There’s a particular dread that descends when someone hands you the IHT400 guidance notes for the first time. You’re grieving. You’re exhausted. And now HMRC wants a 16-page inheritance tax return, plus potentially a dozen supplementary schedules, all within a strict deadline. Welcome to being an executor.

The IHT400 is the main form executors use to report a deceased person’s estate to HMRC. You need it when inheritance tax is due — or when probate requires a full account of the estate. Most executors have never seen IHT400 guidance before. That’s exactly why this guide exists.

What the IHT400 Is and When You Need It

Not every death triggers an IHT400. Simple estates — clearly below the inheritance tax threshold of £325,000, or up to £1 million with the residence nil rate band and spousal transfers — may use the shorter online IHT estate report instead (for deaths from 1 January 2022).

You need the IHT400 when:

- The estate value exceeds the available threshold

- Inheritance tax is actually payable

- The deceased made gifts in the seven years before death that exceed annual allowances

- You’re claiming a transferable nil rate band from a deceased spouse or civil partner

- There are trusts, foreign assets, or business/agricultural property relief claims

- HMRC specifically requests the full account

“Straightforward” estates turn out to be rarer than most people expect. Joint assets, pension death benefits, gifts to grandchildren, a buy-to-let property — each of these can drag you into IHT400 territory even when the estate looks modest at first glance.

IHT400 Guidance: Understanding the Form’s Structure

The IHT400 runs to 16 pages. But the form is really just the skeleton. The real complexity comes from the supplementary schedules — the IHT4XX forms — which attach depending on what the estate holds.

Pages 1–3 cover basic details: who died, who the executors are, domicile status. The estate summary lives on pages 4–6 — totals for all assets and liabilities. Moving further in, gifts, trusts, and other transfers made before death occupy pages 7–9. Exemptions and reliefs — spouse exemption, charity relief, business property relief — all appear on pages 10–12. The actual tax calculation sits on pages 13–14, followed by the declaration and payment details rounding things off on pages 15–16.

What trips most executors up isn’t any single section. It’s the connections between them. Values entered on a supplementary schedule feed into the summary totals, which then shape the tax calculation. One wrong figure creates a ripple effect across the whole return.

The Supplementary Schedules: Your IHT400 Roadmap

This is where solid IHT400 guidance becomes most valuable. The supplementary schedules aren’t optional extras. They’re mandatory when the relevant assets or circumstances apply. Missing one — or using the wrong one — causes delays and HMRC correspondence that nobody wants.

| Schedule | What It Covers | When Required |

|---|---|---|

| IHT401 | Domicile outside the UK | Deceased was domiciled abroad |

| IHT402 | Transferable nil rate band claim | Surviving spouse/civil partner claiming unused NRB |

| IHT403 | Gifts and other transfers of value | Gifts made in the 7 years before death |

| IHT404 | Jointly owned assets | Any assets held in joint names |

| IHT405 | Houses, land, buildings | Deceased owned property |

| IHT406 | Bank and building society accounts | All bank accounts, savings, ISAs |

| IHT407 | Household and personal goods | Contents, jewellery, vehicles |

| IHT409 | Pensions | Any pension arrangements |

| IHT410 | Life assurance and annuities | Life policies not written in trust |

| IHT411 | Listed stocks and shares | Quoted shares, unit trusts, OEICs |

| IHT412 | Unlisted stocks and shares | Shares in private companies |

| IHT413 | Business and partnership interests | Business property relief claims |

| IHT418 | Assets held in trust | Deceased had a life interest in a trust |

| IHT421 | Probate summary | Always required — sent to Probate Registry |

Don’t overlook IHT421. Executors often treat it as a footnote. But the Probate Registry uses it to issue the grant. Errors here stall probate. Double-check that the figures match your IHT400 totals exactly — every single time.

Valuing the Estate: Where IHT400 Errors Begin

HMRC expects the date of death value — not what things might sell for later. Property markets shift. That doesn’t matter. Your IHT400 inheritance tax return must reflect the value on the day the person died.

For property, get a formal RICS valuation or a written letter from a qualified estate agent confirming the date-of-death open market value. Bank statements are simpler — contact each institution and request the balance on the date of death.

Stocks, Shares, and the Quarter-Up Rule

Stocks and shares follow the “quarter-up” rule. Take the lower of the two prices quoted in the Stock Exchange Daily Official List for that date. Add a quarter of the difference between those two prices. Use that figure. HMRC cross-references these figures, so precision matters.

Personal Effects: The Most Undervalued Asset

Personal effects cause frequent IHT400 problems. Executors often write down a nominal sum without considering jewellery, artwork, antiques, or collectibles. HMRC can and does open enquiries where it suspects undervaluation. Anything potentially significant deserves a proper appraisal.

Seven-Year Gifts on Your IHT400 Return: More Layers Than You’d Think

Most people know the seven-year rule in outline — gifts made more than seven years before death are generally exempt. But the detail has more texture than that.

Taper Relief: Often Claimed, Rarely Applies

Gifts made three to seven years before death may qualify for taper relief. This reduces the IHT rate on the gift. But taper relief only applies to gifts that exceed the nil rate band after applying the seven-year running total. Many executors claim it when it makes no difference — because the gift sits within the available nil rate band anyway.

Gifts With Reservation of Benefit

Gifts with reservation of benefit catch a lot of estates out. The classic example: someone gifts their house to their children but continues living in it rent-free. That gift stays in the estate. It returns to the IHT400 as “property subject to a reservation of benefit” — as if the deceased still owned it outright.

The IHT403 schedule requires a full list of every gift above the annual exemption (£3,000 per year) going back seven years. This means detective work. Bank statements, family conversations, financial records from years earlier. Not enjoyable. Absolutely necessary.

⚠️ Easy to miss on the IHT400: Regular gifts from surplus income are exempt from inheritance tax — but only if they genuinely came from income (not capital) and didn’t reduce the donor’s standard of living. You must demonstrate this on IHT403. This is one of the most under-claimed exemptions in UK inheritance tax. Always investigate it properly.

Business and Agricultural Reliefs: High Value, High Scrutiny

Business Property Relief (BPR) and Agricultural Property Relief (APR) can slash an estate’s taxable value — sometimes to zero. But the qualifying conditions are strict. The executor carries the burden of proof.

BPR at 100% applies to:

- A business or interest in a business (sole trader or partnership share)

- Unquoted shares, including AIM-listed shares

- Shares giving control of a quoted company

BPR at 50% applies to:

- Quoted shares where the deceased held control

- Land, buildings, or machinery the deceased used in their business

The two-year ownership rule applies. And businesses that primarily hold investments — such as a company that mainly collects rent — may not qualify. HMRC scrutinises BPR claims on the IHT400 carefully and consistently.

Charitable Donations and the 36% Rate

Charitable donations through the will are fully exempt. And here’s something many executors miss entirely: if 10% or more of the net estate passes to charity, the IHT rate on the taxable portion drops from 40% to 36%. This rule has existed since 2012. It still catches people by surprise every year.

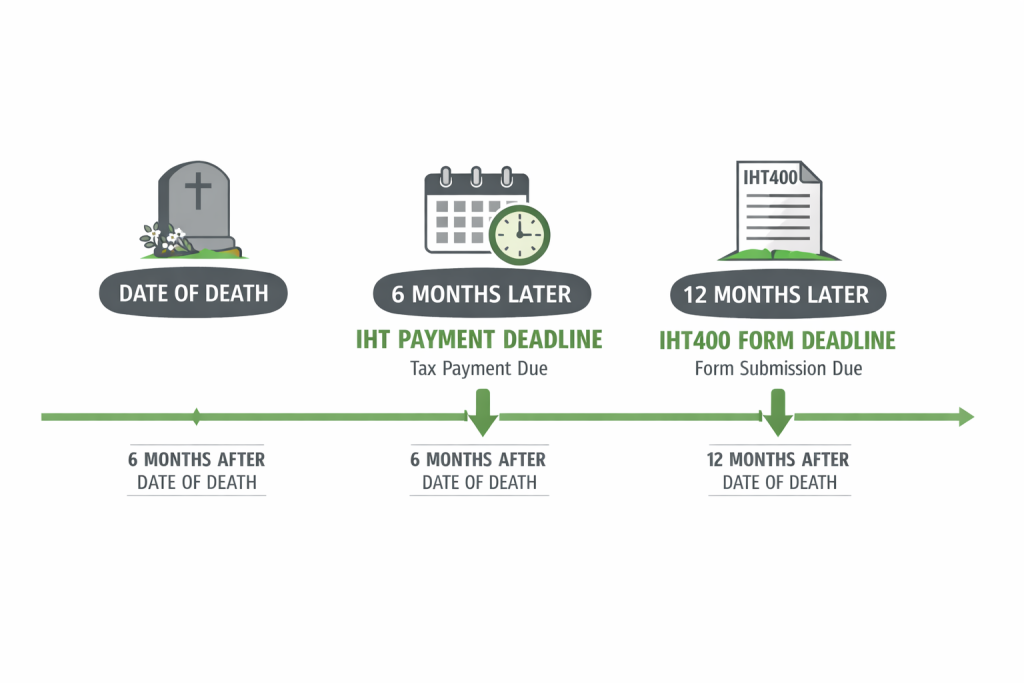

IHT400 Deadlines: The Part That Trips Executors Up Most

The IHT400 guidance from HMRC is clear on one point: submit within 12 months of the end of the month in which death occurred. Death on 15 March 2024 means the IHT400 is due by 31 March 2025.

But here’s the trap. Inheritance tax itself is due within six months of the end of the month of death. In the same example, IHT must arrive at HMRC by 30 September 2024. That’s six months before the form is even due. Late payment brings interest — currently at HMRC’s standard rate, which has stayed uncomfortably elevated.

| Stage | Deadline | Notes |

|---|---|---|

| IHT Payment Due | 6 months after end of month of death | Interest accrues after this date |

| IHT400 Submission | 12 months after end of month of death | Penalties apply for late filing |

| Instalment election | Must elect at time of first payment | Cannot elect retrospectively |

| HMRC processing time | Typically 20 weeks or more | Complex estates take longer |

| Corrective accounts | As needed post-submission | If valuations or assets change |

Paying IHT by Instalments

Some assets qualify for instalment payments spread over ten years — property, controlling shareholdings, and certain business assets. Electing instalments can protect estate liquidity while probate runs. But interest still accrues on the outstanding balance.

The Direct Payment Scheme (Often Overlooked)

Banks and building societies release funds to pay IHT before probate — but only to pay the tax itself, via the direct payment scheme. You need a payment reference from HMRC first (form IHT422). Most major UK banks participate. Few executors know it exists at the outset.

After You Submit the IHT400: What Happens Next

HMRC processes IHT400 inheritance tax returns at their Nottingham office. Processing times have stretched significantly. In 2025, twenty weeks is typical. Complex estates run longer.

During processing, HMRC may accept the figures and issue a clearance certificate (IHT30). Or they raise queries on specific valuations. Formal compliance checks are less common but not unusual for larger estates.

Executors should hold back a portion of the estate after distribution. This protects against late HMRC queries — particularly where lifetime gifts were made that could face challenge.

If the property eventually sells for less than the probate value, submit a corrective account and reclaim the overpaid IHT. This happens frequently in a softening property market.

Common IHT400 Mistakes That Come Back to Haunt Executors

Certain patterns appear again and again in problematic IHT400 submissions.

Forgetting the deceased’s outstanding income tax. The estate must settle any income tax or capital gains tax from the final tax year — and any earlier years with outstanding returns. This is a liability that reduces estate value. But only if executors actually include it on the IHT400.

Treating pension death benefits as estate assets. Most modern pensions fall outside the estate. Do not include them on the IHT400. Annuities and older arrangements behave differently — the IHT409 schedule helps clarify the position for each arrangement.

Claiming exemptions without documentation. Stating that a gift came from “regular income” isn’t enough. HMRC expects evidence: bank statements, income records, a consistent pattern of giving. Without this, the exemption claim will face a query.

Underestimating the time the IHT400 takes. Complex estates take weeks to compile. Hunting down valuations, contacting financial institutions, locating gift records from years earlier — none of this moves quickly.

Getting Professional IHT400 Help: When DIY Stops Making Sense

Some executors handle the IHT400 themselves. For simpler estates, that’s entirely reasonable. For anything involving business assets, trusts, foreign property, significant lifetime gifts, or BPR/APR claims — professional support isn’t a luxury. It’s risk management.

The team at Ask Accountant handles inheritance tax matters alongside broader tax advisory work. They’re well-placed to support executors navigating complex IHT400 inheritance tax returns. Find them at 178 Merton High St, London SW19 1AY, or call +44(0)20 8543 1991.

Having someone who understands HMRC’s expectations when completing an IHT400 can make a real difference — to the outcome and to your stress levels.

FAQs on IHT400 Guidance

Do I always need to submit an IHT400 for probate? No. For smaller, simpler estates below the IHT threshold with no complicating factors, the online IHT estate report may suffice (for deaths from 1 January 2022 onwards). If inheritance tax is payable — or if the estate involves trusts, foreign assets, or significant lifetime gifts — the IHT400 is required.

Can I submit the IHT400 online? Currently, the IHT400 must go by post to HMRC’s Inheritance Tax office in Nottingham. No fully online submission route exists for the main form yet, though HMRC continues moving processes online. Check HMRC’s current guidance for the latest position.

What happens if I make a mistake on the IHT400? Submit a corrective account. If the error led to underpayment of tax, interest accrues on the shortfall. HMRC takes a serious view of deliberate undervaluation. Discover a genuine error? Correct it promptly. Don’t hope it goes unnoticed.

How long does HMRC take to process an IHT400? Currently around 20 weeks for straightforward submissions. Complex estates or those generating HMRC queries take considerably longer. Check HMRC’s processing times page for current figures.

What is the IHT421 and why does it matter? The IHT421 is the probate summary that accompanies the IHT400. The Probate Registry uses it to issue the grant. Figures must match the IHT400 exactly. HMRC forwards it to the Probate Registry after processing — or in some cases, the executor sends it directly.

Can the estate pay IHT before probate? Yes — via the direct payment scheme. Banks transfer funds from the deceased’s accounts directly to HMRC before probate. Request a payment reference from HMRC first using form IHT422. Most major UK banks participate in this scheme.

Where do I find official IHT400 guidance from HMRC? HMRC publishes detailed IHT400 guidance notes for the main form and each supplementary schedule. Work through the notes alongside the form itself, section by section. Reading them cover to cover in isolation rarely helps.

The IHT400 rarely feels straightforward — even with good guidance. But a methodical approach works. Take each supplementary schedule in turn. Gather valuations carefully. Understand which reliefs genuinely apply. And if you’re uncertain whether you’ve got it right, professional review almost always costs less than an HMRC enquiry.