Here’s something most people selling on eBay, taking freelance payments, or running a small side hustle through PayPal genuinely don’t know: HMRC can see PayPal transactions data. Not in some vague, theoretical, “they could if they wanted to” way. In a direct, structured, legally-backed way that’s been quietly tightening for years. If you’ve ever wondered whether those PayPal receipts exist in a kind of financial blind spot, they really don’t.

This isn’t a scare piece. But it is an honest look at what HMRC actually sees, when they start looking, and — just as practically — what you should be doing about it.

The Short Answer (and Why It’s More Complicated Than You Think)

Yes. HMRC can see PayPal transactions. Under UK law, particularly through powers granted by the Finance Act 2011 and subsequent amendments, HMRC has the authority to issue what’s called a third-party information notice — which means they can compel PayPal (and any similar platform) to hand over account data, transaction histories, and identity information about specific users.

PayPal is also registered as a payment service provider in the UK and, like banks, is subject to reporting obligations under anti-money-laundering regulations. So it’s not just that HMRC can ask — it’s that PayPal must comply.

But here’s where it gets genuinely interesting. HMRC doesn’t sit around manually requesting individual PayPal account data for millions of people. That would be impractical. Instead, they use a system.

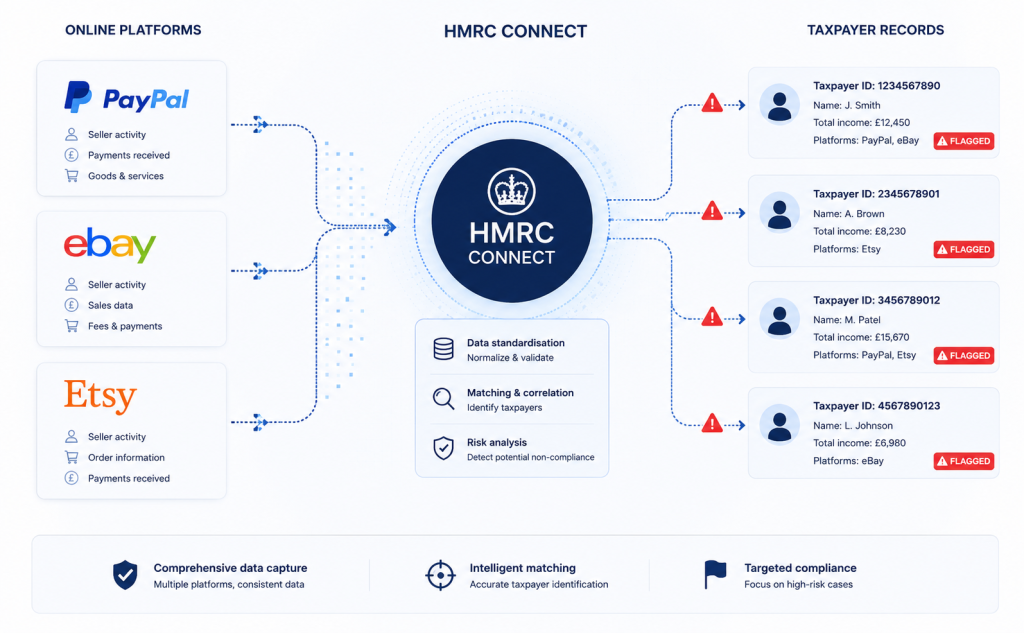

HMRC CONNECT: The Engine Behind the Curtain

Most people have never heard of HMRC CONNECT, but it’s the reason the taxman is far more data-savvy than the average person assumes.

CONNECT is HMRC’s data-matching and risk-analysis platform. It pulls in information from dozens of sources — bank accounts, Land Registry records, DVLA data, social media in some cases, and crucially, third-party payment platforms including PayPal. The system cross-references this data against what individuals and businesses declare on their tax returns.

When something doesn’t add up — say, your self-assessment shows £12,000 in income but your PayPal history suggests significantly more coming in — CONNECT flags it. A human compliance officer then reviews the flag and decides whether to open an enquiry.

This is why the question “can HMRC see PayPal transactions?” isn’t really a yes/no question. The better question is: what happens when HMRC’s system notices a discrepancy in your PayPal activity?

The answer is: they write to you. And that letter is not pleasant.

What the Digital Reporting Rules Actually Say

From January 2024, the UK implemented DAC7 — a set of EU-derived rules that the UK chose to adopt (despite Brexit) because, well, digital income doesn’t respect borders. Under DAC7, digital platforms — including PayPal, eBay, Vinted, Airbnb, Etsy, and Fiverr — are legally required to report seller information directly to HMRC if:

- A seller completes 30 or more transactions in a calendar year, or

- A seller receives over £1,735 in total payments (this threshold may be updated — worth checking current HMRC guidance)

The platform collects your name, address, date of birth, Tax Identification Number (usually your UTR or National Insurance number), and a breakdown of your earnings. This goes straight to HMRC. No request needed. No warrant. Automatic.

So if you sold 35 handbags on Vinted last year and received £2,000 in PayPal payments, HMRC already has a file with your name on it.

⚠️ Something worth knowing: The DAC7 rules apply even if you think you’re just clearing out your wardrobe. HMRC distinguishes between genuine personal sales and trading activity — but the platform doesn’t make that judgement. The data goes across regardless. The judgement about whether tax is owed is yours to make and declare.

The “Casual Seller” Myth

There’s a deeply persistent belief that casual, occasional sellers — the eBay regulars, the Facebook Marketplace flippers, the freelancers taking the odd PayPal invoice — are somehow below HMRC’s radar. They’re not. Or at least, they’re much less below it than they used to be.

The £1,000 Trading Allowance does exist. If your total income from casual trading (not employment, not rent) is under £1,000 in a tax year, you don’t need to report it or pay tax on it. That’s a genuine relief for very small earners.

But once you cross that threshold — even slightly — you’re technically required to register for self-assessment and declare the income. Most people don’t do this. Most people assume no one is watching. And now, with DAC7 data flowing automatically from PayPal to HMRC, that assumption carries real risk.

The team at Ask Accountants UK Ltd regularly see clients come in after receiving an HMRC compliance letter — sometimes covering multiple tax years — because their PayPal or platform income was never declared. The bills (including interest and penalties) can be substantial. It’s one of those situations where a conversation with an accountant before the letter arrives would have saved a lot of grief.

How HMRC Investigates PayPal Income Specifically

So you’ve been flagged. What actually happens?

HMRC tends to open what’s called an aspect enquiry first — focused on one specific part of your tax return (or your absence of one). They might write asking you to explain the payments received into your PayPal account during a particular tax year.

If the enquiry widens — because the initial responses raise more questions than they answer — it can escalate into a full investigation. At that point, HMRC can request:

- Complete PayPal transaction histories (which they may already have)

- Bank statements to check for undeclared income

- Business records, invoices, purchase histories

- Explanation of any unusually large transfers or payments

The investigation process has five distinct stages, and each one is incrementally more serious. Getting professional representation early — at stage one — is usually far cheaper and less stressful than trying to navigate it alone.

Business PayPal Accounts: Even Less Ambiguity

If you hold a Business PayPal account, the reporting landscape is even clearer. Business accounts are explicitly linked to commercial activity in HMRC’s view, and the data reporting obligations under DAC7 apply from the first transaction.

More importantly, if you’re VAT-registered (or should be — once your taxable turnover exceeds £90,000), PayPal income counts toward that threshold. Treating PayPal receipts as separate from your “real” business income isn’t a grey area; it’s simply incorrect accounting.

Cloud accounting tools like QuickBooks and Xero can link directly to PayPal and pull in transactions automatically, which makes reconciliation far less painful and means your records stay current. It’s the sort of thing that takes a few minutes to set up and saves hours (sometimes days) at year-end.

A Comparison of How HMRC Accesses Different Payment Platforms

| Platform | Automatic DAC7 Reporting? | HMRC Can Request Data Directly? | Threshold (approx.) |

|---|---|---|---|

| PayPal (Personal) | Yes (from Jan 2024) | Yes | 30+ transactions or £1,735+ |

| PayPal (Business) | Yes | Yes | From first transaction |

| eBay | Yes | Yes | 30+ transactions or £1,735+ |

| Etsy / Vinted | Yes | Yes | 30+ transactions or £1,735+ |

| Bank transfers (direct) | No (not under DAC7) | Yes (via information notice) | No fixed threshold |

| Cash payments | No | Indirectly (via lifestyle checks) | N/A |

Note: Thresholds and rules are subject to change. Always verify current figures on the HMRC website or with a qualified accountant.

What HMRC Is Particularly Alert To

There are patterns that tend to catch HMRC’s attention more than others. Not all of these will trigger an investigation — but any combination of them increases the odds considerably.

- Income that grows year-on-year on a platform but doesn’t appear in self-assessment filings — HMRC’s CONNECT system is particularly good at spotting this kind of trajectory

- High-volume low-value transactions that look like retail activity but aren’t declared as trading income

- PayPal Friends & Family payments used for business purposes — there’s a persistent myth that using F&F avoids scrutiny; it doesn’t, because HMRC looks at the pattern of payments, not just the category the sender chose

- Overseas PayPal income where currency conversion creates additional complexity — HMRC expects this to be declared in sterling at the exchange rate applicable when received

One thing that surprises people: HMRC doesn’t need to prove intent to evade tax to issue a penalty. If income is undeclared — even through ignorance — the penalty structure can still be substantial. Careless errors attract lower penalties than deliberate concealment, but “I didn’t know” is not a complete defence.

What You Should Do if You’ve Been Receiving PayPal Income

Here’s the practical bit. Not advice you’ll need once — advice you might need right now.

1. Work out what you’ve actually received. Download a full transaction history from PayPal. Separate personal receipts (repayments from friends, birthday money, etc.) from anything that looks like income from goods or services sold.

2. Check your tax position. The Trading Allowance means the first £1,000 of trading income is tax-free. If you’re above that, you likely need to file a self-assessment tax return.

3. If you’re behind, consider disclosing voluntarily. HMRC’s Contractual Disclosure Facility (CDF) and various voluntary disclosure routes exist specifically because HMRC prefers people to come forward rather than be caught. Voluntary disclosure typically results in lower penalties than a compelled investigation.

4. Get proper bookkeeping in place going forward. Whether you use cloud accounting software or a bookkeeping service, tracking PayPal income as it arrives is dramatically easier than reconstructing a year’s worth of transactions under pressure.

The Disclosure Question: A Quick Reference

| Situation | Likely HMRC Response | Recommended Action |

|---|---|---|

| Under £1,000 trading income, no other triggers | Unlikely to investigate | No action needed (keep records) |

| £1,000–£10,000 undeclared, no return filed | May issue aspect enquiry | Voluntary disclosure + catch-up returns |

| Multiple years of undeclared income | Full investigation likely if flagged | Professional representation, urgent disclosure |

| Already received HMRC letter | Investigation is open | Do not respond alone — get specialist help immediately |

| PayPal income fully declared annually | No issue | Carry on, keep records for 5+ years |

FAQs: Can HMRC See PayPal Transactions?

Does HMRC automatically receive my PayPal data every year? From January 2024, yes — if you meet the DAC7 thresholds (30+ transactions or £1,735+ in a year). Below those thresholds, reporting isn’t automatic, but HMRC can still request data directly from PayPal using a third-party information notice.

What if I only use PayPal for personal payments — splitting bills, receiving money back from friends? Personal transfers between individuals generally don’t constitute trading income and don’t need to be declared. The key distinction is whether money is received in exchange for goods or services. If in doubt, an accountant can help you categorise payments correctly.

Can HMRC go back more than one year on PayPal income? Yes. HMRC can typically investigate up to four years back for innocent errors, six years for careless errors, and twenty years for deliberate non-compliance. If you’ve had undeclared PayPal income over several years, that entire period is potentially in scope.

I used PayPal Friends & Family — does that mean HMRC can’t see it? No. The F&F label is a PayPal payment method designation, not an HMRC-recognised classification. HMRC looks at the substance of a transaction — what money was paid for — not how the sender categorised it.

I sell items I’ve bought for personal use — is that still taxable? Not usually, if you’re selling at a loss or for what you paid. Capital Gains Tax applies when you sell personal possessions (called chattels) for more than £6,000 profit — though an exception exists for most everyday items. If you’re buying items specifically to resell at a profit, that’s trading income regardless of the platform.

What if HMRC contacts me about undeclared PayPal income? Don’t ignore the letter and don’t respond hastily without advice. Contact a specialist accountant — ideally one with experience in HMRC investigations — as soon as possible. The earlier you get professional guidance, the better the likely outcome.

Keeping PayPal Income Above Board: It’s Simpler Than People Think

The honest truth is that declaring PayPal income correctly isn’t especially complicated — it’s just something most people never set up a system for. A decent bookkeeping service or cloud accounting setup will handle the categorisation automatically. Filed properly through a self-assessment tax return, the income is on record, the tax is paid, and there’s nothing for HMRC’s systems to flag.

The problem is never the people who do this correctly. It’s the people who assume that PayPal is somehow different from a bank account — that it lives outside the ordinary rules of UK tax. It doesn’t.

If you’re unsure about your position, whether you owe tax on past PayPal income, or whether your current declaration covers everything it should, Ask Accountants UK Ltd — based in 178 Merton High St, London SW19 1AY — offers specialist support across self-assessment, tax compliance, and HMRC investigations. A call to 020 8543 1991 costs nothing and might save considerably more than that.