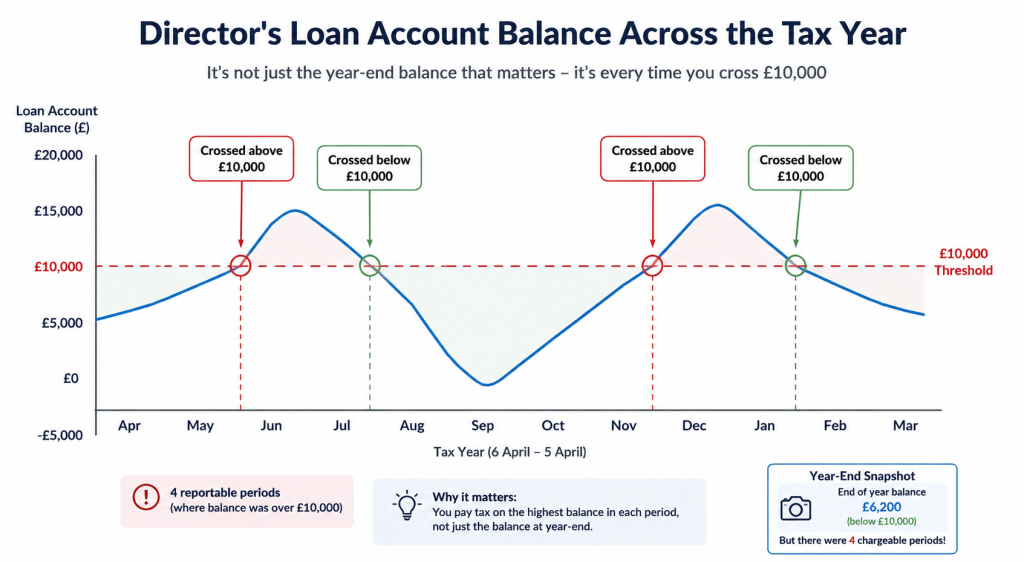

A quick word on director’s loans

Let’s be honest, overdrawn director’s loan accounts happen more often than anyone admits at year-end. If a company lends money to a director, a taxable benefit can arise where no interest is charged. The same applies where the rate charged sits below HMRC’s official rate. For 2025/26, that official rate averages 3.75%. Broadly, if the total outstanding balance across all such loans stays under £10,000 at any point in the year, no benefit arises. Cross that line, even briefly, and it’s worth reviewing properly rather than guessing.

Key P11D deadlines for the 2025/26 tax year

Here’s the bit everyone actually searches for. Mark these in whatever calendar you actually check.

| Deadline | What’s due |

|---|---|

| 6 July 2026 | File P11D and P11D(b) forms with HMRC; give each employee a copy of their own P11D information |

| 19 July 2026 | Class 1A National Insurance must reach HMRC if paying by post |

| 22 July 2026 | Class 1A National Insurance deadline if paying electronically |

Paper P11D forms haven’t been accepted for a while now. Everything goes through HMRC’s PAYE Online service or approved payroll software. The Class 1A NIC rate for 2025/26 sits at 15%, calculated on the total taxable value of the benefits reported.

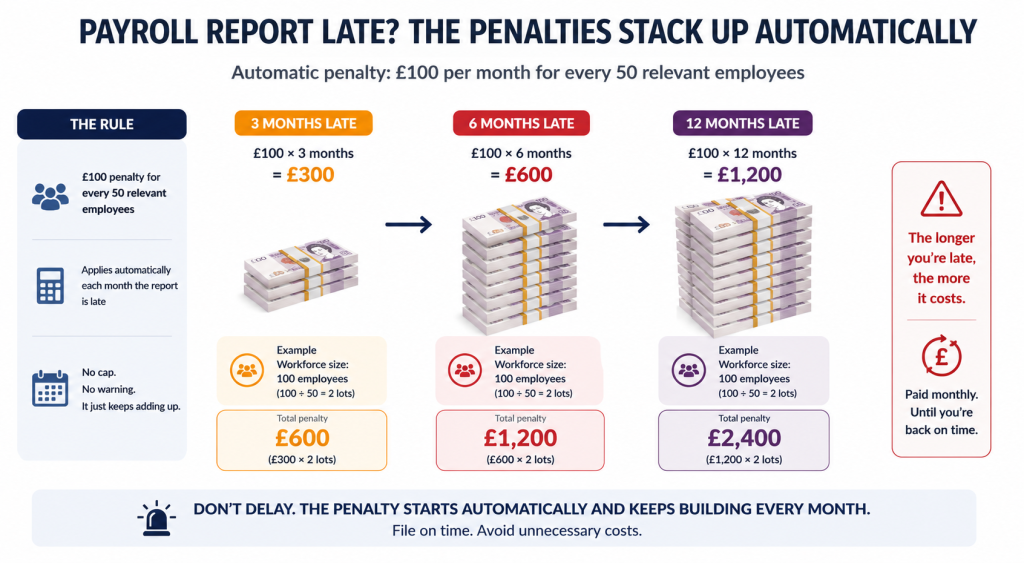

Miss the 6 July deadline and penalties start automatically. They’re set at £100 for every 50 employees, for each month or part-month the P11D(b) is late. Late Class 1A NIC payments pile on interest too, plus escalating penalties. None of this requires HMRC to chase you first. It just happens.

Here’s the same information again, slightly less tidily

(Some benefit categories and their typical treatment — worth double-checking anything unusual against HMRC’s own guidance, as thresholds shift)

| Benefit | Usually reportable? | Notes |

| Company car | Yes | Value based on list price and CO2 emissions |

| Private medical insurance | Yes | Cost to employer, not to employee |

| Business travel | Usually not | If wholly, exclusively and necessarily for work |

| Loans under £10,000 | No | Threshold applies to total balance across all loans |

| Gym membership | Yes | Unless part of an exempt workplace scheme |

Yes, that table’s a bit rough round the edges. A bit like most people’s actual benefits records by the time March rolls around.

What happens if you get it wrong (or late)

I’ll be honest, this is the section people skim past. Then come back to in a panic in August. Late filing penalties on the P11D(b) are automatic. HMRC’s systems flag it — no human judgement involved, no warning email, no grace period. A business with 50 employees that’s three months late is already looking at £300. That’s before interest touches the unpaid Class 1A NIC.

Inaccurate submissions carry their own risk too. Get the benefit values wrong, or miss something HMRC later spots through data matching, and you’re not just correcting a form. You’re potentially opening the door to a wider compliance check. This is one of the areas where HMRC tax investigations often begin: a small discrepancy on a P11D that snowballs into bigger questions about payroll records generally.

The bigger change coming: mandatory payrolling of benefits

Worth knowing, even if it doesn’t affect this year’s filing directly: HMRC is phasing out the annual P11D system. From April 2027, payrolling most benefits in kind becomes compulsory. Motoring benefits and employer-provided medical cover go first, with the rest following from April 2028. Instead of reporting benefits once a year after the fact, income tax on them gets collected through payroll in real time, every pay period.

Loans and employer-provided accommodation are expected to stay outside the mandatory regime for now. So P11D reporting for those specific benefits isn’t disappearing entirely. If you want to get ahead of the curve, voluntary payrolling registration for future tax years opens with HMRC in advance. Worth flagging to whoever runs your payroll services well before the window closes.

One practical knock-on: employees moving onto payrolled benefits will see the tax appear in their monthly pay. Not through a tax code adjustment months later, but straight away. It’s worth telling people this before it shows up as a smaller payslip and triggers an awkward conversation with HR.

Practical steps before the deadline hits

A few things separate the businesses who file calmly from the ones firefighting on 5 July:

- Pull together a complete record of every benefit provided during 2025/26, with values, before you start the forms

- Confirm which benefits, if any, were already payrolled — you don’t file a P11D for those, only the P11D(b) for the NIC

- Double-check director’s loan balances at every point in the year, not just the closing balance

- File and pay through HMRC’s approved online channels — paper forms are rejected outright

- Give employees their copies at the same time you file, not weeks later

If your bookkeeping has been reasonably tidy through the year, this whole exercise takes a fraction of the time. If it hasn’t — well, that’s what July is for, apparently.

Getting help with P11D reporting

None of this is conceptually difficult once you’ve done it a few times. The detail is where people trip up: valuing a benefit correctly, spotting a reportable perk that’s easy to overlook, knowing whether something counts as business necessity or personal advantage. Would you rather hand this over than untangle it yourself in the last week of June? Ask Accountants UK Ltd in Wimbledon handles P11D preparation and filing. The team also covers broader accounts and tax work, tax compliance, and support if HMRC comes asking questions through a tax investigation. You can reach the team on 020 8543 1991, or drop by 178 Merton High St, London SW19 1AY.

For businesses juggling benefits alongside pension duties, it’s also worth glancing at your automatic enrolment obligations while you’re in year-end mode. The two often get reviewed together.

For the official position on any specific benefit, HMRC’s own expenses and benefits A to Z guidance is worth bookmarking. The P11D and P11D(b) filing page is another good one to keep handy.

FAQ

Do I need to file a P11D if I have no benefits to report? If HMRC is expecting a return from your business, yes. You generally need to submit a nil P11D(b) confirming nothing is due, rather than simply doing nothing.

What’s the difference between a P11D and a P11D(b)? The P11D reports individual employee benefits. The P11D(b) is the employer’s summary declaring total Class 1A National Insurance owed across all benefits.

What is the P11D deadline for 2025/26? 6 July 2026 for filing, with Class 1A National Insurance due by 19 July (post) or 22 July (electronic payment).

Are reimbursed business expenses reportable on a P11D? Generally not, provided they were incurred wholly, exclusively and necessarily for business purposes.

What happens after April 2027? Most benefits in kind move to mandatory payrolling. Tax gets collected through payroll in real time rather than reported annually on a P11D, phased in from April 2027 and April 2028.