Nobody tells you about the forms.

You lose someone. There’s grief, there’s funeral arrangements, there’s the slow and slightly surreal business of sorting through a life. And then — usually when you’re least equipped for it — HMRC hands you a document that looks like it was designed by a committee who genuinely enjoy making people feel weird.

Inheritance tax forms are, to put it plainly, a lot. But they don’t have to be a source of panic. Most people who need help filling in inheritance tax forms aren’t accountants, aren’t lawyers, and have never dealt with an estate before. That’s entirely normal. What you need is someone to walk you through it without drowning you in jargon — which is exactly what this guide is here to do.

Do You Even Need to File One? (A Question Worth Asking First)

Before anything else: not every estate requires a full inheritance tax return. This trips people up constantly.

If the total value of the estate is below £325,000 — the standard nil-rate band — and there are no complex assets or gifts to declare, you may only need to complete the shorter IHT205 form (or its online equivalent via the HMRC estate returns service). That said, the IHT205 has been discontinued for deaths on or after 1 January 2022, replaced by a simpler online reporting process for excepted estates. HMRC’s excepted estates guidance is worth reading before you assume the worst.

If the estate is taxable — or if you’re not certain — you’ll be dealing with the IHT400. That’s what most of this guide covers.

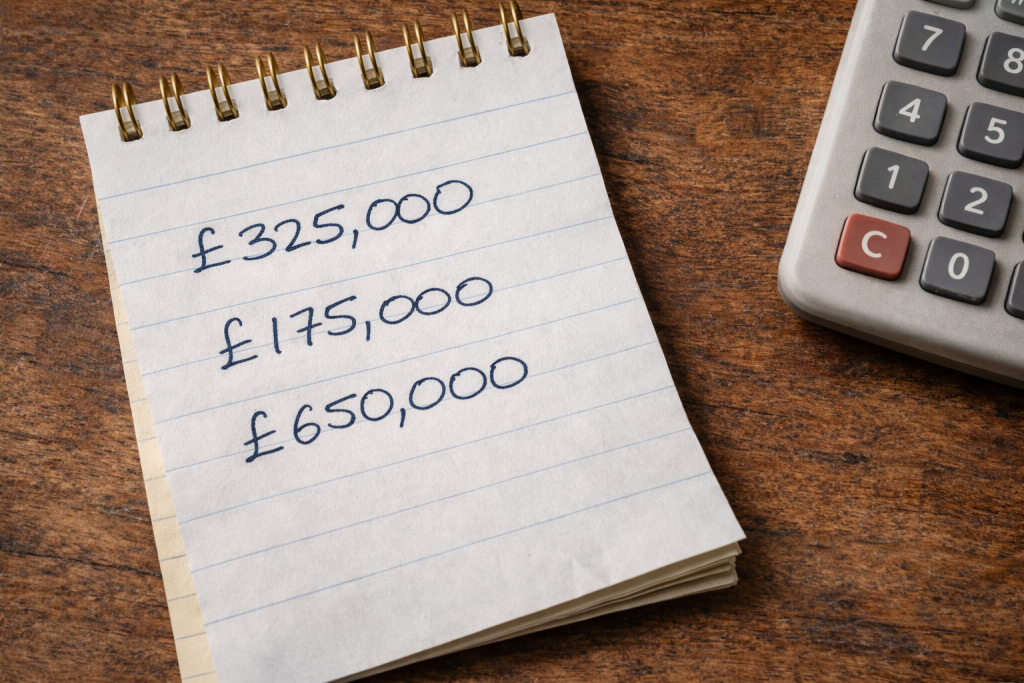

One thing to check: is there a surviving spouse or civil partner? Transfers between spouses are entirely exempt from inheritance tax, which changes the maths considerably. The unused nil-rate band from a deceased spouse can also be transferred, potentially doubling the threshold to £650,000. Worth knowing before you assume there’s a bill to pay.

The IHT400: What It Actually Is (Without the Drama)

The IHT400 is HMRC’s main inheritance tax return form. It’s where you declare everything — the estate’s assets, its debts, any gifts made in the seven years before death, and any reliefs or exemptions you’re claiming.

It comes with a set of supplementary pages called schedules, labelled IHT401 through to IHT436 (and a few more besides). You won’t need all of them — which ones apply depends entirely on the specifics of the estate. For example:

- IHT402 — if you’re claiming a transferred nil-rate band from a deceased spouse

- IHT403 — for gifts and lifetime transfers (this one matters if the deceased was generous in their later years)

- IHT404 — jointly owned assets

- IHT405 — houses, land, and buildings

- IHT421 — this one gets sent to the Probate Registry and is used to grant probate

The form itself runs to around 16 pages. Some of those pages will be irrelevant to you. But working out which pages are irrelevant takes a bit of knowledge — or a bit of help.

For a more detailed breakdown of each section, Ask Accountant’s IHT400 complete guide is a useful companion read.

Before You Put Pen to Paper: The Information You’ll Need

Trying to fill in the form before you’ve gathered everything is the single most common mistake. You’ll get halfway through, hit a question you can’t answer, and have to start over. So. Before you open the form:

Pull together the following:

- The deceased’s full name, date of birth, date of death, and last address

- Their National Insurance number

- Details of all bank and building society accounts (with balances at date of death)

- Property valuations — you’ll need a professional valuation, not just Rightmove estimates

- Details of any shares, ISAs, or investment accounts

- Outstanding debts: mortgages, credit cards, loans, utility bills owed at death

- Details of any gifts made in the seven years before death — this is the one that catches families off guard

- Life insurance policies and pension death benefits (some are exempt, some aren’t)

- Any business interests or agricultural land

The gifts question deserves a moment’s attention. Under the seven-year rule, gifts made within seven years of death may be subject to inheritance tax, with taper relief reducing the rate for gifts made between three and seven years before death. If your relative was generous — paid off a child’s mortgage, gave significant cash gifts at Christmas, helped with a deposit — those need to be declared. Even if they felt like ordinary family kindness at the time.

Walking Through the IHT400 (Section by Section, Without Falling Asleep)

Right. Let’s actually look at what the form asks.

Pages 1–3: Basic Information Name, address, executors. Straightforward. Don’t overthink it.

Pages 4–7: The Estate in the UK This is where you list the assets — property, bank accounts, investments, personal possessions. Each category has its own box. You’re giving the values at the date of death, not what things were worth six months later when you finally got round to selling them.

One thing that surprises people: household contents. You’re supposed to include them. HMRC doesn’t expect a furniture inventory; a reasonable lump-sum estimate is usually fine for standard domestic contents, though for valuable items — art, jewellery, antiques — you’ll want proper valuations.

Pages 8–10: Liabilities and Deductions Outstanding debts reduce the taxable estate. Mortgages, personal loans, credit card balances at the date of death — these go here. Funeral expenses are also deductible (within reason — HMRC won’t accept a bill for an elaborate wake).

Pages 11–13: Exemptions and Reliefs This is where it gets interesting, and where proper advice genuinely pays for itself.

Spousal exemption. Business Property Relief (BPR). Agricultural Property Relief (APR). Charitable donations. Each of these can significantly reduce the tax bill — or eliminate it entirely. But the rules around each are specific, and getting them wrong in either direction (under-claiming or over-claiming) creates problems.

If the estate includes a business — even a small one — business property relief could reduce its value for IHT purposes by up to 100%. That’s not a typo. But it has conditions attached, and claiming it incorrectly tends to attract HMRC’s attention.

Pages 14–16: Calculating the Tax The maths, essentially. By this point, if you’ve completed everything accurately, HMRC’s own calculation worksheet walks you through it. The standard rate is 40% on anything above the nil-rate band. If more than 10% of the net estate passes to charity, the rate reduces to 36%.

The Residence Nil-Rate Band: The Relief Nobody Mentions Enough

Here’s something that reduces inheritance tax bills for a lot of families, and yet somehow doesn’t get the attention it deserves.

Since 2017, there’s been an additional allowance called the Residence Nil-Rate Band (RNRB) — currently £175,000 per person — available when a main residence passes to direct descendants (children, stepchildren, grandchildren). Combined with the standard nil-rate band, a single person’s threshold rises to £500,000. For a married couple, potentially £1 million.

The rules around the RNRB get complicated when estates are large (it tapers away above £2 million), when the property has been downsized, or when it’s left in trust. But for many families with a family home and children, it’s a significant relief worth claiming — via IHT435 and IHT436.

For a fuller explanation of how allowances stack up, this guide to maximising inheritance tax allowances is worth reading alongside the official form guidance.

The Key Forms at a Glance

| Form | What It’s For | When You Need It |

|---|---|---|

| IHT400 | Main inheritance tax return | Taxable estates; estates where you’re unsure |

| IHT401 | Domicile outside the UK | Deceased was not UK-domiciled |

| IHT402 | Transferable nil-rate band | Claiming unused NRB from a deceased spouse |

| IHT403 | Gifts and lifetime transfers | Gifts made in the 7 years before death |

| IHT404 | Jointly owned assets | Jointly held property, bank accounts etc. |

| IHT405 | Houses, land, buildings | Any property owned by the deceased |

| IHT421 | Probate summary | Sent with IHT400 to support probate application |

| IHT435 / IHT436 | Residence nil-rate band | Home left to direct descendants |

What Happens After You Submit

You send the completed IHT400 (and any supplementary schedules) to HMRC’s Inheritance Tax office in Nottingham. Not online — by post, at least for now. The address is on the form.

Any tax due must be paid within six months of the end of the month in which the person died. Miss that deadline and interest accrues. The tricky bit: you often need money from the estate to pay the tax, but you can’t access the estate until you have probate, and you can’t get probate until HMRC has processed the return. Banks generally have a process for releasing funds specifically to pay IHT — it’s worth asking about this early.

HMRC’s current processing times for IHT400 returns have stretched in recent years. For the latest realistic timelines, this piece on IHT400 HMRC processing times gives a frank picture of what to expect.

A note on probate: The IHT421 schedule goes to the Probate Registry (in England and Wales) as part of your probate application. You can apply for probate online through HMRC’s government portal. HMRC and the Probate Registry communicate directly — you don’t need to chase both simultaneously.

Common Mistakes That Cause Delays (And How to Avoid Them)

This section is arguably the most useful in the whole article. These aren’t rare edge cases. They happen all the time.

Undervaluing property. HMRC has district valuers who check property valuations. If yours looks suspiciously low, they’ll query it. Get a proper RICS surveyor valuation — an estate agent’s guide price isn’t sufficient.

Forgetting gifts. We mentioned this already, but it bears repeating: any gift over the annual £3,000 allowance made in the seven years before death needs to be declared, even if it didn’t feel significant at the time.

Missing the IHT402. If the deceased’s spouse or civil partner died first and didn’t use their full nil-rate band, you can claim the unused portion. This is genuinely free money — or rather, a legitimate reduction in the tax bill — that executors sometimes miss entirely.

Not claiming Business Property Relief. If the estate includes shares in a trading company, or a business that qualifies, BPR can dramatically reduce or eliminate the tax on those assets. But you have to actively claim it.

Sending the form without signatures. Sounds absurd, but it happens. HMRC will simply send it back.

The Timeline: Realistic, Not Optimistic

| Stage | Typical Timeframe | Notes |

|---|---|---|

| Gathering valuations and documents | 4–8 weeks | Property valuations take time; don’t underestimate |

| Completing the IHT400 | 1–3 weeks | Longer with complex estates or business assets |

| HMRC processing time | 12–20 weeks (currently) | Has been longer in busy periods |

| Probate granted (after HMRC clearance) | 4–8 weeks additional | England and Wales; Scotland uses Confirmation |

| Estate distribution | Varies enormously | Depends on assets, disputes, property sales |

Note: These are approximate figures. Complex estates, HMRC queries, or disputed valuations extend timelines significantly.

Can You Submit the IHT400 Online?

Short answer: not fully, not yet.

As of 2025, the IHT400 itself must be submitted by post. Some related processes — including reporting excepted estates and applying for probate — can be done online, but the main return for taxable estates is still paper-based. HMRC has been working on digital improvements, but they’ve been slow to materialise.

For the full picture on what can be done digitally, this piece on submitting IHT400 online covers the current state of play honestly.

When Getting Professional Help Filling In Inheritance Tax Forms Is Worth Every Penny

Look. Plenty of executors complete these forms themselves. For straightforward estates — house, bank accounts, no lifetime gifts, no business interests — it’s absolutely manageable with patience and the right guidance.

But there are situations where professional help isn’t just convenient; it’s protective:

- The estate includes a business or partnership

- There were significant gifts in the last seven years

- The estate’s value is near the threshold (where small errors matter most)

- You’re claiming Business Property Relief or Agricultural Property Relief

- There’s property in multiple jurisdictions

- The deceased had complex investments or trusts

Getting help filling in inheritance tax forms from a qualified tax adviser means someone who knows what HMRC looks for, what triggers queries, and where reliefs are being left on the table. An error in the IHT400 doesn’t just delay probate — it can attract penalties and interest.

The team at Ask Accountant (based in Merton, South London at 178 Merton High St, SW19 1AY) deals with inheritance tax returns as part of their broader personal tax planning and tax advisory work. They’re not a probate solicitor — they’re the people who make sure the tax side is done accurately, reliefs are fully claimed, and HMRC doesn’t come back with questions six months later. If you’d rather talk it through than stare at a 16-page form, they’re reachable on +44(0)20 8543 1991.

Frequently Asked Questions

How long does HMRC take to process an IHT400? Currently between 12 and 20 weeks for straightforward returns, though this varies. Complex estates or queries from HMRC can extend the process considerably. Filing accurately and completely is the best way to avoid delays.

Do I need help filling in inheritance tax forms if the estate is small? If the estate qualifies as an “excepted estate” (broadly: under £325,000 with no complex assets), you likely won’t need the IHT400 at all. For estates near the threshold or with any complication, professional guidance is usually a good investment.

What is the deadline for submitting the IHT400? The return must be submitted within 12 months of the end of the month of death. Tax due, however, must be paid within six months. Interest runs on unpaid tax from the six-month point.

Can I fill in the IHT400 myself without a solicitor? Yes. Executors commonly complete the form themselves. HMRC provides official guidance notes alongside the form. For complex estates, a tax adviser rather than a solicitor is often more useful for the IHT element specifically.

What happens if I make a mistake on the IHT400? Errors can be corrected by writing to HMRC’s Inheritance Tax office. If underpaid tax is discovered, interest and potentially penalties apply. If you overpaid, HMRC will refund the difference. Honest mistakes are generally treated differently from attempts to conceal assets.

Is inheritance tax paid before or after probate? Technically before — or at least simultaneously. Banks will often release funds specifically to pay the IHT bill before probate is granted, precisely because of this chicken-and-egg situation. This is worth arranging early in the process.

What gifts count for inheritance tax purposes? Any gift made within seven years of death may be counted, unless it falls within an exemption (such as the annual £3,000 allowance, gifts from income, or small gifts of up to £250). For the full picture, HMRC’s guidance on inheritance tax gifts is a helpful starting point.