There’s a particular kind of dread that settles in when an HMRC letter lands on the doormat. You know the one — brown envelope, official crest, and a first line that never quite says what it means. For a lot of business owners, MTD VAT is exactly that kind of dread: a phrase everyone’s heard, few people fully understand, and almost nobody enjoys thinking about before their morning coffee.

Here’s the short version, because you deserve one before we get into the weeds: MTD VAT — Making Tax Digital for VAT — is HMRC’s requirement that VAT-registered businesses keep their records digitally and file VAT returns through approved software, rather than typing numbers into a box on the old government portal. It’s been mandatory for every VAT-registered business since April 2022, no exceptions based on size or turnover. If you charge VAT, you’re in it, whether you fancy it or not.

That’s the headline. The rest of this guide is everything underneath it — the history, the penalties, the software choices, the mistakes I keep seeing crop up in client conversations, and where MTD VAT sits alongside the newer, noisier cousin arriving this year: MTD for Income Tax. Grab a tea. This one’s worth reading properly.

So What Exactly Is MTD VAT, Anyway?

Making Tax Digital is HMRC’s long-running project to drag the UK tax system out of spreadsheets-and-shoeboxes territory and into something closer to real-time reporting. VAT was the guinea pig. It launched first, back in April 2019, for businesses trading above the VAT threshold, and it’s been the model HMRC has copied for everything since.

Strip away the jargon and MTD VAT asks for two things:

- Digital record-keeping. Your sales and purchase records need to live in compatible software — not a paper ledger, not a standalone Excel file with no digital link to anything else.

- Digital filing. Your VAT return gets submitted straight from that software to HMRC via an API, rather than you copying figures manually into the old online portal.

That’s genuinely it. No new tax, no new rate, no change to what you owe or when you pay it. MTD VAT changes how the information travels, not how much VAT you’re paying. I’ve had clients visibly relax when that clicks — they’d assumed it was some fresh financial burden. It isn’t. It’s a filing method with teeth.

The Slow, Bumpy Road to Mandatory MTD VAT

MTD VAT didn’t arrive overnight, and understanding the timeline actually helps explain why some businesses still get caught out.

| Date | What Changed |

|---|---|

| April 2019 | MTD VAT becomes mandatory for VAT-registered businesses trading above the £85,000 threshold |

| April 2022 | MTD VAT extended to every VAT-registered business, regardless of turnover — sole traders, charities, landlords, the lot |

| November 2022 | Final compliance deadline — this is the point at which “I’ll get round to it” stopped being an option |

| January 2023 | Points-based penalty system introduced for late VAT submissions and payments |

| April 2024 | VAT registration threshold rises to £90,000 |

| April 2026 | MTD for Income Tax launches alongside MTD VAT for sole traders and landlords earning over £50,000 |

Worth sitting with that middle row for a second: since April 2022, there’s been no opt-out based on turnover. A sole trader billing £12,000 a year and a company turning over £4 million follow exactly the same MTD VAT rules. Size doesn’t buy you an exemption — only genuine digital exclusion does, and HMRC applies that sparingly.

Who Actually Has to Bother With MTD VAT?

Short answer: if you’re VAT-registered, you’re following MTD VAT rules. Full stop. That covers:

- Sole traders

- Limited companies

- Partnerships

- Landlords who’ve registered for VAT

- Charities and not-for-profits

- Non-UK businesses registered for UK VAT

The only real get-out is a formal HMRC exemption — usually granted where someone is digitally excluded because of age, disability, remoteness of location, or religious grounds that prevent computer use. Insolvency proceedings can also trigger a temporary exemption. Everyone else? Compatible software, digital records, done through the API. HMRC signs up new VAT registrations automatically now, so there’s no separate MTD sign-up step to forget — though I still meet business owners who assume there is, and spend weeks hunting for a form that no longer exists.

The Nuts and Bolts: What Digital Record-Keeping Under MTD VAT Actually Demands

This is where people either nod along or their eyes glaze over slightly, so let me be concrete. Under MTD VAT, your software needs to hold certain pieces of information digitally: your business name, VAT registration number, and the VAT accounting schemes you use; the time of supply and value of each transaction; and the VAT rate charged. If you use more than one piece of software — say, a spreadsheet for one part of the business and cloud accounting software for another — those systems need a digital link between them. Manually retyping figures from one to the other doesn’t count. Copy-paste, at a stretch, is tolerated. Retyping from memory is not.

Quick warning, and it’s one I give more often than I’d like: an Excel spreadsheet on its own is not MTD-compliant, even if every number in it is perfectly accurate. You need either fully integrated accounting software or “bridging software” that creates that digital link between your spreadsheet and HMRC’s system. Accuracy isn’t the test here. The digital trail is.

Picking Software Without Losing the Will to Live

There’s no shortage of MTD-recognised software on the market, and honestly, the choice overwhelms people more than the actual filing does. Here’s a rough — deliberately rough — comparison of where the main options sit.

| Software | Best for | Price from | Notes |

|---|---|---|---|

| Xero | Small-medium businesses wanting a full package | ~£16/mo | |

| QuickBooks | Sole traders, freelancers | from £14 | Good mobile app |

| Sage | Larger or more established firms | Varies wildly depending on the tier honestly | |

| FreeAgent | Contractors | Free with some business bank accounts | Often bundled — check your bank first |

| Bridging software | People married to their spreadsheet | £5–£10/mo roughly | Cheapest route, but you’re still doing the manual work |

(I’ve left that table a little untidy on purpose — some rows have notes, some don’t, the Sage pricing is genuinely that vague depending which reseller you ask, and that’s closer to how the real comparison feels when you’re actually shopping around at 11pm with seventeen browser tabs open.)

Whichever you land on, it needs to be on HMRC’s recognised software list — check before you commit, because “MTD-friendly” marketing language on a vendor’s website isn’t the same as HMRC recognition.

Miss a Deadline? Here’s What MTD VAT Penalties Look Like Now

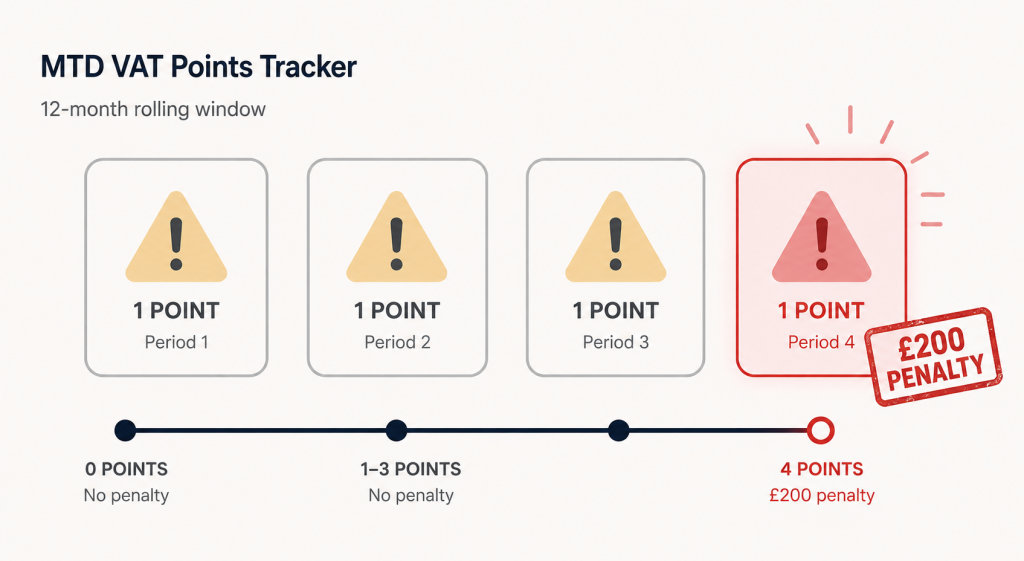

HMRC scrapped the old default surcharge system back in January 2023 and replaced it with a points-based penalty regime. It’s less brutal than it sounds, provided you’re not making a habit of lateness.

Each late VAT return earns you a penalty point. Rack up enough points — four, if you file quarterly — and HMRC issues a £200 fine. Every further late submission while you’re at that threshold costs another £200. Points do eventually expire, generally after 24 months of good behaviour, so it’s not a permanent black mark, but repeated slip-ups get expensive fast.

Late payment is a separate matter, calculated on how overdue the money is:

- Up to 15 days late: No penalty, provided you pay or arrange a Time to Pay plan

- 16–30 days late: 2% penalty on the outstanding VAT

- 31+ days late: 4% penalty, plus daily interest continuing to accrue

I’ll be blunt — that structure genuinely rewards businesses that pick up the phone to HMRC early rather than going quiet and hoping the problem resolves itself. It rarely does.

MTD VAT and Its Newer, Noisier Cousin: MTD for Income Tax

For years, MTD VAT stood alone. That changes from 6 April 2026, when MTD for Income Tax Self Assessment (MTD ITSA) launches for sole traders and landlords with qualifying income above £50,000 — dropping to £30,000 from April 2027, and £20,000 proposed from April 2028.

If that’s you, and you’re also VAT-registered, you’ll be running both systems side by side: MTD VAT for your VAT returns, MTD for Income Tax for quarterly updates on your trading and property income. The good news is that the software overlap is significant — Xero, QuickBooks, Sage and FreeAgent all support both — but you have to authorise each one separately with HMRC. One sign-up doesn’t cover the other. Partnerships and limited companies remain outside MTD for Income Tax for now; HMRC has confirmed it doesn’t currently plan to extend Making Tax Digital to corporation tax at all, favouring a different modernisation approach instead.

Anyone straddling both regimes tends to benefit from a proper review of their cloud accounting setup before April rolls around, rather than discovering the gaps mid-quarter.

Common MTD VAT Mistakes I Still See, Even Now

You’d think seven years in, the teething problems would be gone. They’re not, and a handful crop up again and again:

- Treating a spreadsheet as sufficient without a genuine digital link to filing software.

- Forgetting to authorise software separately for each HMRC service — VAT and Income Tax aren’t linked accounts.

- Copying figures manually between systems, which breaks the digital link requirement even when the numbers are correct.

- Ignoring penalty points because the fine hasn’t landed yet — by the time it does, several late filings have usually stacked up.

- Ignoring deregistration paperwork. If your turnover drops below the £88,000 deregistration threshold, MTD VAT obligations don’t just vanish — you still need to file a final return and formally deregister.

None of these are dramatic failures. They’re small, boring administrative gaps that turn into penalty letters six months later. Good bookkeeping habits close most of them before they open.

Exemptions: The Few Genuine Ways Out of MTD VAT

Exemptions exist, but HMRC doesn’t hand them out casually. You may qualify if:

- You’re digitally excluded — age, disability, location, or religious grounds genuinely prevent online engagement

- You’re subject to an insolvency procedure

- HMRC accepts there’s no reasonable, practical way for you to comply

Applications go through HMRC directly, and you’ll need to explain your circumstances in some detail. Until a decision comes back, you’re not expected to follow MTD VAT rules — but once refused, the clock resumes.

MTD VAT FAQ

Does MTD VAT change how much VAT I owe? No. MTD VAT changes the filing method, not your liability, VAT rate, or payment deadlines.

Do I need to sign up for MTD VAT myself? Generally no — HMRC automatically signs up new VAT registrations. Existing businesses should already be enrolled.

Can I still use a spreadsheet under MTD VAT? Only with bridging software creating a genuine digital link to HMRC’s system. A standalone spreadsheet isn’t compliant on its own.

What happens if I deregister for VAT? Your MTD VAT obligation ends once you’ve filed a final VAT return covering the period up to deregistration.

Is MTD VAT the same as MTD for Income Tax? No — they’re separate systems requiring separate sign-up, though many software packages, including those recommended for cloud accounting clients, support both.

Getting MTD VAT Right, Without the Headache

None of this is designed to be complicated on purpose — HMRC’s stated aim is fewer errors and less last-minute scrambling, and for businesses with tidy digital records, that mostly holds true. The friction tends to show up for people juggling several income streams, switching software mid-year, or trying to sort MTD VAT and MTD for Income Tax at the same time without a clear plan.

That’s genuinely where a second pair of eyes helps. At Ask Accountants UK Ltd, based at 178 Merton High St, London SW19 1AY, we work through VAT compliance, tax compliance more broadly, and cloud accounting migrations with businesses who’d rather not become accidental MTD VAT experts themselves. If you’re unsure whether your current setup genuinely meets the digital link requirement, or you’re bracing for MTD for Income Tax landing on top of MTD VAT this April, it’s worth a conversation before the next filing deadline rather than after a penalty point arrives. Call us on 020 8543 1991, or take a look at our self-assessment and HMRC investigations support if things have already gone slightly sideways.

For the official position, HMRC’s own Making Tax Digital for VAT collection page and VAT registration thresholds guidance are worth bookmarking — rules do shift, and it’s the one place that updates the moment they do.