Here’s a confession from behind the desk. I’ve lost count of how many times a client has phoned in a mild panic because an invoice “looked wrong.” No VAT on it. Some odd sentence at the bottom about HMRC. A nagging feeling they’d been short-changed. Nine times out of ten, they hadn’t been. What they were looking at was reverse charge VAT, doing exactly what it’s meant to do.

What Is Reverse Charge VAT?

Let’s get the topic clear from the off. Reverse charge VAT flips who reports the VAT on a transaction. Instead of the supplier charging VAT and paying it to HMRC, the customer declares that VAT themselves, on their own return. No cash changes hands for the VAT element at all.

It sounds like a technicality. It isn’t. Get the treatment wrong and you can end up paying twice, under-claiming, or fielding an HMRC enquiry you didn’t see coming.

I’ll be honest: when the construction version of this rule landed in March 2021, half the industry hadn’t heard of it until the week before go-live. Some subcontractors thought it was a scam email. It wasn’t. HMRC now actively checks for it, and in 2026 the penalties have real teeth.

Why HMRC Built the Reverse Charge in the First Place

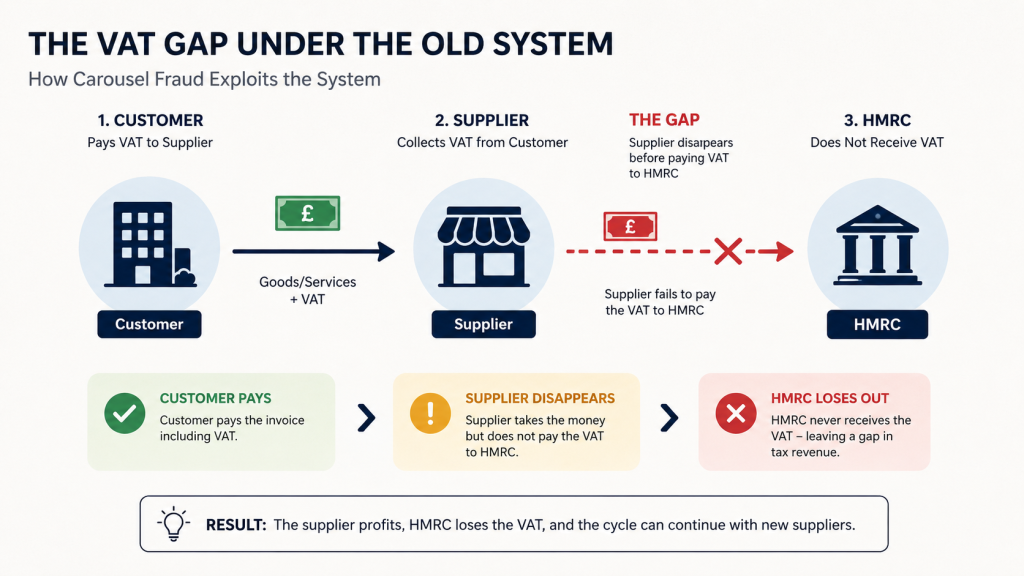

Under ordinary VAT rules, a supplier charges VAT on an invoice, collects the money, and hands it to HMRC on their return. Simple enough, until someone in the chain pockets the VAT and vanishes before paying it across. HMRC calls this “missing trader fraud.” It has cost the Treasury eye-watering sums over the years.

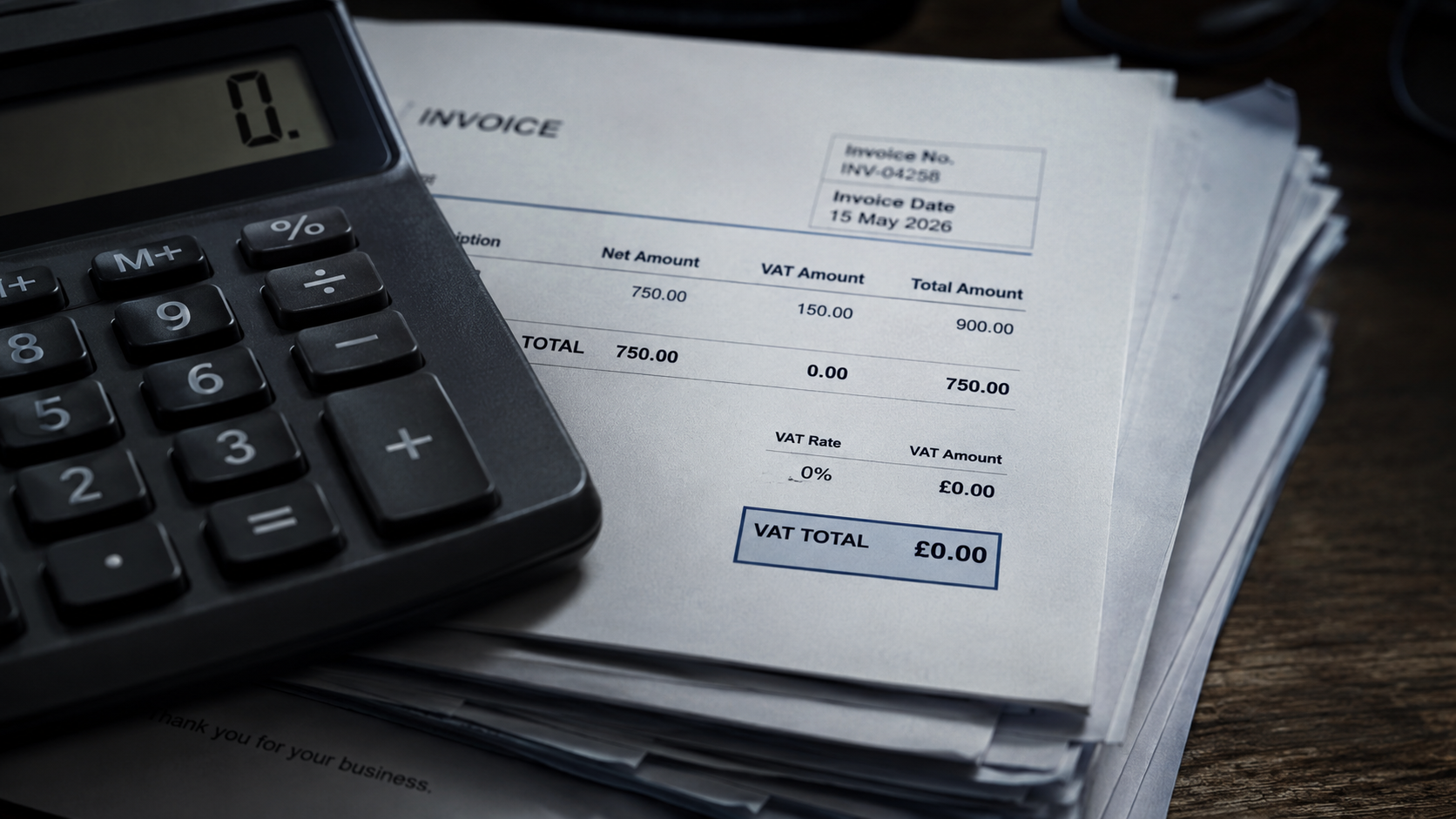

The reverse charge removes that opportunity. The supplier never collects any VAT to lose, hide, or run off with, because the customer accounts for it directly. The supplier still issues an invoice, net of VAT, with wording explaining the reverse charge. The customer declares that VAT as both output tax and input tax on the same return. Assuming they can recover VAT normally, the whole thing nets off to zero. No cash moves. Just paperwork, box numbers, and one specific sentence that has to appear somewhere on the invoice.

That neutrality is exactly why some business owners assume the rule “doesn’t matter.” It matters a great deal if you get the treatment wrong, because HMRC can and does assess for errors even where no actual tax was lost.

Where You’ll Actually Meet Reverse Charge VAT

There isn’t just one flavour here. The reverse charge shows up in a few distinct contexts, and mixing them up is where a lot of confusion starts.

Cross-border services. Say a UK business buys services from a supplier based outside the UK: a software licence from a US company, consultancy from an EU firm. The reverse charge usually applies under the general “place of supply” rules. The UK business self-accounts for the VAT rather than the overseas supplier registering here.

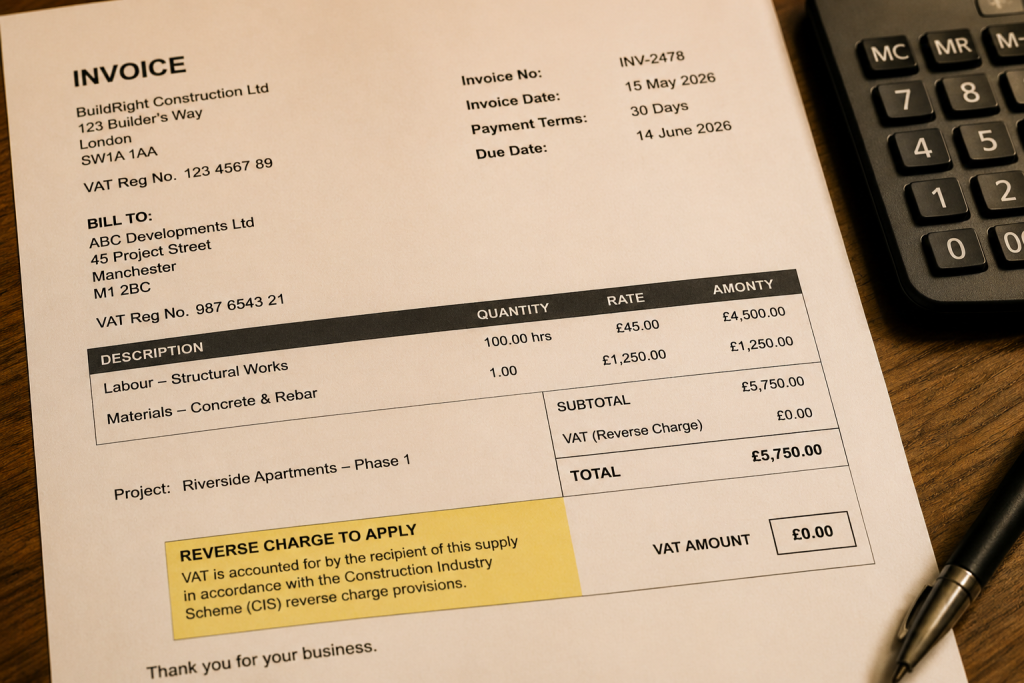

Domestic reverse charge for construction (DRC). This is the one that generates the most phone calls to accountants. Since 1 March 2021, VAT-registered contractors buying certain construction services from VAT-registered subcontractors must apply the reverse charge instead of paying VAT normally. This applies provided the work sits within the Construction Industry Scheme and the customer isn’t an “end user.”

Specific goods categories. Mobile phones, computer chips, emissions allowances and a handful of other goods have carried their own reverse charge rules for years, aimed at the same missing-trader problem.

This article leans heavily on the construction version, because that’s where the mistakes, and the HMRC letters, are currently concentrated.

The Five-Question Test for Domestic Reverse Charge VAT

For the construction sector, DRC only applies when every one of these five conditions holds true. Miss one, and standard VAT rules take over again.

| Condition | What it means in practice |

|---|---|

| Both parties VAT registered | If your customer isn’t VAT registered, charge VAT the normal way. Reverse charge VAT never applies to consumers. |

| Work falls within CIS scope | Construction, alteration, repair, demolition, and most trades on site count. Pure design, surveying, or plant hire alone usually don’t. |

| Standard or reduced VAT rate | Zero-rated work, like most new-build housing, sits outside DRC entirely. |

| Customer isn’t an “end user” | HMRC charges end users, the ultimate owner or occupier of the building, VAT normally. |

| Customer isn’t an “intermediary supplier” | Landlords and connected businesses acting for an end user also sit outside the reverse charge. |

None of these five conditions is optional. Skip the CIS-scope test, for instance, and you’ve applied the reverse charge to a supply that never needed it. That’s its own separate headache to unwind.

Quick warning, not a footnote: get written confirmation from your customer that they’re an end user. Don’t assume it. HMRC has been asking construction firms to produce that paperwork during VAT inspections, and “I just knew they were the end user” doesn’t hold up well in an enquiry.

Getting the Invoice Right

An invoice subject to the reverse charge still needs the VAT rate and amount shown, just not charged. HMRC accepts wording along the lines of:

“Reverse charge: customer to pay the VAT due to HMRC”

or a slightly more formal version referencing the relevant VAT Act section. Either works, but it has to say “reverse charge” somewhere. A blank VAT box with no explanation is exactly the sort of thing that gets flagged.

One genuinely underrated trap: splitting a single job into separate labour and materials invoices to dodge the charge on the materials portion. It doesn’t work. If labour on a contract falls under DRC, materials supplied as part of that same contract usually follow it too, even on a separate invoice line.

The Cashflow Sting Nobody Warns You About

Here’s the bit that catches subcontractors off guard, and it’s got nothing to do with getting the rules “wrong.” It’s simply how the reverse charge changes your bank balance.

Previously, a subcontractor invoicing £10,000 plus £2,000 VAT would receive the full £12,000. They’d sit on that VAT until their quarterly return fell due. Under the reverse charge, that same subcontractor invoices £10,000 only. No VAT lands in the bank account at all.

Profit stays identical. Cash in hand doesn’t. If a chunk of your turnover moved onto the reverse charge and your forecasting hasn’t caught up, you can end up short of working capital while your accounts look perfectly healthy on paper. Flag this to whoever handles your cashflow planning, sooner rather than after an awkward overdraft conversation.

Why 2026 Is a Worse Year Than Usual to Get This Wrong

HMRC’s early approach to reverse charge VAT for construction was, by most accounts, fairly forgiving. Think of it as a settling-in period while businesses adjusted. That period has ended. Enforcement has stepped up markedly. From April 2026, new powers let HMRC cancel a construction firm’s Gross Payment Status, and pursue directors personally, where a business links to fraudulent supply-chain arrangements. Reverse charge VAT compliance now sits squarely inside that scrutiny.

Keep your CIS status checks, end-user confirmations, and VAT-registration evidence filed together for every job. Don’t scatter them across email threads and memory. If HMRC asks how you reached a reverse charge VAT decision on a contract from eighteen months ago, “we were pretty sure at the time” won’t age well as an answer.

Normal VAT vs the Reverse Charge, Side by Side

| Normal VAT | Reverse Charge VAT |

|---|---|

| Supplier charges VAT on invoice | Supplier issues invoice net of VAT |

| Supplier collects VAT from customer | No VAT cash changes hands |

| Supplier pays VAT to HMRC (Box 1) | Customer declares VAT as output tax (Box 1) |

| Customer reclaims VAT separately if entitled (Box 4) | Customer reclaims same amount, same return (Box 4) |

(Yes, that table’s a bit rougher round the edges than the one above. Some habits from spreadsheet life are hard to shake.)

Common Mistakes We See on a Regular Basis

- Charging VAT normally when the reverse charge should have applied, usually because “the customer said they were the end user,” with nothing in writing to prove it

- Forgetting the reverse charge wording on the invoice entirely, leaving a blank VAT line that raises questions

- Treating plant hire with an operator the same as plant hire without one (these aren’t the same for CIS purposes, and that single distinction changes the VAT treatment)

- Applying the reverse charge to zero-rated new-build housing work, where it was never meant to apply

- Never revisiting the very first reverse-charge invoices from 2021. Some errors from that period remain correctable, though the window is closing fast

None of these mistakes are unusual or unfamiliar to anyone who’s worked in construction accounts for a while. They’re the everyday slips that happen when a busy site manager, or a one-person accounts department, juggles six other things and nobody’s explained the reverse charge properly.

If your invoicing software or bookkeeper hasn’t flagged how to treat the reverse charge on your last few construction contracts, raise it before your next VAT return goes in, not after.

Reverse Charge VAT and Your VAT Return, Box by Box

If you’re the customer receiving reverse-charge services: include the VAT due as output tax in Box 1, reclaim the same figure as input tax in Box 4 (subject to normal recovery rules), and record the net purchase value in Box 7. If you’re the supplier: put the net sale in Box 6. Critically, put nothing in Box 1 for that transaction, because you never charged the VAT in the first place.

Muddle the boxes and your own return might still balance, while triggering a mismatch against your customer’s or supplier’s figures elsewhere in HMRC’s system. That’s the kind of discrepancy that quietly sits there until a VAT inspection surfaces it.

When It’s Worth Bringing In Help

You can manage most of this in-house, particularly once your bookkeeping system handles it correctly from the start. But the reverse charge sits at the intersection of two separate rulebooks: general VAT law and the Construction Industry Scheme. That overlap is exactly where mistakes tend to compound rather than cancel out.

This is where firms like Ask Accountants UK Ltd, based at 178 Merton High St, London SW19 1AY, tend to get pulled in, not to replace your bookkeeping, but to sit alongside it. Reviewing VAT accounting and compliance, sorting out CIS claims and refunds, and checking that your reverse charge treatment matches what HMRC expects to see, counts as fairly routine territory for an accounts and tax team that handles construction clients day to day. If you’d rather have someone double-check a handful of contracts than discover an error during an HMRC review, call 020 8543 1991.

Frequently Asked Questions

Does reverse charge VAT apply to sole traders? Yes, if you’re VAT registered and supply or receive services that meet the conditions above. Trading as a sole trader rather than a limited company makes no difference here.

Do I still need to register for VAT if all my income falls under the reverse charge? Reverse-charge sales don’t count towards your VAT registration threshold the same way ordinary sales do. This can help smaller subcontractors who work mostly for larger contractors. Check your specific position rather than assume.

What happens if I charged VAT normally when the reverse charge should have applied? You’ll typically need to issue a credit note for the incorrect invoice and reissue it with the correct wording. Your customer can’t properly recover VAT you shouldn’t have charged, so leaving it unresolved causes problems on both sides.

Is the domestic reverse charge the same as reverse charge VAT generally? Not quite. The construction version (DRC) is one specific application of the broader principle. The same underlying logic, where the customer self-accounts for VAT instead of the supplier charging it, also applies to cross-border services and certain goods.

Does the reverse charge affect my cashflow? For subcontractors, often yes. You stop receiving the VAT-inclusive payment you might have briefly relied on holding before your VAT return fell due. Forecast for that shift; it catches more new-to-DRC businesses than you’d expect.

For the fuller technical picture, HMRC’s own VAT Notice 735 sets out the domestic reverse charge for construction services in detail. The VAT registration and thresholds guidance on GOV.UK is worth a bookmark too, especially if you’re anywhere near the £90,000 threshold.

If this topic touches your invoicing and you’d like a second opinion, our guide on VAT accounting compliance for UK businesses covers the wider compliance picture. Our piece on how VAT accounting works in the UK makes a decent primer if any of the box numbers above felt unfamiliar. Construction businesses might also find our construction accounting guide for UK contractors and our note on CIS compliance mistakes useful reading alongside this one. If HMRC has already contacted you about a VAT or CIS matter, our overview of HMRC tax investigations explains what to expect next.