You filed your Self Assessment. You hit submit. And then — possibly minutes later, possibly three weeks later while eating a sandwich — you realised something was wrong. Maybe you forgot a freelance income stream. Maybe you entered your pension contributions in the wrong box and maybe you genuinely have no idea what you did, but the numbers don’t look right and your stomach is quietly telling you something.

Here’s the good news: yes, you can amend a tax return after submission. HMRC fully expects that mistakes happen, and the system is built to accommodate corrections. The less comforting news? There are time limits, specific rules about how corrections are made, and a few situations where the process gets considerably more complicated. Getting this wrong the second time — when HMRC is already watching — isn’t ideal.

This guide covers everything you need to know about amending a submitted UK tax return, from the basics of how to do it to the messier questions about what happens when the deadline for amendments has already passed.

The Window You Have to Work With

When you ask can I amend a tax return after submission, the first thing to understand is that you’re working against a clock. HMRC gives you 12 months from the original filing deadline to make amendments to a Self Assessment tax return — not 12 months from when you submitted it, but from the deadline itself.

For most people, that means:

- Tax return for the 2023–24 tax year → filing deadline was 31 January 2025 → amendment deadline is 31 January 2026

- Tax return for the 2024–25 tax year → filing deadline is 31 January 2026 → amendment deadline is 31 January 2027

So if you filed early — say, in October — you actually have more than 12 months from your submission date to make changes. That’s one of the underappreciated advantages of getting your return in well before the deadline. Rushing to file in January and then discovering an error two months later still leaves you with plenty of runway; discovering one in February two years later does not.

⚠️ One thing worth flagging: If you submitted a paper tax return rather than using HMRC’s online system, the amendment process is different and involves a written letter rather than an online change. More on that below.

How to Actually Make the Change (Online vs. Paper)

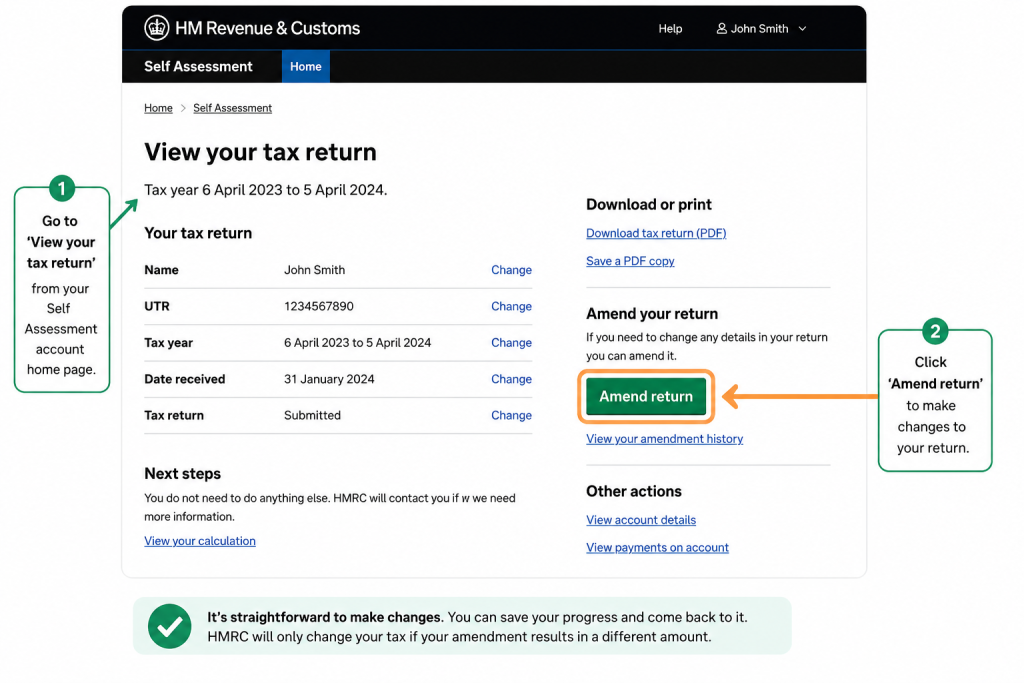

Amending Online Through Your HMRC Account

For most people who filed digitally, amending a tax return after submission is fairly straightforward. You log into your HMRC Personal Tax Account, navigate to your tax return for the relevant year, and select the option to make a correction. The system will ask you to go through the relevant sections and change the figures you need to update.

A few things to keep in mind:

- You can only amend online within the 12-month window. After that date, the system simply won’t let you edit the return.

- HMRC will automatically recalculate your tax liability based on the updated figures. If you’ve underpaid, you’ll owe the difference (plus potential interest). If you’ve overpaid, you’ll receive a refund.

- Keep your own records of what changed and why — HMRC doesn’t require a written explanation for standard amendments, but if questions arise later, you’ll want documentation.

When You Filed on Paper

If your original return was submitted on paper, amending it means writing to HMRC directly. You’ll need to send a letter explaining which figures are incorrect and what the correct figures should be. Include your Unique Taxpayer Reference (UTR), the tax year in question, and — if possible — a copy of the relevant pages with the correct entries marked clearly.

Send it to:

HMRC Self Assessment HM Revenue & Customs BX9 1AS

This is slower, less satisfying, and somewhat anxiety-inducing compared to clicking a button online. If you expect to be making corrections in future years, it might be worth switching to online filing.

What Happens If You’ve Missed the 12-Month Amendment Deadline?

This is where things get thornier. If you want to amend a tax return after the 12-month window has closed, you cannot do it yourself through the standard process. But that doesn’t necessarily mean the situation is hopeless.

You have a couple of routes:

1. Make an overpayment relief claim If you believe you’ve overpaid tax as a result of an error on your return, you can make a formal claim under HMRC’s overpayment relief rules. The time limit here is four years from the end of the relevant tax year — so considerably longer, which is useful.

This isn’t the same as amending your return; it’s a separate claim process. You’ll need to write to HMRC explaining the error and why you believe you’ve overpaid, providing supporting evidence. It’s not quick, and HMRC reserves the right to push back, but it’s a legitimate route.

2. Contact HMRC directly and explain your circumstances In certain situations — particularly where an error came to light through an HMRC enquiry or where there are genuinely exceptional circumstances — HMRC may exercise some discretion. Don’t bank on this. But it’s worth knowing the door isn’t necessarily completely shut.

3. Get professional help If you’re in late-amendment territory, this is genuinely the point at which speaking to a tax adviser pays for itself. The difference between a well-made overpayment relief claim and a poorly worded letter to HMRC can be significant, both financially and in terms of the response you get.

Common Reasons People Need to Amend a Tax Return

Why does this happen so often? In part, because tax returns are complicated. But some mistakes come up again and again:

- Forgetting income sources — a small amount of freelance work, dividends from shares, bank interest that fell below the reporting threshold the previous year but not this year

- Pension contributions entered incorrectly — either the wrong amount or claimed in the wrong section

- Capital gains errors — sale of shares or property where the original cost basis was misremembered

- Self-employment expenses overclaimed or underclaimed — people either include things they shouldn’t or forget legitimate deductions entirely

- Student loan repayments — sometimes ticked incorrectly

- Gift Aid declarations — if you made charitable donations under Gift Aid but forgot to declare them (or declared ones you shouldn’t have)

- High Income Child Benefit Charge — frequently misunderstood and sometimes missed entirely

The common thread? Most of these are genuine mistakes, not attempts at evasion. HMRC knows this. The amending process exists precisely because they’d rather you correct errors voluntarily than discover them later during a compliance check.

What If HMRC Corrects Your Return First?

Here’s a scenario that trips people up: HMRC itself can make corrections to your return within nine months of you filing it. These are typically minor arithmetic corrections or obvious errors — not full-blown amendments.

If HMRC corrects your return and you disagree with the correction, you have 30 days to reject it. You do this by writing to HMRC explaining why you believe their correction is wrong. This is different from making your own amendment — you’re essentially disputing their change rather than updating your figures.

If you do nothing within those 30 days, HMRC’s correction stands.

| Situation | What to Do | Time Limit | Result |

|---|---|---|---|

| Error found within 12 months of filing deadline | Amend online via HMRC account (or write in for paper returns) | 12 months from original deadline | Return updated; tax recalculated |

| Overpaid tax, missed the amendment window | Submit overpayment relief claim in writing | 4 years from end of relevant tax year | HMRC reviews; refund if approved |

| HMRC has corrected your return | Reject in writing if you disagree | 30 days from HMRC notification | HMRC reverts or disputes further |

| Underpaid tax discovered | Amend return and pay the difference | Within 12-month window; otherwise contact HMRC | May involve interest on unpaid tax |

| Under HMRC enquiry | Seek professional advice immediately | Depends on enquiry scope | Negotiated settlement or formal closure |

Amending a Tax Return When You’ve Underpaid

If your amendment reveals that you owe more tax than you originally paid, you’ll need to pay the difference. HMRC will charge interest on unpaid tax from the original payment deadline — typically 31 January following the tax year — regardless of when the error is discovered.

The current HMRC late payment interest rate sits above 7% (it fluctuates with the Bank of England base rate), so underpayment interest adds up faster than people expect. The sooner you identify and correct the error, the less interest accrues.

Penalties for underpayment are a separate matter from interest. If HMRC believes an error was careless rather than deliberate, penalties are typically lower — and making a voluntary correction before HMRC spots the issue generally attracts the lowest possible penalty loading. This is one of the strongest arguments for amending quickly rather than hoping nobody notices.

The Question Nobody Wants to Ask: What If the Error Wasn’t Accidental?

If you’re reading this because you know there was deliberate underreporting on your tax return — whether because someone advised you that it was fine, or because things got out of hand, or for any other reason — the answer is still: deal with it.

HMRC’s Contractual Disclosure Facility (CDF) exists specifically for situations involving deliberate tax fraud. It allows people to come forward voluntarily, disclose fully, and negotiate a settlement in a structured way. Coming forward voluntarily will almost always result in lower penalties than being caught.

This is not a situation to handle without proper professional support. An accountant or tax adviser with experience in HMRC investigations will know how to approach this without making things worse.

| Tax Year | Filing Deadline | Last Day to Amend | Overpayment Relief Claim By |

|---|---|---|---|

| 2021–22 | 31 Jan 2023 | 31 Jan 2024 ❌ passed | 5 April 2026 |

| 2022–23 | 31 Jan 2024 | 31 Jan 2025 ❌ passed | 5 April 2027 |

| 2023–24 | 31 Jan 2025 | 31 Jan 2026 ⏳ open | 5 April 2028 |

| 2024–25 | 31 Jan 2026 | 31 Jan 2027 ✅ open | 5 April 2029 |

Note: Overpayment relief deadlines run from 5 April at the end of the relevant tax year, not from the filing deadline. Always verify current deadlines with HMRC or a tax adviser.

Can You Amend a Tax Return That’s Already Under HMRC Enquiry?

Short answer: it’s complicated.

Once HMRC has opened a formal enquiry into your return under Section 9A of the Taxes Management Act 1970, your ability to amend that return yourself is restricted. You can still technically submit an amendment, but HMRC can set it aside and continue the enquiry based on the original figures.

If you’re in this situation, any corrections you want to make need to happen through the enquiry process itself — essentially as part of negotiations with HMRC. Getting professional advice here isn’t optional; it’s the only sensible path forward. The team at Ask Accountants UK Ltd handles HMRC investigations and enquiry support, and the sooner you get specialist help in these situations, the better your position tends to be.

Company Tax Returns: Slightly Different Rules

Everything above applies to personal Self Assessment returns. But if you run a limited company and need to amend a Corporation Tax return (CT600), the rules are similar but not identical.

You can amend a Corporation Tax return within 12 months of the filing deadline for that accounting period — which is itself 12 months after the end of the accounting period. In practice this gives you up to 24 months from the end of the period to make corrections, though the maths varies depending on when accounts are due.

As with Self Assessment, overpayment relief claims are available beyond that window, subject to the four-year time limit.

Voluntary Disclosure: Better to Own It

A thread running through all of this: HMRC has relatively little appetite to punish people who come forward voluntarily with corrections. The penalty regime under Schedule 24 FA 2007 is explicitly structured to reward disclosure — the penalty loading for an unprompted disclosure (you spotted the error and told HMRC before they asked) is meaningfully lower than for a prompted disclosure (HMRC spotted something and then you agreed).

The difference can be substantial. Penalties for careless errors where you disclose unprompted might be reduced to zero. The same error disclosed only after HMRC has launched an enquiry could attract a penalty of 15–30% of the tax owed. On a significant underpayment, that’s a large sum.

The practical implication: if you think you might have an error on a submitted return, don’t sit on it. Whether you’re within the 12-month amendment window or not, addressing it sooner is almost always the financially smarter choice.

A Practical Step-by-Step: Amending Your Self Assessment Return Online

- Log into your HMRC online account at gov.uk — use your Government Gateway credentials

- Navigate to ‘Self Assessment’ in your account dashboard

- Select the tax year you need to amend

- Choose ‘Amend return’ — this opens the return for editing

- Update the figures in the relevant sections — don’t change sections that are correct

- Review the recalculated tax liability before submitting

- Submit the amendment — HMRC confirms receipt online

- Make any additional payment due by the relevant deadline; if a refund is due, it will typically be processed within a few weeks

That’s it, in the uncomplicated version. If your situation involves missed deadlines, HMRC enquiries, or deliberate errors — go back to the earlier sections, and consider getting professional tax compliance support before taking any action.

Frequently Asked Questions

Can I amend a tax return after submission if I filed early? Yes — the 12-month amendment window runs from the filing deadline (usually 31 January), not from when you actually submitted. So if you filed in October, you still have until the following 31 January to make changes.

What if I find an error after the 12-month window? You can’t amend the return yourself, but you can submit an overpayment relief claim if you’ve paid too much. If you’ve underpaid, contact HMRC proactively — voluntary disclosure usually means lower penalties.

Will amending my tax return trigger an HMRC investigation? Not automatically. Amending a return is a normal part of the process and HMRC does not treat all amendments as suspicious. That said, a correction involving a significant additional payment or an unusual pattern of amendments could attract attention. There’s no way to guarantee you won’t be looked at, but making voluntary corrections is still far better than being caught.

Can I amend a tax return to claim expenses I forgot? Yes — as long as you’re within the 12-month window. Forgotten expenses are one of the most common reasons to amend a tax return after submission. Just make sure you have receipts and records to support the claim.

What if my employer issued a corrected P60 after I filed? If you received amended payslips, a corrected P60, or revised benefit figures from your employer, you can (and should) update your return with the correct figures. HMRC will cross-reference the figures your employer reports against what you’ve declared, so a mismatch between the two is worth correcting.

Does amending a tax return affect payments on account? Yes, potentially. If your amendment changes your tax liability significantly, HMRC may revise your payments on account for the following year. This can cut both ways — a lower liability might reduce future payments, while a higher one might increase them.

Can a tax adviser amend my return on my behalf? Yes — if you have an authorised agent (such as an accountant or tax adviser), they can amend your return on your behalf through HMRC’s agent services. If you’re dealing with a complex correction, this is often the easiest route. Self Assessment services from a qualified firm can handle the entire process.

Getting It Right the Second Time

Amending a tax return after submission is genuinely common — more so than most people realise, because most people assume they’re the only ones who make mistakes. They’re not. The UK tax system is complicated, deadlines are tight, and the information you need sometimes arrives after you’ve already filed.

The mechanics of the process are, mostly, manageable. What creates problems is leaving errors unaddressed, missing the amendment window without taking any alternative action, or discovering an issue after HMRC already has — at which point your options narrow considerably.

If you’re uncertain about an error, unsure whether something needs correcting, or dealing with a situation that’s more complex than a simple figure adjustment, speaking to a professional accountant is the most efficient first step. Ask Accountants UK Ltd (178 Merton High St, London SW19 1AY — you can reach the team on 020 8543 1991) offers personal tax planning and Self Assessment support for individuals and businesses across London and beyond. The sooner you get clarity, the more options you have.