If you’ve ever invoiced a builder for £2,000 of labour and watched £400 quietly disappear before the payment landed, you’ve already met the Construction Industry Scheme. We just haven’t introduced you properly yet. So let’s fix that. How does CIS tax work, exactly, and why does the construction trade get its own special set of rules when the plumber down the road on PAYE doesn’t? This article walks through it from both sides of the invoice — contractor and subcontractor — without the jargon fog that usually swallows the topic whole.

Here’s the short version before we go deep. CIS is HMRC’s way of grabbing income tax at source from self-employed construction workers. Why? The industry has a long, slightly notorious history of cash-in-hand deals where the tax somehow never reached HMRC. So a contractor deducts a slice from a subcontractor’s labour payment and hands it straight to HMRC as an advance on that worker’s tax bill. Simple in theory. Gloriously fiddly in practice.

Why the taxman built a whole scheme around scaffolding and bricks

Back in 1972, the government noticed something. The construction sector leaked tax everywhere — itinerant, project-based, full of one-week jobs and self-employed grafters. Workers turned up, did a job, took their pay, and moved on before anyone could pin an Income Tax bill on them. The Construction Industry Scheme fixed that. HMRC has refined and re-refined it ever since, and the current version dates to April 2007.

The logic is almost old-fashioned: don’t trust the money to find its own way to HMRC. Take it at the moment it changes hands. That’s the whole philosophy. When you understand how does CIS tax work at its core, you realise it’s just a withholding mechanism — the same instinct behind PAYE, only bolted onto a sector that doesn’t have employers in the usual sense.

A quick note on who counts, because people get this wrong constantly. A contractor is anyone who pays subcontractors for construction work. That covers the obvious builders, but also property developers and even non-construction businesses that spend heavily on construction each year — the so-called “deemed contractors.” A subcontractor is the business or individual doing the work. And yes — you can be both at once, paying people below you while someone above pays you. Plenty of mid-sized firms juggle both hats. They register twice.

CIS Tax Rates: The Three Numbers That Decide What Disappears

This is the part everyone actually wants. The deduction rate isn’t random; it depends entirely on the subcontractor’s status with HMRC. There are three possibilities, and the gap between them is the difference between healthy cash flow and a permanent overdraft.

| Subcontractor status | Deduction taken | What it means in plain terms |

|---|---|---|

| Registered with CIS | 20% | The standard rate for anyone who’s bothered to sign up. Most subcontractors sit here. |

| Not registered | 30% | The lazy-tax. An extra 10% bleeds out simply because you skipped a free registration. |

| Gross Payment Status | 0% | Paid in full, no deduction at all — you settle your own tax later. The holy grail. |

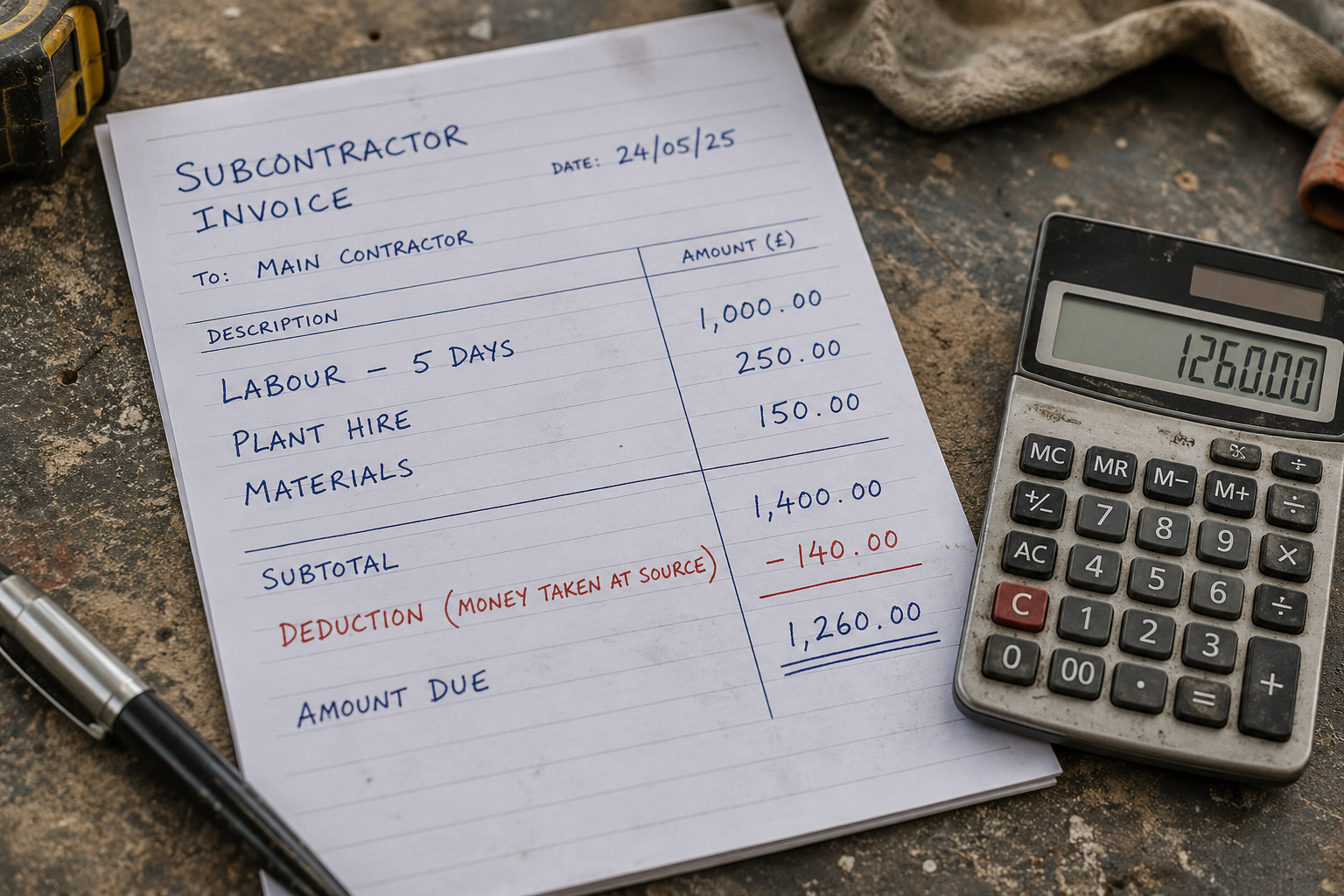

Notice that 10-point cliff between registered and unregistered? On a £40,000 year of labour that’s four grand of your own money sitting in HMRC’s account instead of yours, all because of a registration form. I’ve seen subcontractors leave that on the table for years out of sheer admin avoidance. Don’t be that person.

A tip most people learn the expensive way: CIS only ever touches the labour portion of an invoice — never materials, never plant hire without an operator, never VAT. So itemise. Lump £5,000 of timber into a single “labour” line and you hand HMRC a deduction on money that never owed tax in the first place. Split your invoices. Always.

How does CIS tax work day-to-day for the contractor?

If you’re the one paying, the scheme lands a genuine list of duties on your desk. First, before a single penny moves, you must verify every new subcontractor with HMRC. This is the step that tells you whether to deduct 20%, 30%, or nothing. Skip it and you’re guessing — and guessing wrong makes you liable for the shortfall, not them. That’s worth reading twice: if you fail to deduct what you should have, HMRC still wants the money from you.

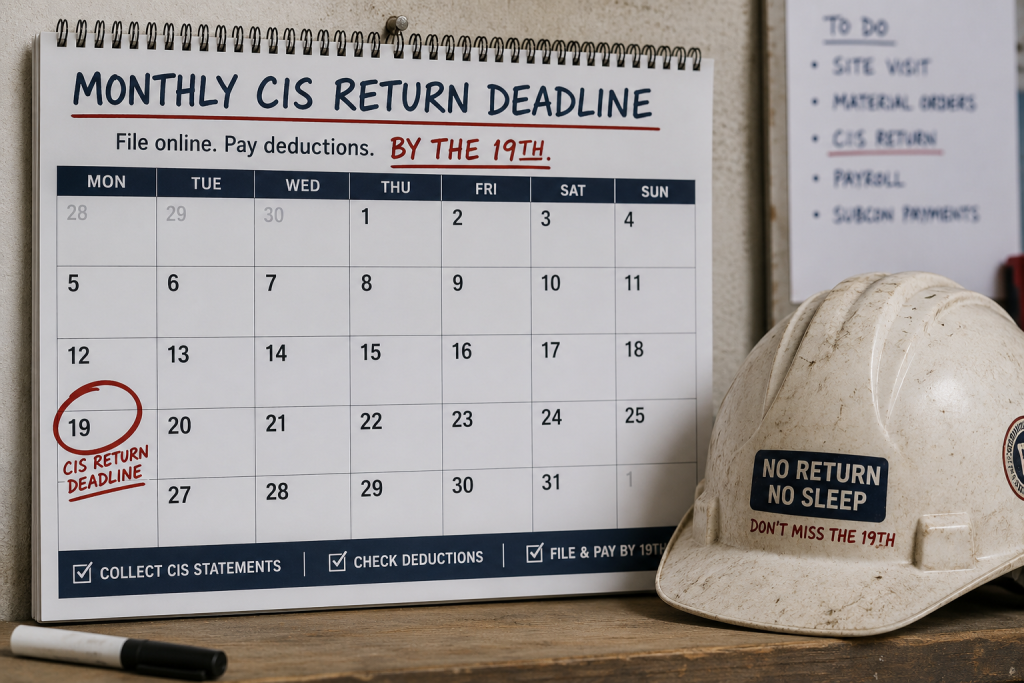

Then comes the monthly rhythm, which is the bit that trips up busy site managers. Each CIS “tax month” runs from the 6th of one month to the 5th of the next. By the 19th of the following month you must:

- File a monthly CIS return listing every subcontractor you paid and every deduction you made

- Pay those deductions over to HMRC (the 22nd if you pay electronically, the 19th if by post)

- Hand each subcontractor a payment and deduction statement — their proof that the tax has already gone to HMRC

Miss a payment month with no subcontractors? You still tell HMRC. File a nil return or notify them, otherwise their system assumes you’ve simply forgotten and starts the penalty clock. Speaking of which — those penalties stack up with a kind of grim efficiency:

| How late | Penalty |

|---|---|

| 1 day late | £100 |

| 2 months late | £200 (on top) |

| 6 months | £300 or 5% of the CIS due, whichever is higher |

| 12 months late | another £300 or 5% |

Let a return drift a full year unfiled and the penalties alone can clear £1,500 — before you’ve even touched the actual tax owed or the interest piling on top. The construction accounting side turns unforgiving fast. That’s exactly why so many firms hand the monthly filing to someone who does it for a living. (More on that below. I won’t pretend a guide written by accountants has no horse in this race.)

How Does CIS Tax Work for Subcontractors? An Advance, Not a Loss

Here’s the reassurance subcontractors rarely get told clearly enough. That 20% isn’t a tax on top of your normal tax. It’s a down payment. File your Self Assessment at year-end, and every pound the contractor deducted counts against your total Income Tax and National Insurance bill.

The contractor strips that 20% from your gross labour, ignoring every business cost you carry. So most subcontractors overpay by the time the year closes. Tools, mileage, protective gear, a slice of your phone bill — the contractor counted none of it when they lopped off 20%. A refund becomes the norm, not the exception. This is the satisfying part of understanding how does CIS tax work: the system tends to grab too much, and a clean return claws it straight back. Plenty of subcontractors never reclaim the four-figure sums HMRC still holds. If that’s you, our guide on how to claim a CIS refund is the place to start. The dedicated CIS refund claim service exists for one reason: the paperwork puts people off doing it themselves.

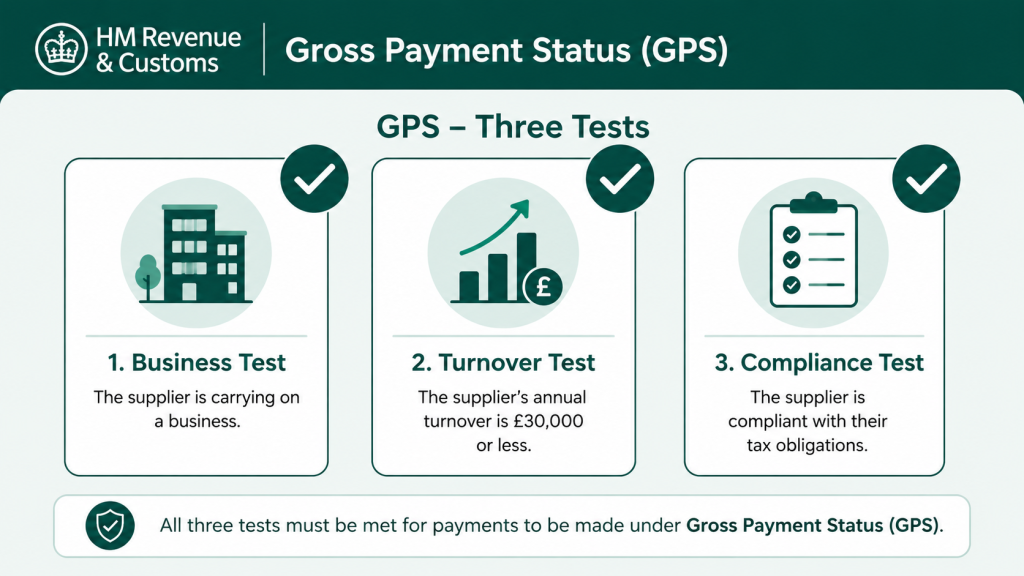

Chasing the zero: Gross Payment Status

Now for the prize. Gross Payment Status (GPS) means contractors pay your invoices in full — no 20%, no deduction, nothing. You handle the entire tax bill yourself once a year. For a subcontractor turning over £80,000, that’s roughly £16,000 of working capital staying in your account through the year rather than HMRC’s. Cash flow transforms.

HMRC doesn’t hand it out freely, though. You have to pass three tests:

- The business test — you genuinely do construction work in the UK and run the business through a UK bank account.

- The turnover test — net construction turnover (excluding VAT and materials) of at least £30,000 for a sole trader; £30,000 per partner or director, or £100,000 for the whole entity, for partnerships and companies.

- The compliance test — a clean 12-month record of filing returns and paying tax, PAYE, and VAT on time.

That compliance test is where applications die. HMRC has tightened its grip noticeably for 2025/26, with more frequent reviews and real-time monitoring replacing the old once-a-year glance. A single £100 penalty you forgot about, or a VAT payment that landed a few days late, can sink the whole thing. Apply from a position of strength, not hope.

CIS Tax Traps That Catch People Out

Some hard-won observations, in no particular order, from years of cleaning up CIS messes:

- Cleaning, surveying, and architecture aren’t always “construction.” The scope of what CIS covers is broader and stranger than people assume — scaffolding yes, carpet fitting sometimes, delivering materials no. Get the classification wrong and the deductions are wrong.

- Employment status is a separate landmine. If HMRC decides a “subcontractor” was really an employee in disguise, the contractor faces back-dated PAYE, NIC, and penalties. CIS does not make the employed-vs-self-employed question go away.

- Records matter for longer than you think. Keep CIS paperwork at least three years after the tax year ends — six is wiser, and saves you when an HMRC investigation comes knocking.

For a deeper look at the recurring blunders, the breakdown of common CIS compliance mistakes is worth ten minutes of your time, as is the wider piece on construction accounting for contractors.

Where a professional earns their fee

I’ll be honest about the bias here. The monthly filing, the verifications, the materials-vs-labour splits, the GPS applications — this is repetitive, deadline-driven work where one slip costs real money. It’s the kind of thing that quietly eats a contractor’s weekends.

At Ask Accountants UK Ltd, the day-to-day grind of CIS is bread and butter — from payroll management and CIS returns filing to bookkeeping, tax compliance, and recovering the refunds subcontractors never get round to claiming. If the scheme is costing you sleep, a quick conversation usually sorts it: the team sits at 178 Merton High St, London SW19 1AY, or on 020 8543 1991, and you can always drop them a line directly. Think of it less as a sales pitch and more as “you probably shouldn’t be doing this at 11pm yourself.”

You can also read the official source straight from the horse’s mouth — HMRC’s CIS guide for contractors and subcontractors (CIS 340) and the registration pages on GOV.UK. Fair warning, though: they aim for technical accuracy first and human readability a distant second.

Frequently asked questions

So, in one sentence — how does CIS tax work? A contractor deducts 20% (or 30% if you’re unregistered) from your labour payments and sends it to HMRC as an advance on your Income Tax and National Insurance, which you then reconcile through Self Assessment.

Do subcontractors have to register for CIS? Not legally — but if you don’t, the deduction jumps from 20% to 30%. Registering is free and takes minutes, so there’s no sensible reason to skip it.

Is CIS deducted from the whole invoice? No. Only the labour element. CIS leaves materials, VAT, and operated plant hire alone — which is why itemising your invoices properly genuinely matters.

How does CIS tax work with VAT? Since March 2021, VAT-registered contractors and subcontractors usually apply the domestic reverse charge on qualifying work. The customer accounts for the VAT rather than the supplier. You still work out the CIS deduction on the labour figure separately.

Will I get a CIS refund? Very often, yes. The deductions ignore your business expenses, so most subcontractors overpay across the year. You claim the difference back once you file your Self Assessment return.

What happens if a contractor files a CIS return late? Penalties start at £100 for a single day and escalate to several hundred pounds over the following months — easily topping £1,500 across a year of inaction, plus interest.