Auto Enrolment Guidance for Small Employers: What You Must Do

Nobody starts a small business thinking, “I can’t wait to navigate workplace pension legislation.” And yet, here we are. Auto enrolment has quietly become one of the most pressing compliance obligations sitting on the desk of every UK employer — whether you’ve got two members of staff or two hundred.

Miss it, and the Pensions Regulator won’t write a polite letter asking you to pop a cheque in the post. Fines arrive fast. Daily penalties for persistent non-compliance can reach £2,500 per day for larger employers — and even the smallest businesses face £50 a day once enforcement escalates.

This auto enrolment guidance exists because the rules are genuinely confusing. Staging dates, re-enrolment cycles, qualifying earnings bands — most of what you’ll find online is either too vague to act on or too dense to decipher on a Tuesday afternoon between payroll runs. So let’s go through it properly, section by section.

Auto Enrolment Guidance Explained: The Foundation Every Employer Needs

Auto enrolment is the legal requirement for UK employers to automatically enrol eligible workers into a qualifying workplace pension scheme — no action needed from the employee. Introduced in 2012 and rolled out by employer size, every business with at least one eligible worker came under scope by 2018.

The reasoning behind it? Millions of workers were reaching retirement age with little private pension provision. Making enrolment the default — with an opt-out option — shifted behaviour at scale. And it worked. Participation rates climbed dramatically once the opt-in barrier disappeared.

The mechanics of compliance, though? That’s where small employers consistently trip up.

Which Workers Trigger Your Auto Enrolment Duties?

Not everyone on your payroll qualifies for automatic enrolment. Understanding the three worker categories matters — your legal duties differ significantly depending on which group an employee falls into.

| Worker Type | Age Range | Earnings Threshold | Employer Duty |

|---|---|---|---|

| Eligible Jobholder | 22 – State Pension Age | Earns over £10,000/year | Must automatically enrol |

| Non-Eligible Jobholder | 16–21 or State Pension Age–74 | Earns £6,240–£10,000/year, or any age earning above £6,240 | Must enrol them if they request it |

| Entitled Worker | 16–74 | Earns below £6,240/year | Can join a scheme — no employer contributions required |

Thresholds update each tax year — the figures above reflect 2024/25. Review them annually.

Agency workers, zero-hours staff, and casual employees complicate this picture considerably. The job title or contract wording doesn’t determine worker status — the Pensions Regulator looks at the substance of the working relationship. Checking each situation individually avoids expensive assumptions.

Staging Dates: Still Relevant, Even Now

Employers who registered with HMRC after 1 April 2012 had no staging date — auto enrolment duties kicked in from the first day of employment. No grace period. No countdown.

For businesses that predated that cutoff, the staging date was the Pensions Regulator’s starting gun for compliance. That date has long passed for most employers — but two reasons keep it relevant today:

- Re-enrolment cycles run every three years from the original staging date

- Any historic compliance failures will anchor to that date during an investigation

New employers sometimes assume they have a buffer before obligations begin. They don’t. Hire someone in January, fail to set up a qualifying scheme, and by March the regulator has grounds to issue a compliance notice.

Auto Enrolment Contribution Rates: What the Minimum Actually Looks Like

Since April 2019, the statutory minimums have held at:

- Employee: 5% of qualifying earnings (inclusive of tax relief)

- Employer: 3% of qualifying earnings

- Combined total: 8%

Qualifying earnings run between £6,240 and £50,270 per year for 2024/25. For a worker earning £25,000, contributions calculate on £18,760 — not the gross salary. Some schemes base contributions on total pay from pound one, which simplifies the maths — just confirm the minimum qualifying earnings test still passes.

| Contribution Type | Minimum % | Basis | Key Point |

|---|---|---|---|

| Employer | 3% | Qualifying earnings | Cannot offset against employee contributions |

| Employee | 5% | Qualifying earnings | Includes basic rate tax relief at source |

| Total minimum | 8% | Qualifying earnings | Both contributions due each pay period |

Picking a Qualifying Pension Scheme

The scheme you select must meet the Pensions Regulator’s standards. For most small employers, the practical options are:

- NEST (National Employment Savings Trust) — the government-backed default, obligated to accept every employer regardless of size

- The People’s Pension — straightforward setup, popular with micro-businesses

- Smart Pension, NOW: Pensions — both qualify and integrate well with common payroll software

Scheme fees vary, and at smaller contribution levels the differences matter. Before committing to whatever your payroll provider suggests by default, spend time comparing costs against your employee headcount and average contribution size.

💡 One thing worth checking: Your chosen scheme must integrate with your payroll software. Manual contribution uploads each pay period are error-prone and time-consuming — the kind of administrative drag that causes missed payment deadlines and compliance gaps.

The Opt-Out Rules: A Line Employers Cannot Cross

Workers have the right to opt out within one calendar month of enrolment. If they do so within that window, any contributions already deducted must be refunded in full.

What employers absolutely cannot do: suggest, hint at, or encourage opting out. Even informally. Even as an offhand remark during a salary negotiation. The Pensions Regulator treats inducement to opt out as a serious offence — fines and criminal proceedings apply in the most clear-cut cases.

Specifically, employers must never:

- Offer a pay rise conditional on opting out

- Raise the subject of opting out during recruitment

- Hand over the opt-out form without the employee requesting it

The opt-out process belongs to the worker and runs through the pension scheme’s own system. Your role ends at enrolment.

Re-enrolment: The Three-Year Obligation Most Small Employers Forget

Every three years from your staging date (or duties start date for newer employers), re-enrolment kicks in. Any workers who previously opted out or stopped active membership must be re-enrolled automatically.

Re-enrolment doesn’t run itself. Here’s what the process involves:

- Identify your re-enrolment date — you have a six-month window around the third anniversary

- Re-assess your entire workforce against the eligibility criteria

- Re-enrol all eligible workers who aren’t currently active pension members

- Submit a re-declaration of compliance to the Pensions Regulator within five months of your re-enrolment date

Missing the re-declaration is one of the most common compliance failures among small employers. Not because anything went wrong with the pension contributions — purely because the paperwork deadline slipped off the radar.

For ongoing support with auto enrolment guidance compliance, including re-enrolment cycles and re-declaration filing, the team at Ask Accountant manages these obligations as part of their payroll management service.

What the Pensions Regulator Does When You Don’t Comply

Enforcement follows a clear escalating path. Understanding it helps explain why ignoring early correspondence is such a bad idea.

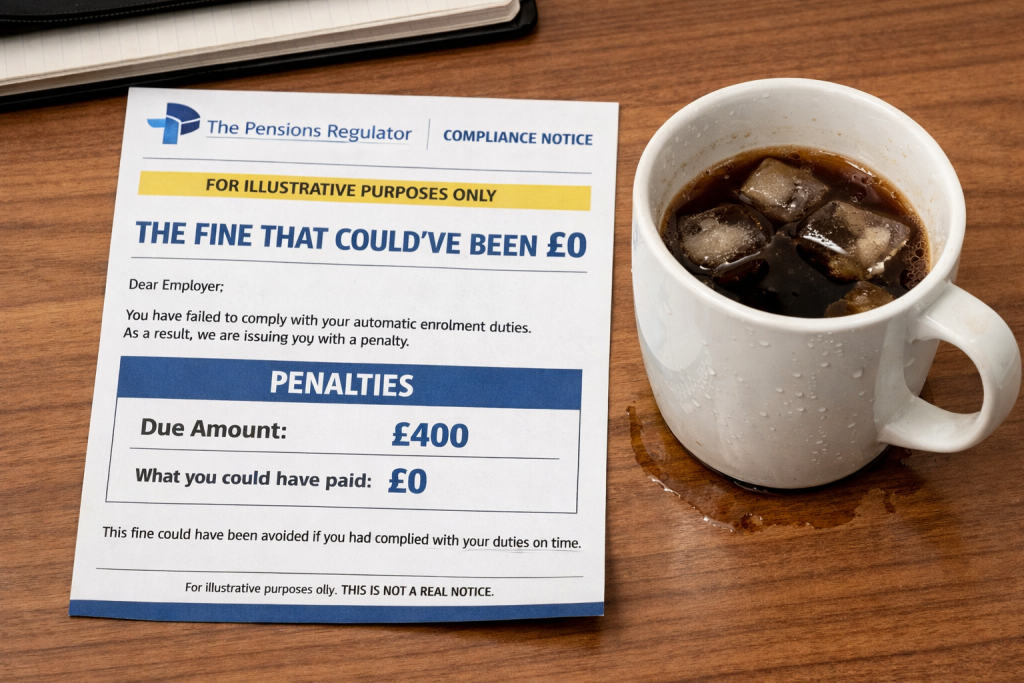

Stage 1 — Compliance notice: You receive a deadline to comply. This is your chance to sort things out before financial consequences arrive.

Stage 2 — Fixed penalty notice: A flat £400 fine, regardless of business size.

Stage 3 — Escalating penalty notice: Daily fines kick in based on employee numbers. For 1–4 employees, that’s £50/day. For 5–49, it rises to £500/day. At 50–249 employees, daily fines reach £2,500.

Stage 4 — Civil or criminal proceedings: Reserved for persistent or deliberately evasive non-compliance.

Reading through the Pensions Regulator’s published enforcement cases, the pattern repeats almost identically: an employer convinced the rules didn’t apply to them, a compliance notice that went unanswered, and a penalty that dwarfed the cost of just setting up the scheme in the first place.

If you’ve already fallen behind, acting now — before a compliance notice arrives — puts you in a far stronger position when dealing with the regulator.

Record-Keeping: The Part Nobody Finds Interesting Until They’re Investigated

Records relating to auto enrolment must be kept for a minimum of six years. The Pensions Regulator can request these at any point, and failure to produce them carries its own separate penalty.

Your records need to cover:

- Names and dates of birth for all enrolled workers

- Enrolment dates and any opt-out notices received

- Contribution amounts and the dates each payment was made

- Copies of all written communications sent to workers about enrolment

- Your declaration of compliance reference number

Cloud-based payroll systems make this considerably less painful. If payroll still runs through spreadsheets or paper files, the administrative risk of an audit is much higher than it needs to be. The bookkeeping and accounting services at Ask Accountant integrate payroll record-keeping directly — so auto enrolment documentation doesn’t become a separate manual exercise.

Every New Hire Triggers Fresh Auto Enrolment Duties

Auto enrolment guidance for small employers often focuses on the initial setup — the staging date, the scheme selection, the declaration. But the obligations recur with every new employee. Each eligible hire requires enrolment within six weeks of their start date (known as the “joining window”).

Workers aged 22 or over, below State Pension Age, and earning more than £10,000 a year must be enrolled. No exceptions for probationary periods — although employers can apply a postponement of up to three months, provided written notice reaches the employee within six weeks of their start date.

Part-time workers below the £833/month threshold retain the right to opt into the scheme. Those earning between £520 and £833 per month who ask to join entitle themselves to employer contributions as well.

Small Businesses Carry the Same Weight as Large Ones Here

A persistent belief among micro-employers is that auto enrolment somehow applies less rigorously to very small businesses. It doesn’t. The statutory duties land equally on a sole director with one member of staff and a regional employer with forty.

The Pensions Regulator has made its enforcement priorities plain since mass staging completed. Smaller employers who never properly established their schemes now feature prominently in compliance campaigns.

Small business owners navigating this for the first time — or realising compliance has slipped — can get straightforward auto enrolment guidance from Ask Accountant, based at 178 Merton High St, London SW19 1AY. Call +44(0)20 8543 1991 or visit the site to explore small business accounting services that cover payroll, bookkeeping, and pension compliance together — rather than treating each as a separate problem.

Frequently Asked Questions: Auto Enrolment Guidance for UK Employers

Q: Do part-time staff need to be enrolled? Any worker aged 22 or over, below State Pension Age, and earning above £833 per month (£10,000/year) must be automatically enrolled. Hours worked don’t affect the calculation — earnings do.

Q: An employee already has a personal pension. Does that change anything? No. Eligibility for auto enrolment doesn’t disappear because someone has existing arrangements. Enrol them into the workplace scheme; they can opt out afterwards if they prefer their own provision.

Q: Is salary sacrifice allowed under auto enrolment? Yes — many employers use salary sacrifice because it reduces National Insurance contributions for both parties. The scheme must still pass the minimum contribution test, and the arrangement must not take any worker’s pay below the National Minimum Wage.

Q: What’s the postponement period and how does it work? Employers can delay auto enrolment for up to three months for a new hire. A written notice must reach the worker within six weeks of their start date explaining the postponement — miss that communication and the postponement becomes invalid.

Q: Do company directors have to be enrolled? A sole director with no other staff is generally outside the scope of auto enrolment. Once two or more directors hold contracts of employment, the standard employer duties apply. Getting business advice tailored to your company structure is worth the hour.

Q: How does declaring compliance work? Declarations go through the Pensions Regulator’s online portal. You’ll need your staging or duties start date, PAYE reference, and pension scheme details. The declaration must reach the regulator within five months of your staging date or re-enrolment date.

Q: Can I run a scheme where only employees contribute? No. The 3% employer contribution is a statutory minimum. Any scheme that removes employer contributions entirely fails the qualifying test.

⚠️ Worth flagging: Auto enrolment sits at the intersection of payroll, employment law, and tax compliance simultaneously. Sorting the pension correctly while inadvertently underpaying National Minimum Wage or misclassifying a worker’s status creates overlapping problems that compound each other. These areas genuinely need reviewing together.

Further Reading and Resources

From Ask Accountant:

- The Ultimate Guide to Auto Enrolment: Workplace Pensions in 2025

- Auto Enrolment Smart Pension Compliance Guide for UK Employers

- Payroll Management Including CIS Returns

- Business Advice for Growing Employers

- Best Small Business Accounting Services UK

External sources: