VAT on service is one of the most misunderstood corners of UK tax law, and it catches out even experienced business owners. Somewhere between “I’ll sort the VAT later” and an unexpected letter from HMRC, a lot of people learn a painful lesson: VAT on services does not behave like VAT on goods, and treating them the same is how penalties happen. If you sell consultancy, design work, IT support, coaching, marketing, freelance writing, construction labour, or pretty much anything that isn’t a physical product changing hands, this is the tax rulebook you actually need to understand — not the shortened version that gets taught in a five-minute “VAT basics” video.

I’ve sat across the table from enough business owners to know the moment it clicks (or doesn’t). Someone starts invoicing a client in Berlin, or takes on a subcontractor, or crosses £90,000 in turnover without quite noticing, and suddenly VAT on services stops being an abstract compliance topic and becomes a live problem with a deadline attached. So let’s take this properly, in order, without the jargon-soup.

VAT on Service: What Actually Counts as a “Service”?

This sounds like an obvious question until you’re three years into running a business and genuinely unsure. HMRC’s definition is broad: a service is basically anything you supply that isn’t goods. Consultancy, hire of staff, software licences, digital downloads, repair work, professional advice, hairdressing, gardening, freelance design — all services. The tax treatment of VAT on services hinges less on what the service is and more on where it’s supplied and who it’s supplied to, which is where most of the confusion starts.

Compare that to goods, where VAT largely follows the physical movement of the item. Services have no physical form to track, so the rules had to invent something else: the “place of supply.” That single concept quietly runs the entire show.

Place of Supply: The Rule Behind VAT on Service

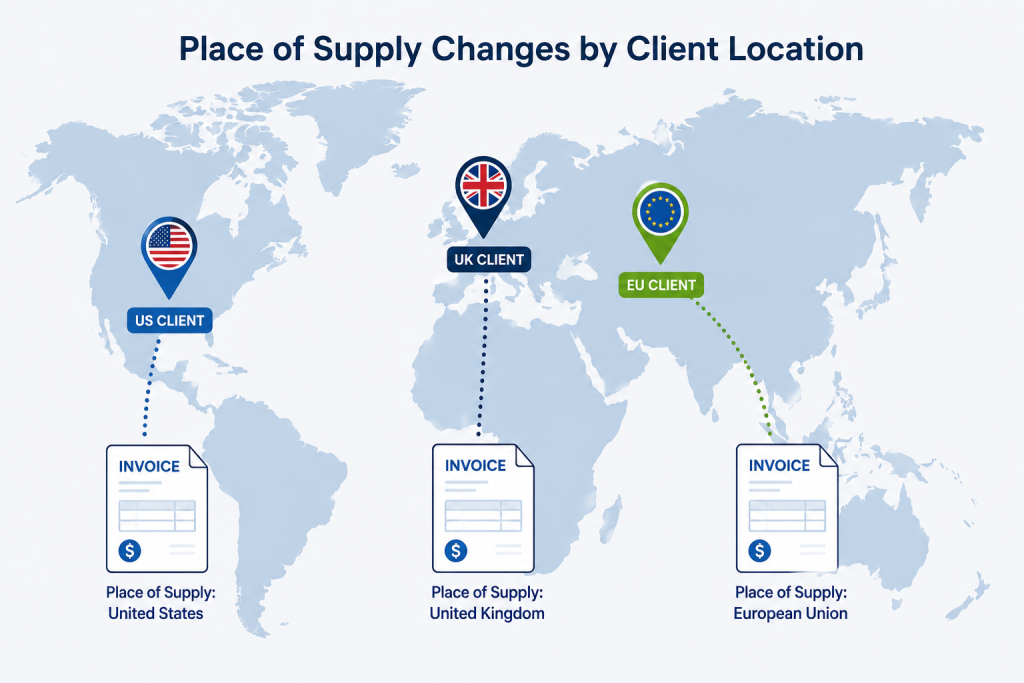

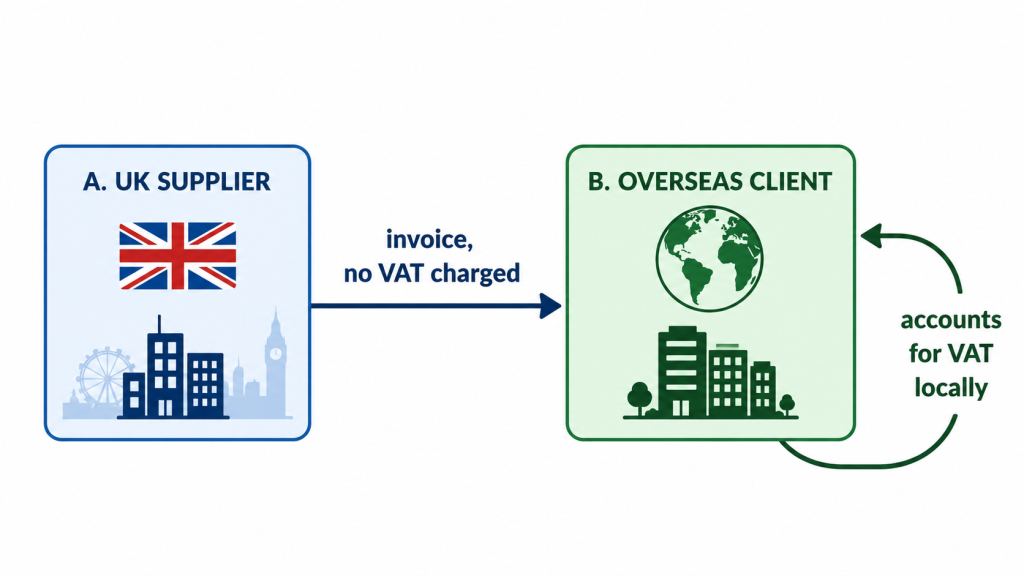

Here’s the bit that catches people out constantly, and I mean constantly. For business-to-business (B2B) services, the general rule is that the place of supply is wherever your customer is based, not where you are. Sell consultancy to a company in France, and — assuming the general rule applies rather than one of the exceptions — the place of supply is France. You typically don’t charge UK VAT at all; the customer accounts for it themselves under the reverse charge in their own country.

Business-to-consumer (B2C) services usually flip the other way: the place of supply is generally where you, the supplier, belong. Sell the same consultancy to a private individual in France, and UK VAT rules on services would normally apply instead.

There are exceptions layered on exceptions — services related to land and property, admission to events, restaurant and catering services, hiring of transport — each with its own special place-of-supply rule that overrides the general one. HMRC’s own guidance on the place of supply rules for services runs to dozens of pages for exactly this reason. Nobody memorises all of it. What matters is knowing the general rule, recognising when your service might sit in an exception category, and checking before you invoice rather than after.

VAT on Services Rates: 20%, 5%, 0% and the Ever-Confusing “Exempt”

Most services in the UK sit at the standard rate of 20%. But not all of them, and the gaps between categories aren’t always logical (welcome to tax law). A handful of services get the reduced 5% rate — certain energy-saving installations, for instance — and a small list qualifies for zero-rating, which is different from being exempt even though both mean “no VAT charged.” The distinction matters enormously for reclaiming input VAT, and it’s the sort of detail that trips up otherwise switched-on business owners.

| VAT Treatment | Typical Services | Can You Reclaim Input VAT? |

|---|---|---|

| Standard Rate (20%) | Consultancy, IT support, marketing, most professional services | Yes |

| Reduced Rate (5%) | Certain energy-saving installations, some residential renovation work | Yes |

| Zero-Rated (0%) | Some construction of new dwellings, certain exports of services | Yes |

| Exempt | Insurance, certain finance, some education and health services | No (generally) |

Full and current details sit on HMRC’s official VAT rates page and in VAT Notice 700, which is the closest thing to a VAT bible that exists. Bookmark it. You’ll be back.

When You Actually Have to Register for VAT on Services

The threshold that governs VAT on services (and goods, for that matter) is £90,000 of taxable turnover in any rolling 12-month period — not a tax year, a rolling window that resets every month. Cross it and you have 30 days to register. Miss that window and HMRC can backdate your liability, which is about as fun as it sounds.

A few things people get wrong here:

- It’s turnover, not profit. A service business with thin margins and £95,000 of billings is over the threshold even if it made almost nothing.

- Exempt income doesn’t count toward the threshold, but zero-rated income does. This surprises people constantly.

- Voluntary registration is a legitimate strategy, particularly if most of your clients are VAT-registered businesses who can reclaim what you charge them anyway. Registering early can also mean reclaiming VAT on your own costs — software subscriptions, equipment, professional fees — sooner.

We’ve written more on the mechanics of this in our guide to company VAT registration, including the pros and cons that don’t get discussed enough.

Reverse Charge: The Rule Everyone Forgets Applies to VAT on Services

If there’s one concept around VAT on services that genuinely deserves its own warning sign, it’s the reverse charge. Under this mechanism, instead of the supplier charging VAT, the customer accounts for both the output and input VAT on the transaction — effectively cancelling each other out on their own return. It applies to a huge range of cross-border B2B services and, domestically, to certain construction industry supplies under the VAT domestic reverse charge for building and construction services.

Quick warning, not a footnote: if you’re a subcontractor in construction and you’re still adding 20% VAT to invoices for services that should fall under the domestic reverse charge, stop. You could be sitting on VAT you were never supposed to collect, and unpicking that with HMRC is nobody’s idea of a good afternoon.

Get this wrong in either direction — charging VAT when the reverse charge should apply, or not charging when it shouldn’t — and you’re looking at corrected invoices, amended returns, and awkward conversations with clients. Ask around any accountancy office and you’ll hear at least one reverse-charge horror story a week.

Digital Services: The Overseas Headache Nobody Warns You About

Selling software subscriptions, online courses, or digital downloads to consumers abroad brings its own layer of VAT on services complexity. Historically this meant registering for VAT in every EU country your customers were based in, or using a scheme like the EU’s One Stop Shop (OSS) to simplify reporting. Post-Brexit, UK businesses selling digital services to EU consumers generally can’t use the EU’s OSS directly and often need a non-Union OSS registration or country-by-country registration instead.

It’s genuinely one of the more painful corners of VAT, and honestly? A lot of small digital businesses under-comply here simply because the compliance burden feels disproportionate to their turnover. That’s not advice to ignore it — it’s an observation about why so many people do, and why it tends to catch up with them eventually.

Invoicing for VAT on Services Properly

A VAT invoice for services needs specific information: your VAT registration number, the tax point (usually the invoice date or completion of service, whichever is earlier), a description of the service, the rate applied, and the VAT amount shown separately from the net figure. Miss any of this and, technically, the invoice isn’t valid for VAT purposes — which matters enormously if your client tries to reclaim the VAT you charged them.

| Invoice Element | Notes |

|---|---|

| VAT registration number | Must appear clearly |

| Tax point | Date of supply, unless invoice issued within 14 days |

| Net amount | Before VAT |

| VAT rate & amount | Shown separately, per rate if mixed |

| Total | Gross figure |

(Yes, that second table is a little untidy — one column’s centred, one’s right-aligned, one’s left, and it’s honestly a decent reflection of what half the invoices we see actually look like before we tidy them up.)

Common VAT on Services Mistakes I See on Repeat

Some of these are almost formulaic at this point:

- Charging VAT on services that should have fallen under the reverse charge, or vice versa.

- Forgetting that a service delivered digitally to an overseas consumer might trigger foreign VAT obligations.

- Registering late because turnover crept past £90,000 without anyone tracking it monthly.

- Assuming all professional services sit at 20% without checking for exemptions (finance, insurance, certain education).

- Not keeping digital records that satisfy Making Tax Digital requirements — more on that below.

None of these are unusual errors. They’re the ordinary, everyday kind that happen because running a business leaves precisely zero spare hours for tax research, and honestly, that’s fair enough — it’s not your job to know this stuff cold. It’s ours.

Making Tax Digital and VAT on Services

Since MTD for VAT became mandatory, VAT-registered businesses have needed to keep digital records and submit returns through compatible software rather than typing figures into HMRC’s old portal. It sounds like a hassle, and setting it up can be, but most service businesses find that once cloud accounting software is properly linked to invoicing, VAT on services reporting becomes far less of a quarterly scramble. We go into more detail on this in our piece on Making Tax Digital for VAT, and separately on how VAT accounting works day to day for businesses that haven’t quite made the leap yet.

Reclaiming VAT on Services: The Bit People Forget to Ask About

Registration isn’t only an obligation — it’s also an opportunity to reclaim input VAT on legitimate business costs: software, equipment, professional subscriptions, even certain travel costs tied to delivering a service. Businesses that focus purely on the “charging VAT” side of things often leave money on the table by not properly reclaiming VAT on their own purchases. Our guide to reclaiming VAT for business savings walks through what typically qualifies.

Sole traders in particular sometimes assume VAT registration is something only “proper companies” deal with. It isn’t. If you’re weighing this up, it’s worth reading our take on sole trader VAT registration before deciding either way.

A Word on Getting It Wrong

HMRC does investigate VAT compliance, and services businesses — with their trickier place-of-supply questions and reverse charge quirks — are not immune. If you’ve had a letter, or you suspect a past return might have errors in it, addressing it proactively is almost always better than waiting. We’ve written separately about what an HMRC tax investigation actually involves, if that’s useful context.

Frequently Asked Questions

Do I need to charge VAT on services to overseas clients? It depends on the place of supply. For B2B services to business customers outside the UK, the general rule usually means no UK VAT is charged, with the reverse charge applying instead. For B2C sales, UK VAT often still applies, subject to exceptions.

Is VAT on services always 20%? No. Most services sit at the standard 20% rate, but some qualify for the 5% reduced rate, zero-rating, or exemption depending on what’s being supplied.

What’s the VAT threshold for service businesses in 2026? £90,000 of taxable turnover in any rolling 12-month period, the same threshold that applies to goods. The deregistration threshold sits at £88,000.

Can I register for VAT voluntarily even under the threshold? Yes. It’s a genuinely useful option for service businesses whose clients are mostly VAT-registered, since they can usually reclaim the VAT you charge without it affecting their real cost.

What happens if I get the place of supply wrong? You risk charging VAT that shouldn’t have been charged (or the reverse), which typically means correcting invoices, amending VAT returns, and potentially facing penalties if HMRC finds the error first.

Where This Leaves You

VAT on services isn’t a topic that rewards guesswork, and it’s rarely as simple as “check the rate and move on.” Between place of supply, reverse charge, digital service rules, and the ordinary business of registering and invoicing correctly, it’s genuinely one of the areas where a second pair of eyes pays for itself. If you’d rather have someone check your VAT position than lie awake wondering about it, Ask Accountants UK Ltd works with service businesses across London on exactly this — VAT accounting and compliance, bookkeeping, cloud accounting setup, and the rest of the accounts and tax picture — from our office at 178 Merton High St, London SW19 1AY. A quick call to 020 8543 1991 usually sorts out more than an afternoon of forum-reading ever will.