Every landlord I’ve ever spoken to has the same story. It starts with one property, one set of keys, and the optimistic belief that it’ll “basically manage itself.” Fast-forward eighteen months: there are repair receipts stuffed inside an old envelope, a spreadsheet held together with crossed fingers and bad formulas, and a self-assessment deadline that seems to materialise earlier every year.

The search for a better system almost always leads to the same question — could QuickBooks for landlords UK actually fix this?

It’s a fair question. QuickBooks is the most-searched accounting software in Britain for a reason, and property income — with its peculiar mix of rental receipts, allowable expenses, mortgage interest headaches, and HMRC’s ever-tightening grip — does need something more robust than a colour-coded spreadsheet. But whether QuickBooks is that something? That depends enormously on the kind of landlord you are, how many properties you hold, and how comfortable you are navigating software that was largely designed with businesses selling goods and services, not renting bedrooms, in mind.

Let’s dig into it properly.

What QuickBooks Actually Offers Property Owners (and What It Glosses Over)

QuickBooks Online, the version most UK landlords end up on, is a genuinely capable bit of software. Bank feed connections, invoicing, expense categorisation, VAT returns, payroll if you have staff — it covers the accounting fundamentals well. For a plumber, a freelance designer, or a small retail business, it clicks into place almost immediately.

For landlords, it’s… a looser fit.

The core problem is that QuickBooks isn’t built specifically for property. There’s no native “tenancy” module, no rent schedule tracker, no automatic flagging when a lease expires. You can make it work for rental income — and plenty of landlords do — but it requires a fair bit of customisation that the software doesn’t walk you through. You’ll be creating your own chart of accounts, manually separating income by property, and working out how to handle things like deposit protection records or section 24 mortgage interest restrictions (more on that shortly) without much in-software guidance.

That said, here’s where QuickBooks for landlords UK does genuinely shine:

- Bank reconciliation is fast and largely painless once you connect your accounts

- Expense tracking for things like repairs, agent fees, and insurance is straightforward

- Self-assessment readiness — the reports it generates do translate reasonably well to the UK property income pages of a tax return

- Making Tax Digital (MTD) compliance — this matters more than many landlords realise right now, and QuickBooks is HMRC-recognised for MTD for Income Tax

The MTD Time Bomb Every UK Landlord Should Know About

Speaking of Making Tax Digital — this is not a background concern anymore.

HMRC’s MTD for Income Tax Self-Assessment (MTD for ITSA) mandates that landlords with gross property income above £50,000 must use compatible digital software to submit quarterly updates from April 2026. That threshold drops to £30,000 in April 2027, and eventually £20,000 is in the pipeline too.

If your rental income sits anywhere near those figures, you essentially need MTD-compatible software. QuickBooks is on the HMRC-approved list, which gives it a meaningful advantage over basic spreadsheets. This is perhaps the single strongest argument for QuickBooks for landlords UK right now — not because it’s perfect, but because it’s compliant, and compliance is non-negotiable.

⚠️ Worth knowing: Just being on compliant software doesn’t mean your submissions will be correct. MTD moves the deadline, not the responsibility. Landlords who don’t understand what they’re submitting quarterly can still end up with errors — just faster ones.

If you’re uncertain whether MTD applies to you yet, or how to set up your records correctly, it genuinely pays to speak with a property-experienced accountant before you’re scrambling in April.

Setting Up QuickBooks for Rental Properties: What It Actually Looks Like

Let’s say you’ve decided to try it. Here’s where most landlords hit friction:

Step one is connecting your bank account. Easy enough — QuickBooks integrates with most major UK banks including Barclays, HSBC, NatWest, and Lloyds. Transactions pull through automatically, which is the first genuine time-saver.

Step two is the bit that trips people up: setting up a sensible property-by-product or property-by-class structure. Because QuickBooks doesn’t have a property module, the workaround is to use either Classes or Locations (available on higher-tier plans) to tag income and expenses by individual property. If you have three properties, this is manageable. If you have twelve, you’ll feel it.

Categorising expenses comes next. Allowable expenses for UK landlords are specific — letting agent fees, maintenance and repairs, buildings insurance, ground rent for leaseholds, accountancy fees. Things like mortgage capital repayments are not deductible (only the interest element, and even that’s been restricted since Section 24 changes). QuickBooks won’t stop you from miscategorising; it’ll just record what you tell it to.

Rent invoices can be set up as recurring invoices sent to tenants, which is actually quite useful. Whether tenants actually use them to pay through the system is another matter — most still pay by bank transfer, which means you’re reconciling rather than collecting through QuickBooks anyway.

There’s a useful existing resource on setting up QuickBooks for UK rental properties if you want to go deeper on the technical setup side.

How Does QuickBooks Compare? A Snapshot for UK Landlords

| Feature | QuickBooks Online | Xero | Dedicated Property Software (e.g. Landlord Vision) | Spreadsheet |

|---|---|---|---|---|

| MTD for ITSA Compatible | ✅ Yes | ✅ Yes | Varies by provider | ❌ No |

| Built-in tenancy management | ❌ No | ❌ No | ✅ Yes | Manual only |

| UK bank feed integration | ✅ Strong | ✅ Strong | Limited | ❌ No |

| Section 24 mortgage interest handling | Manual workaround | Manual workaround | Some built in | Manual |

| Monthly cost (approx.) | £15–£35+ | £16–£47+ | £5–£30 | Free–£10 |

| Accountant access / collaboration | ✅ Excellent | ✅ Excellent | Variable | Clunky |

| Learning curve | Moderate | Moderate | Low (for landlords) | Low initially |

Prices approximate and subject to change. QuickBooks and Xero frequently run promotional discounts for new subscribers.

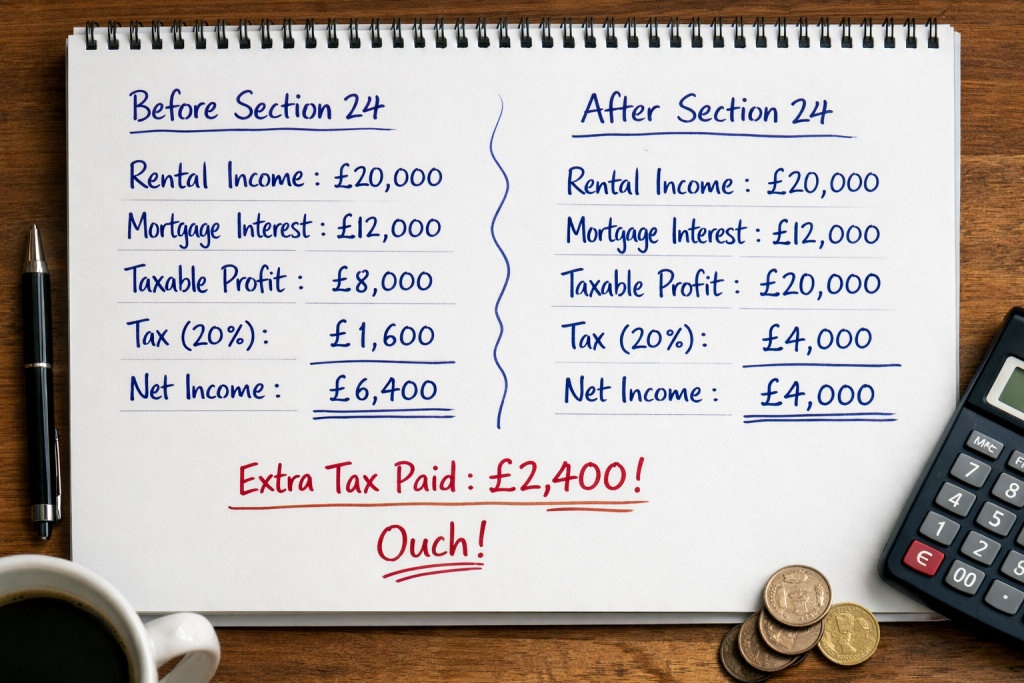

Section 24 and Why Your Software Choice Quietly Matters

If you own buy-to-let property as an individual (not through a limited company), Section 24 of the Finance Act 2015 is already affecting your tax bill — and most landlords still underestimate it.

Before 2020, you could deduct your full mortgage interest against rental income before calculating tax. Now, you can only claim a 20% tax credit on that interest, regardless of whether you’re a higher-rate taxpayer. For someone in the 40% tax bracket, this is a painful difference.

QuickBooks doesn’t automatically account for this. You’ll need to track your mortgage interest separately, ensure it’s not being counted as a direct expense in your profit calculation, and apply the credit adjustment at tax return time. It’s not impossible — but it’s a step that software designed for general businesses simply won’t flag for you.

This is one of those moments where the right accountant pays for themselves. A good one familiar with property accounting will set up your QuickBooks chart of accounts to handle this correctly from the start, rather than letting you discover the mistake after submission.

Who Actually Benefits Most from QuickBooks for Landlords UK

Here’s my honest take, after all of it:

QuickBooks for landlords UK works well if you:

- Already use QuickBooks for another business or self-employment and want to consolidate

- Have a modest portfolio (under eight properties, roughly) and want solid expense tracking plus MTD compliance in one place

- Work with an accountant who’s familiar with QuickBooks — the accountant access features are genuinely excellent, with real-time collaboration built in

- Need a proper audit trail for HMRC purposes rather than loose receipts

It’s probably the wrong choice if you:

- Need tenancy management, lease tracking, or rent arrears alerts — you’d need separate software alongside QuickBooks, which doubles your cost and admin

- Have a large portfolio where property-specific reporting becomes cumbersome without a dedicated property module

- Are a complete accounting novice with no appetite to learn — the setup for property use is not intuitive

For accidental landlords (you inherited one flat, you’re not building an empire), the honest answer might be that a good cloud-based spreadsheet plus a bookkeeping service is cheaper and less faff than a full QuickBooks subscription. It’s not glamorous advice, but there it is.

The QuickBooks Plans Available in the UK Right Now

QuickBooks UK currently offers three main tiers for small businesses and landlords:

| Plan | Approx. Monthly Cost | Key Features Relevant to Landlords | Property Class/Location Tracking |

|---|---|---|---|

| Simple Start | ~£15/month | Income/expense tracking, bank feeds, basic reports, 1 user | ❌ No |

| Essentials | ~£25/month | All above + 3 users, bill management, time tracking | ❌ No |

| Plus | ~£35/month | All above + 5 users, Classes and Locations, project tracking, budgeting | ✅ Yes — essential for multi-property landlords |

If you have more than one property and want to track finances per property, you effectively need the Plus plan. Budget accordingly.

A Note on QuickBooks and Limited Company Landlords

If you’ve incorporated your portfolio — or you’re considering it — QuickBooks becomes a somewhat better fit, ironically. Limited companies aren’t subject to Section 24 restrictions in the same way (they pay corporation tax on profits and can still deduct mortgage interest as a business expense), and QuickBooks handles corporate accounting quite capably.

The question of whether to hold property personally or through a limited company is a big one with no universal answer. Stamp duty, corporation tax rates, extraction costs, and inheritance planning all feed into it. If you’re weighing this up, business advice from a specialist can save you considerably more than the cost of the conversation.

There’s also a reasonable argument that moving to a limited company structure makes proper accounting software — QuickBooks included — more clearly worth the investment. Your reporting obligations are more formal, your accounts need to be filed at Companies House, and the audit trail matters more.

Cloud Accounting and Why the Days of “I’ll Sort It in January” Are Ending

This is probably the broader point underneath all the QuickBooks specifics.

The direction of travel for UK landlords and HMRC is unmistakably toward real-time, digital record-keeping. MTD for Income Tax isn’t just an inconvenience — it’s a structural shift in how the government collects data on property income. Quarterly reporting means quarterly attention to your numbers, not an annual panic in January.

Cloud accounting — whether that’s QuickBooks, Xero, or something more property-specific — is the infrastructure of that shift. Landlords who’ve already adapted are finding it genuinely less stressful than the annual scramble, even if the setup took some effort. Those who haven’t are looking at a compulsory change anyway, just with less time to do it gracefully.

The switch to QuickBooks is covered thoroughly in this guide: Switch to QuickBooks UK today.

Frequently Asked Questions About QuickBooks for Landlords UK

Can I use QuickBooks for a buy-to-let property in the UK?

Yes — QuickBooks Online can be used to track rental income and allowable expenses for buy-to-let properties. It’s not purpose-built for property management, but with some customisation it handles the accounting side competently. You’ll need the Plus plan if you want to track multiple properties separately.

Is QuickBooks HMRC-approved for Making Tax Digital?

QuickBooks Online is on HMRC’s list of MTD-compatible software for both VAT and Income Tax Self-Assessment. This matters if your gross property income exceeds £50,000 from April 2026 (dropping to £30,000 in 2027).

What’s the best accounting software for landlords UK?

There’s no single answer — it depends on your portfolio size and needs. QuickBooks for landlords UK suits those who want robust general accounting with MTD compliance. Landlord-specific tools like Landlord Vision or Arthur Online offer better tenancy management. Xero is a strong alternative if you prefer a slightly cleaner interface.

Does QuickBooks handle Section 24 mortgage interest correctly?

Not automatically. You’ll need to manually separate mortgage interest in your accounts and apply the 20% tax credit adjustment at the self-assessment stage. An accountant who knows property will set this up correctly.

How much does QuickBooks cost for UK landlords?

Plans range from approximately £15/month (Simple Start) to £35/month (Plus). For landlords needing per-property tracking via Classes and Locations, Plus is effectively the minimum viable plan.

Can a landlord do their own bookkeeping with QuickBooks?

Absolutely — many do. The more useful question is whether they’re doing it correctly. Property income has enough tax-specific quirks (Section 24, capital vs. revenue expenditure, wear and tear changes) that having an accountant review your setup at the start — and annually — is worth considerably more than the cost.

Do I need an accountant if I use QuickBooks?

Software records transactions; accountants provide judgement. QuickBooks won’t tell you whether a refurbishment counts as capital expenditure or an allowable repair. It won’t flag if your structure is tax-inefficient. It won’t spot that you’ve missed a claimable expense. The software and the professional are genuinely complementary, not alternatives.

Should You Actually Use QuickBooks?

Look — QuickBooks for landlords UK isn’t a bad choice. It’s a capable, MTD-compliant, cloud-based accounting platform that millions of UK businesses use successfully. For landlords, the wrinkle is that you’ll need to bend it slightly to fit your use case, rather than having it meet you where you are.

If you’re methodical, if you have a bookkeeper or accountant on hand, or if you’re already in the QuickBooks ecosystem for another reason, then yes — it makes sense. The bank feeds alone will save you hours.

If you want software that thinks like a landlord — that tracks tenancy renewals, sends rent reminders, and understands the difference between a repair and an improvement without you having to explain — then you might also want dedicated property management software alongside it, or instead.

And if you’re sitting there with a growing portfolio, a complicated ownership structure, and a vague anxiety about whether you’re doing any of this correctly — that’s the sign to get proper property accounting support before QuickBooks (or any software) can actually help you.

At Ask Accountant, based in Merton, South London, the team handles exactly this kind of situation — landlords who’ve been managing everything themselves and hit a point where the complexity outgrew the system. Bookkeeping, self-assessment, tax advisory, and proper setup on whatever software you’re using — it’s the kind of support that makes the difference between software that creates a digital mess and software that actually works.

Give them a ring on +44(0)20 8543 1991 or drop into 178 Merton High St, London SW19 1AY if you’d rather talk it through in person. Sometimes the most useful thing is a straight conversation.

Further Reading

- QuickBooks for Real Estate Rental Properties – Complete UK Setup Guide 2025

- Property Accounting Services – Save Thousands on Tax with a Pro

- Switch to QuickBooks UK Today

- Small Business Accounting Services Explained

- Cloud Accounting – Why London Businesses Are Making the Switch

- HMRC – Making Tax Digital for Income Tax (external)

- HMRC Allowable Expenses for UK Landlords (external)