Lost the receipt. Again. It happens to everyone — the crumpled till slip that went through the wash, the petrol station that printed something so faded it might as well pass for a Rorschach test, the parking machine that just… didn’t. So here’s the question that sends business owners spiralling at 11pm before a VAT return falls due: can you claim VAT without a receipt, or have you waved goodbye to that £8.40 of input tax for good?

Short version: sometimes, yes. Longer version — and this is the bit that actually matters — it depends on how much, what you bought, and whether you can prove the thing happened at all. Let me untangle it, because the rules are weirdly specific and most online answers either oversimplify or scare you into binning legitimate claims.

The £25 Rule Everyone Half-Remembers (and Usually Gets Wrong)

There’s a genuine concession buried in HMRC’s guidance. You can reclaim VAT without a receipt on individual purchases of £25 or less, including the VAT, provided the supplier is VAT-registered. This sits in HMRC’s VAT Notice 700, and it’s the rule everyone in the pub seems to know about but nobody can quote properly.

Here’s the catch nobody mentions. HMRC never intended that £25 allowance as a get-out-of-jail card for forgetful directors. It grew out of much older legislation covering situations where suppliers genuinely couldn’t issue a receipt — think coin-operated machines, road tolls, car park meters, and (charmingly outdated) phone calls from public payphones. The ‘£25 receipt’ concept comes from an old, often misunderstood piece of legislation that originally let businesses claim VAT back on purchases from coin-operated machines, such as telephone boxes and parking machines, which historically gave no receipts.

So can you claim VAT without a receipt for a £20 lunch on the basis of “it’s under £25”? Technically the concession exists. Practically? With coin-operated phone boxes a rarity and parking machines commonly issuing receipts these days, as a rule of thumb you shouldn’t try to claim VAT without a valid VAT receipt, or you may end up dealing with incorrectly charged VAT. The myth has outgrown the rule.

A warning dressed up as friendly advice: Build a habit of claiming under-£25 amounts with no paperwork and you create a pattern. HMRC compliance officers train their eyes to spot exactly that. One lost receipt looks human. Forty of them raises a flag.

What HMRC Wants Before You Can Reclaim VAT

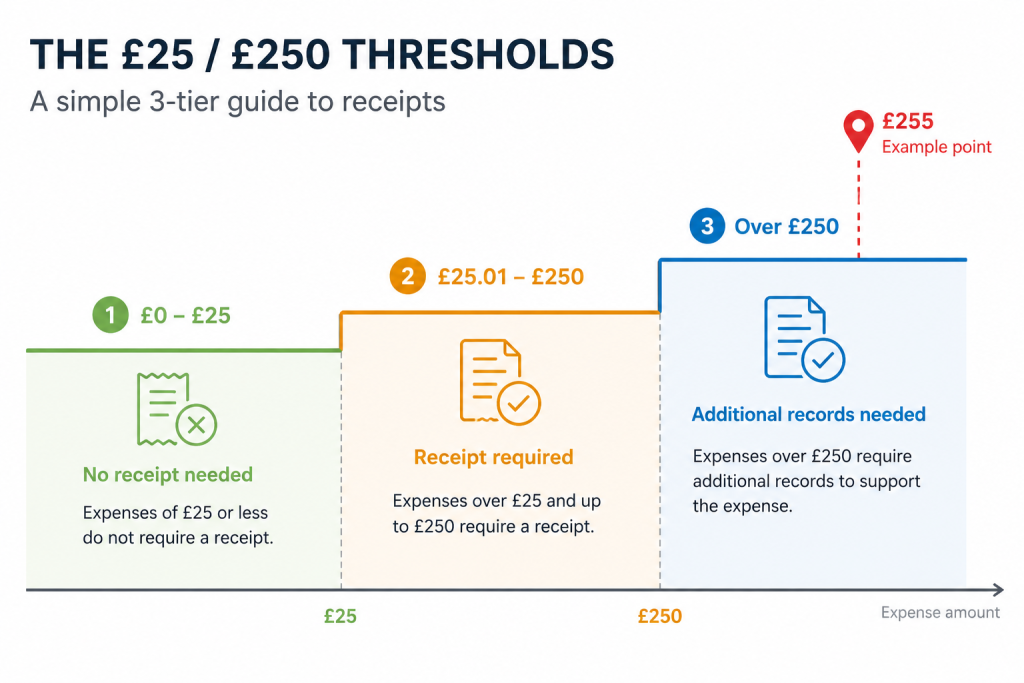

To work out whether you can claim VAT without a receipt, you first need to know what counts as evidence. There’s a hierarchy, and most everyday spending never reaches the full version.

A full VAT invoice sets the gold standard. A simplified (or “less detailed”) VAT invoice is what the petrol station, the high-street shop or the café hands you. HMRC accepts less detailed invoices where the tax-inclusive value of the supply comes to £250 or less — and that single line solves most of life’s receipt panic, because your retail till receipt usually is a valid simplified VAT invoice already. You just didn’t clock it.

The dividing lines, laid out plainly:

| Purchase value (inc. VAT) | What you need to reclaim the VAT | Must it show your business name? |

|---|---|---|

| £25 or less | Concession may apply — no receipt needed for specific items (tolls, parking machines, vending). Supplier must be VAT-registered. | No |

| £25.01 – £250 | Simplified VAT invoice (retail receipt): supplier name, address, VAT number, date, description, VAT rate | No |

| Over £250 | Full VAT invoice — including your name and address | Yes |

That £250 line is sharper than people expect. A marketing agency bought software licences for £255 and kept only a simplified receipt; HMRC found that because the total was over the simplified threshold, the lack of the agency’s name and address on the document made the claim invalid. Five pounds over the line and the rules change entirely. Brutal, but that’s the system.

Can You Claim VAT Without a Receipt When It’s Genuinely Lost?

This is where the real question lives — not the tidy £25 hypotheticals, but the £180 invoice from a supplier who’s stopped answering your emails. Can you claim VAT without a receipt when the only trace left is a line on a bank statement?

Maybe. And that “maybe” is doing a lot of work.

HMRC holds the discretion here. They don’t have to refuse a claim simply because the paper’s missing — they can accept alternative documentary evidence once you satisfy them that the purchase happened and that the supplier genuinely charged VAT. To claim input tax successfully, a business must hold appropriate evidence; without it, HMRC can dispute the claim even where the underlying transaction is genuine — though other forms of documentation may also work depending on the nature of the supply.

What helps your case:

- A bank or credit card statement showing the payment to a named, VAT-registered supplier

- A supplier confirmation — many will happily reissue an invoice if you ask

- An internal exception note explaining what was bought, why, and what you did to find the missing document

- A consistent record everywhere else, so this is plainly the exception

A blunt truth from the trade: for VAT claims, detailed notes and bank statements may not pass muster on their own, so if you don’t hold a proper VAT receipt, talk to your accountant about whether to include the expense on your VAT Return. A bank statement proves you paid someone. It doesn’t prove how much of that payment counted as VAT — and that distinction decides the whole game. This is the precise sort of grey area where a conversation with Ask Accountants UK Ltd earns its keep, because you rarely want to make the judgement call on a borderline claim alone, the night before filing.

Three Places People Quietly Lose VAT

A few situations break the simple rules in ways worth flagging.

Reclaiming VAT on fuel and mileage

Reclaiming VAT on business mileage feels like it should skip the receipt entirely — you’re paying a per-mile rate, after all. It doesn’t. Drivers who claim VAT on mileage but keep no VAT receipt make a common, costly mistake; you must keep a VAT receipt for the fuel you buy before you can reclaim VAT on business mileage. Your petrol receipts need to cover at least the fuel value of the mileage you claim. No receipts, no reclaim. It trips people up constantly.

When a receipt won’t help anyway: entertainment

Even a flawless receipt can’t rescue the VAT on entertaining clients — HMRC blocks it outright. You cannot recover input tax on the provision of business entertainment expenses, and business entertainment differs from staff entertainment, which follows its own treatment. So in this one case, the missing receipt never mattered.

A receipt in someone else’s name

A frequent worry: the invoice carries your employee’s name, not the company’s. The law lets only the person or business that receives the supply reclaim the VAT — but where an invoice shows an employee’s details and the purchase served your business, you can still reclaim it, typically for subsistence or motoring costs. Common sense wins here, which feels rarer than it should in tax.

A Quick, Slightly Untidy Reference of Common Spends

I’ve kept this one deliberately rough-and-ready — it’s the cheat sheet I’d actually scribble for a client, not a polished compliance manual.

| Spend | Receipt needed? | Notes |

|---|---|---|

| Car park machine (£3) | Not strictly | £25 concession territory — but grab the receipt if the machine gives one |

| Coffee & sandwich, £6.50 | Yes, ideally | Till slip = simplified invoice. Don’t lean on the £25 myth |

| Office chair, £140 | Yes | Simplified VAT invoice fine (under £250) |

| Laptop £620 | Yes — full invoice | Over £250, so it must carry your business name & address |

| Road toll | No | Classic coin-operated-style exemption |

| Fuel for mileage claim | Yes | Receipts must cover the fuel value claimed |

(Yes, that last row’s a little crooked — leaving it. Real notes look like this.)

Why Any of This Matters More Than It Used To

Two reasons. First, Making Tax Digital. VAT-registered businesses now keep digital records and file through compatible software, so your evidence trail shows up far more clearly — and HMRC can audit it far more easily — than the shoebox era ever allowed. If that shift still rattles you, our piece on Making Tax Digital for VAT walks through what compliant record-keeping looks like day to day, and HMRC’s own VAT record-keeping guidance sets out the bare minimum.

Second, the registration threshold. The VAT registration threshold sits at £90,000 for the 2025–2026 tax year, measured against your taxable turnover over any rolling 12-month period. Cross it — you can check the rules on GOV.UK’s register for VAT page — and the whole question of whether you can claim VAT without a receipt suddenly lands on your desk, with HMRC expecting you to keep VAT records for six years. Plenty of newly-registered businesses learn the rules the hard way, mid-investigation.

And on that note: poor receipt discipline is one of the quiet triggers that turns a routine check into a full enquiry. If a letter from HMRC ever lands, our HMRC investigations team handles exactly this, and tidy bookkeeping is the cheapest insurance against ever needing them.

The Practical Bottom Line

Can you claim VAT without a receipt? In narrow, specific cases — sub-£25 items like tolls and machines — yes, by concession. For most everyday spending, your retail till slip already counts as a valid simplified invoice, so you never really went “without a receipt” to begin with. And when paper truly vanishes, HMRC can accept alternative evidence — but you carry the burden of proving both the purchase and the VAT, and a bank statement alone rarely clears that bar.

My honest advice after years of watching this play out? Treat the £25 concession as a safety net for the unavoidable, not a strategy. Photograph receipts the moment they hit your hand — your future self, the one staring at a VAT return at midnight, will thank you.

If your records are a patchwork and a deadline is looming, it’s worth a proper conversation before you file something you’ll have to unpick later. The team at Ask Accountants UK Ltd — 178 Merton High St, London SW19 1AY, 020 8543 1991 — offers VAT, bookkeeping, cloud accounting and tax compliance support, and a ten-minute call usually costs nothing but settles the question for good. Get in touch here if a missing receipt is keeping you up.

Frequently Asked Questions

Can you claim VAT without a receipt on purchases under £25? Yes, by concession, on specific items such as car park machines, road tolls and vending machines, as long as the supplier holds VAT registration. Keep it for genuinely receipt-less situations rather than routine spending.

Is a bank statement enough to claim VAT without a receipt? On its own, usually not. A statement proves you paid a supplier but won’t show how much VAT the supplier charged. HMRC may accept it as part of a wider evidence package, though it rarely stands alone.

Do I need my business name on a receipt to reclaim VAT? Only for purchases over £250 (including VAT), which need a full VAT invoice showing your name and address. Below that, a simplified retail receipt does the job.

What if a supplier won’t give me a VAT receipt? Ask HMRC to consider the claim by giving them the facts and any alternative evidence. They may exercise discretion once you show that the purchase happened and the supplier charged VAT.

How long must I keep VAT receipts? Six years, matching HMRC’s record-keeping requirements for VAT-registered businesses.