If you work in construction as a subcontractor, there’s a decent chance HMRC is sitting on money that belongs to you. Not because of any error on your part — it’s just how the Construction Industry Scheme (CIS) works. Contractors deduct tax from your payments before you even see them, at either 20% or 30%, and in many cases that deduction is more than your actual tax liability. The difference? That’s your CIS refund. And it can be substantial.

I’ve spoken to plasterers, electricians, and groundworkers who genuinely had no idea they were entitled to thousands back. One roofer I know had four years of unclaimed refunds sitting with HMRC — money he’d essentially lent to the government, interest-free, without realising it.

So. Let’s fix that.

What the CIS Scheme Actually Does (and Why It Creates Refunds)

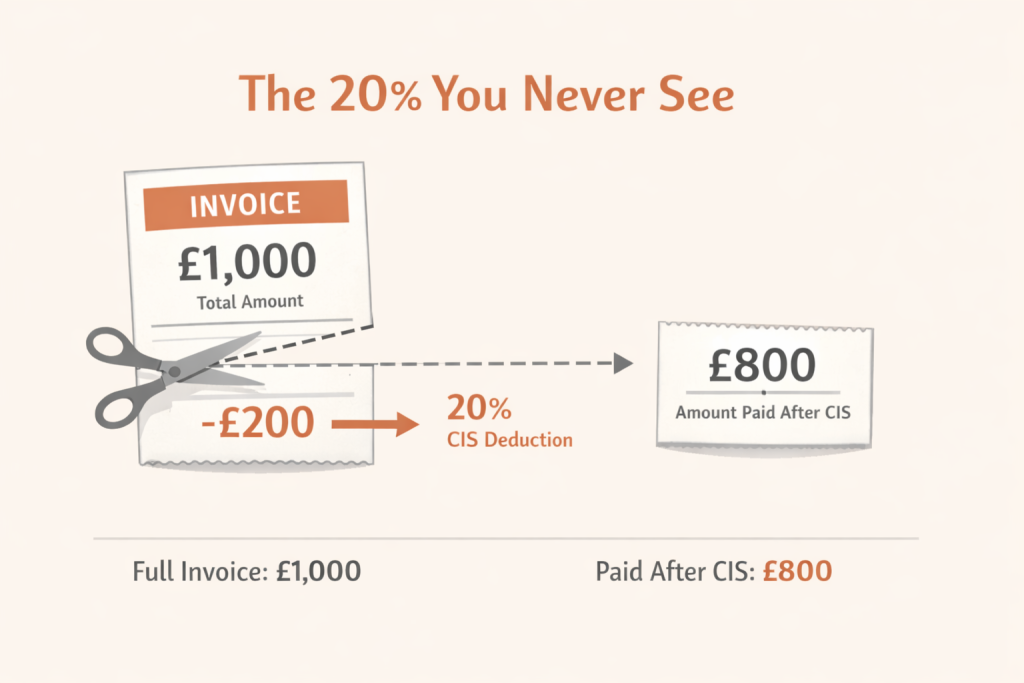

The Construction Industry Scheme was set up by HMRC to ensure tax compliance in an industry historically prone to cash-in-hand arrangements. In practice, it means that when a contractor pays a registered subcontractor, they’re required to deduct either 20% (if you’re verified with HMRC) or 30% (if you’re not registered or can’t be verified) from the labour portion of your payments.

This deduction goes to HMRC as a sort of advance payment against your tax bill.

Here’s where the mismatch happens: the 20% or 30% deducted isn’t calibrated to your actual tax position. Your real tax liability depends on your total income, your allowable expenses, your personal allowance, National Insurance contributions — a whole constellation of factors that CIS deductions don’t account for. So if your deductions collectively exceed what you genuinely owe, you’re entitled to a CIS tax refund.

For sole traders and partnerships, this comes back via Self Assessment. For limited companies, it’s offset against Corporation Tax.

Who Can Actually Claim?

This bit matters, because there’s sometimes confusion.

You can claim a CIS refund if you are:

- A sole trader subcontractor registered under CIS

- A partner in a partnership working in construction

- A director of a limited company that receives CIS-deducted payments

What you cannot do is claim back deductions that were correctly applied if your tax bill equals or exceeds the amount deducted. The refund only arises when deductions outstrip liability — which, honestly, happens quite often for subcontractors with significant business expenses or those who didn’t work the full tax year.

One important distinction: if you’re operating through a limited company, you don’t claim the refund personally. Your company offsets the CIS deductions against its PAYE liabilities or Corporation Tax, and if there’s still a surplus, it requests repayment from HMRC. The process is different — and messing this up is a common mistake. The team at Ask Accountant handles both routes regularly, which matters when you’re trying to avoid accidentally filing in the wrong category.

The Documents You’ll Need Before You Start

Don’t skip this section — nothing derails a CIS refund claim faster than missing paperwork.

Here’s what you’ll want to gather:

- CIS payment and deduction statements — your contractor is legally obliged to provide these monthly. They show the gross payment, the cost of materials (which isn’t subject to deduction), and the tax deducted. If your contractor hasn’t given you these, chase them. You’re entitled to them.

- Details of all your business expenses — tools, vehicle costs, protective equipment, phone bills used for work, insurance. Everything you’ve spent wholly and exclusively for your construction work can reduce your taxable income, which directly increases your refund.

- Your UTR number (Unique Taxpayer Reference) — you’ll need this to file Self Assessment and for HMRC to link the deductions to your record.

- Bank statements and invoices — to corroborate your income and expenditure figures.

- Your HMRC online account login — or access through your accountant’s agent credentials.

How the Claim Process Actually Works

For sole traders, the CIS refund comes through your annual Self Assessment tax return. You declare your gross construction income, deduct your allowable business expenses, arrive at your taxable profit, calculate the tax owed — and then subtract the CIS deductions already paid. If those deductions exceed your liability, HMRC issues a refund.

The timeline? Once your Self Assessment return is submitted, HMRC aims to process refunds within 2–6 weeks, though it can take longer during busy periods (January and February tend to be nightmarish). You can also call HMRC to chase if it’s been a while.

For limited companies, it’s done through the company’s CIS return and monthly PAYE submissions. The company can offset CIS deductions suffered against PAYE it owes as an employer. If the CIS deductions exceed the PAYE liability, the company can request repayment directly. This is filed through the Employer Payment Summary (EPS) rather than Self Assessment — a completely different mechanism.

Worth knowing: You can claim back CIS refunds for up to four tax years — not just the current one. So if you’ve been registered as a subcontractor for several years and never filed properly, there could be multiple years of overpayments to recover. The window closes after four years from the end of the relevant tax year, so older claims get lost forever.

What HMRC Will and Won’t Accept as Expenses

This is where the difference between a modest refund and a genuinely worthwhile one often lives.

Allowable expenses for CIS subcontractors typically include:

- Cost of materials (if you supply them)

- Tools and equipment (outright purchases or hire)

- Work clothing and PPE

- Vehicle expenses — mileage at HMRC’s approved rates, or actual costs if you keep records

- Public liability insurance and professional indemnity cover

- Accountancy and bookkeeping fees (yes, really — including what you pay for help with the refund claim itself)

- Mobile phone — the proportion used for work

- Training directly related to your trade

What HMRC doesn’t like:

- Ordinary commuting (site-to-home travel, unless your home is your base of operations)

- Personal clothing, even if you only wear it for work

- Fines and penalties

- Client entertainment

The expenses question is genuinely worth getting right. Underclaming costs you money; overclaiming risks HMRC scrutiny. If you’re unsure where the line is, proper tax advisory guidance can pay for itself several times over.

CIS Deduction Rates at a Glance

| Subcontractor Status | Deduction Rate | When It Applies | Refund Likelihood |

|---|---|---|---|

| Registered (verified) | 20% | Standard registered subcontractors | Moderate to high |

| Unregistered / unverified | 30% | Not registered or HMRC can’t verify | Very high |

| Gross payment status | 0% | HMRC-approved, larger businesses | N/A — no deductions made |

Gross Payment Status — Is It Worth Pursuing?

While we’re on the topic: if you’re tired of having deductions taken at source and then waiting months to reclaim them, gross payment status might be something to consider. It means contractors pay you in full with no CIS deductions at all — you simply manage your own tax through Self Assessment.

To qualify, you need to meet HMRC’s business, turnover, and compliance tests. The turnover threshold is £30,000 for sole traders (or £30,000 per partner in a partnership, up to £200,000 total). Your tax affairs have to be squeaky clean — no late filings, no unpaid tax. It’s not available to everyone, but for established subcontractors, it eliminates the refund chase entirely.

Common Reasons CIS Refund Claims Go Wrong

In no particular order, here are the mistakes that cause delays, rejections, or underpayments:

Missing deduction statements. If you haven’t collected monthly statements from every contractor you’ve worked for, your figures will be incomplete. HMRC cross-references what you claim against what contractors have reported — gaps attract questions.

Miscategorising materials. CIS deductions only apply to the labour element of payments — not materials. If a contractor has been deducting 20% from the full invoice including materials, you’ve been overtaxed. The deduction statements should show the split. If they don’t, you need to challenge that.

Not registering for Self Assessment. This sounds obvious, but some subcontractors simply don’t register, assuming their contractor handles everything. They don’t. If you’re self-employed under CIS, you must file Self Assessment.

Late filing. You can still claim, but HMRC penalties for late returns eat into the benefit.

Claiming personal expenses as business ones. Even minor inaccuracies here can trigger a compliance check. And nobody wants that.

The Timeline: What to Expect

| Stage | Approximate Timeframe | Notes |

|---|---|---|

| Gather documents | 1–2 weeks | Longer if chasing contractors for statements |

| File Self Assessment return | 1 day–1 week | Faster with professional help |

| HMRC processing | 2–6 weeks typically | Can extend to 10+ weeks in peak periods |

| Refund received | 3–5 days after processing | Paid to your nominated bank account |

What If You’re Employed AND Self-Employed?

Quite a few construction workers straddle both worlds — working as a PAYE employee for one company while taking subcontractor work on the side. This complicates things slightly, but it’s very manageable.

Your Self Assessment return will need to capture both income streams. The CIS deductions from your subcontractor income are declared and offset. Your PAYE income is included too, though the tax on that has already been deducted by your employer. HMRC looks at the whole picture to determine whether you’ve over or underpaid overall.

The key error people make here is forgetting to include both. Omitting your PAYE income doesn’t increase your refund — it just makes your return inaccurate, which HMRC will eventually spot.

Can You Claim Previous Years?

Yes. Up to four complete tax years back from the current date. So if it’s currently the 2025/26 tax year, you can potentially reclaim going back to 2021/22.

Each year requires its own Self Assessment return (or amendment, if you filed but didn’t include CIS deductions). The amounts can stack up — it’s not unusual for someone doing this retrospective exercise to recover £5,000, £8,000, or more once multiple years are factored in.

The clock is ticking though. Each year, the oldest claimable year drops off. This isn’t an area where procrastination pays.

If you need help working out what years you can still claim for and whether the figures justify the admin, the CIS refund claims service at Ask Accountant is specifically built for this kind of retrospective recovery work.

A Note on Limited Companies and CIS

Limited company subcontractors have a notably different experience under CIS, and this is where the most expensive mistakes tend to happen.

When a limited company receives CIS-deducted payments, the deductions are credited against the company’s employer PAYE liabilities — not the director’s personal tax. So if your company deducts £3,000 in PAYE from staff wages and has suffered £4,500 in CIS deductions from contractors, you can net these off and claim the £1,500 difference back from HMRC (or carry it forward).

If your company has no employees or very low PAYE liabilities, CIS deductions can accumulate quickly. HMRC’s system for reclaiming these is the Employer Payment Summary (EPS) — filed monthly through your payroll software.

Critically: this is separate from the company’s Corporation Tax return. The two mechanisms don’t interact directly. Getting this wrong means either leaving money on the table or — worse — claiming the same deduction twice, which HMRC takes very seriously.

Payroll management and CIS returns filing is a distinct competency, and it’s worth having someone who knows both sides of the equation.

Frequently Asked Questions

How long does a CIS refund take? After you file your Self Assessment return, HMRC typically processes refunds within 2–6 weeks. During peak periods (January/February), this can stretch to 10 weeks or more. You can check the status through your HMRC online account.

How much can I get back? It depends entirely on your deductions versus your actual tax liability. Someone deducted at 20% with significant business expenses and a quiet trading year could get most of that money back. Someone deducted at 30% who was never even registered? The refund could be considerable. There’s no typical figure — the range is genuinely wide.

Do I need an accountant to claim a CIS refund? No, you can file Self Assessment yourself. But accountants often identify expenses you’ve missed, ensure your deduction statements are complete, and can file faster — which means your refund arrives sooner. For complex situations (multiple years, limited company, mixed employment) professional help usually pays for itself.

What if my contractor didn’t give me deduction statements? Ask for them in writing. Contractors are legally required to provide monthly deduction statements within 14 days of the end of each tax month. If they refuse or can’t provide them, contact HMRC — they can sometimes cross-reference the contractor’s returns to confirm what was deducted.

Can HMRC refuse a CIS refund claim? They can query it or request evidence, yes. Full refusal is rare if your return is accurate. The risk of refusal rises if your expenses seem disproportionate, your income doesn’t match what contractors reported, or there are prior compliance issues on your record. Accuracy and documentation are your best defences.

What’s the difference between CIS and Self Assessment? CIS is the scheme under which contractors deduct tax from subcontractor payments. Self Assessment is the mechanism through which sole traders and partners report their income and expenses to HMRC — and through which CIS refunds are actually claimed. They’re connected but not the same thing.

I haven’t filed Self Assessment in years. Is it too late? Possibly not entirely. You can file late returns for up to four years (subject to penalties for lateness). But get advice before assuming you’re in the clear — the penalty structure for late filing means you want to understand the full picture before submitting. The self-assessment service covers exactly this scenario.

The Bigger Picture: CIS Refunds and Business Health

There’s something slightly frustrating about the CIS system — not because it’s unfair, exactly, but because it creates a cash flow asymmetry that hits small subcontractors hardest. You do the work, you invoice the contractor, but 20% of what you’ve earned disappears into HMRC’s coffers immediately. Then you wait. Potentially a year or more, depending on when you file.

For sole traders running lean businesses, that’s real working capital sitting idle.

This is why some subcontractors choose to work on getting their finances properly organised — not just chasing refunds reactively, but understanding what their ongoing liability actually is, planning for it, and filing promptly each year so the refund cycle is as short as possible. Business accounting services and bookkeeping aren’t glamorous, but they shorten that wait considerably.

And if you’re a contractor rather than a subcontractor — running your own workers under CIS — you have your own compliance obligations: verifying subcontractors, making monthly returns to HMRC, issuing deduction statements. Getting that wrong has its own sting. There’s a helpful overview of CIS accountant compliance mistakes worth reading if that’s your situation.

Ready to Claim Yours?

If you’ve been making CIS deductions and haven’t claimed back what you’re owed — or if you’re not sure whether you have or not — it’s worth finding out. The four-year window closes year by year, and the cost of not claiming is simply leaving your own money with HMRC.

Ask Accountant works with subcontractors and construction businesses across the UK, handling CIS refund claims, Self Assessment filing, limited company CIS returns, and related compliance work. Based at 178 Merton High St, London SW19 1AY, they’re reachable on +44(0)20 8543 1991 or through the contact page.

It won’t take as long as you think. And the refund almost certainly will be worth it.