Nobody sits down on a Tuesday morning and thinks, “Right, today I fancy working through 24 pages of HMRC inheritance tax guidance.” And yet, here you are. Probably because someone you cared about has died, and now there’s a form between you and settling their estate properly.

The IHT 400 Notes — officially titled “How to fill in form IHT400” — is HMRC’s guidance document that runs alongside the main IHT400 return. It’s comprehensive. It’s thorough, and it’s also, if we’re being honest, the kind of document that makes perfectly intelligent people feel suddenly, inexplicably dim.

This guide cuts through the fog. Whether you’re an executor doing this for the first time, a solicitor wanting a plain-English reference, or just someone who found the official HMRC notes about as illuminating as a candle in a hurricane — welcome. Let’s go section by section and work out what’s actually being asked of you.

Why the IHT400 Exists (And Why the Notes Matter More Than You Think)

The IHT400 is the inheritance tax return that must be submitted to HMRC when a deceased person’s estate exceeds the inheritance tax threshold — currently £325,000 for the standard nil-rate band, with additional allowances possible depending on circumstances. (If you’re unsure where your estate sits, the inheritance tax threshold guide is worth reading before you touch this form.)

The form itself is one thing. But the IHT 400 Notes are what make the form navigable. They tell you why each box exists, what counts as a valid answer, and — crucially — where estates commonly make mistakes that delay probate or trigger HMRC enquiries.

Getting the IHT400 wrong doesn’t just mean paperwork corrections. It can mean delayed probate, interest on unpaid tax, or in serious cases, penalty charges. The notes are your operating manual. Read them. Or — read this, which is arguably more digestible.

Sections 1–3: Who Died, Who’s Responsible, and What You’re Declaring

The opening sections of the IHT400 (and corresponding parts of the IHT 400 Notes) deal with basic identification and executor responsibilities. Sounds straightforward. Mostly it is — but a few things trip people up.

The deceased’s domicile matters enormously. If the person who died was domiciled outside the UK, the rules shift in ways that affect how much of the estate is even subject to UK inheritance tax. The IHT 400 Notes walk through domicile carefully, because HMRC has seen enough cases where executors assumed UK residency meant UK domicile and got it wrong.

Executors (or administrators if there’s no will) sign the declaration confirming the information is accurate. This isn’t ceremonial. Deliberately providing false information on an IHT400 carries serious legal consequences. The notes make this explicit — and it’s the right thing to flag.

The Estate Valuation Pages: Where Most Headaches Live

Sections covering the estate’s assets are where the IHT 400 Notes become genuinely indispensable. This is the meat of the form.

Property. Residential property must be valued at the open market value at the date of death. Not what the estate agent thinks it might fetch in a buoyant market. Not what it was worth when the deceased bought it in 1987. The date-of-death value — ideally supported by a RICS-qualified surveyor’s report.

Bank accounts and savings. Include the balance at the date of death, including any accrued interest not yet credited. The IHT 400 Notes specify that you need to include all accounts — even dormant ones, even small ones.

Stocks and shares. Valued using the “quarter-up” rule: take the difference between the lower and higher price on the date of death, divide by four, and add to the lower price. It sounds arcane because it is arcane. The notes explain this, though not with the warmth and enthusiasm you’d hope for.

Household contents and personal belongings. People almost always undervalue these. HMRC knows people undervalue these. The IHT 400 Notes suggest using auction house estimates or professional valuations where the estate contains items of value — jewellery, art, antiques, wine collections. “Assorted furniture: £500” on a form covering a five-bedroom house tends to raise eyebrows.

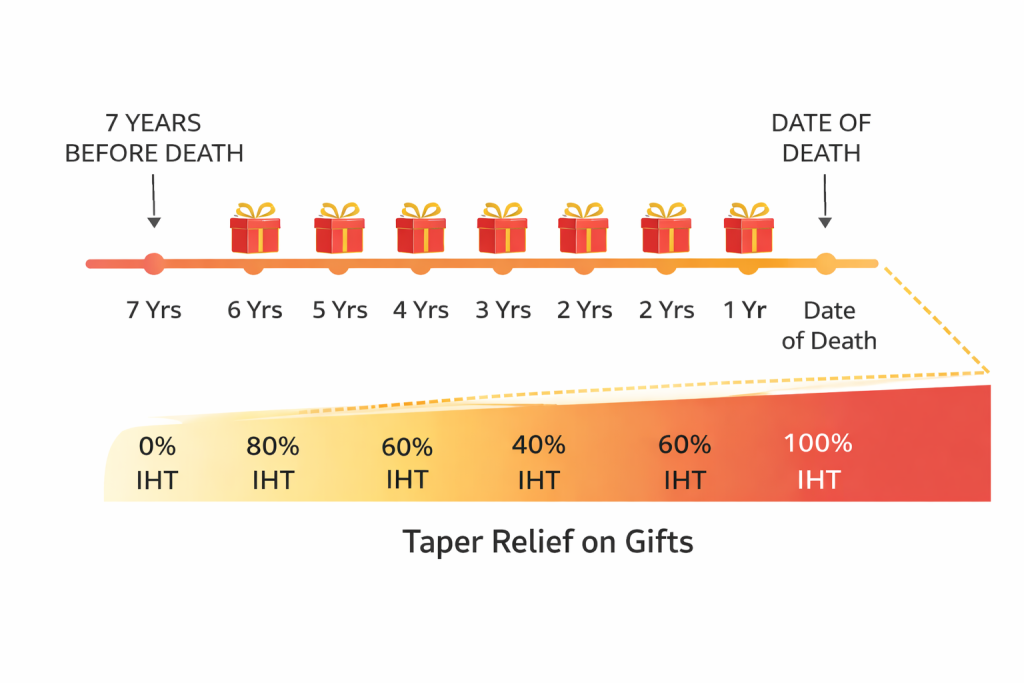

Gifts, Transfers, and the Seven-Year Shadow

One of the most technically complex parts of the IHT 400 Notes relates to lifetime gifts. If the deceased made gifts within seven years of their death, those gifts may be included in the estate for inheritance tax purposes — this is the infamous seven-year rule.

The notes require executors to investigate and disclose:

- Cash gifts to individuals

- Assets transferred at undervalue

- Contributions to trusts

- Regular gifts out of income (which can be exempt if properly documented)

The IHT 400 Notes give detailed guidance on what qualifies as a “normal expenditure out of income” exemption — one of the most powerful but frequently misused reliefs. HMRC wants evidence that the gifts were habitual, made from income (not capital), and didn’t reduce the donor’s standard of living. Establishing this retrospectively is… not easy.

If you’re dealing with an estate where significant gifts were made, this section alone may warrant professional input. The team at Ask Accountant handles exactly these kinds of inheritance tax complexities — it’s the sort of thing where getting it right first time genuinely matters.

For a deeper look at how gifts interact with inheritance tax, the inheritance tax gifts rules guide covers this in practical terms.

Reliefs and Exemptions: The Sections That Can Save Thousands

This is where careful reading of the IHT 400 Notes pays dividends.

Spouse or civil partner exemption. Assets passing to a surviving spouse or civil partner are generally exempt from inheritance tax — unlimited. The form requires this to be declared explicitly, not assumed.

Charity exemption. Gifts to qualifying charities are exempt. If 10% or more of the net estate passes to charity, the remaining estate may qualify for a reduced 36% IHT rate (rather than 40%). The IHT 400 Notes explain how to calculate whether this threshold is met — it’s not always obvious.

Business Property Relief (BPR) and Agricultural Property Relief (APR). These reliefs can be substantial — potentially 50% or 100% reduction on qualifying assets. The IHT 400 Notes devote considerable space to what qualifies, what doesn’t, and how to evidence the claim. A business that’s been trading for less than two years, for example, won’t qualify. Neither will a business that’s investment-heavy rather than trading-focused.

Getting BPR wrong — either overclaiming or failing to claim where it’s legitimately available — is a common and costly error. If the estate includes business interests, read this section more than once.

The Supplementary Forms: IHT400’s Extended Family

Here’s something the IHT 400 Notes explain but that catches many executors off guard: the IHT400 is not a standalone document. It has a suite of supplementary schedules, each covering a specific type of asset or relief.

| Schedule | What It Covers | When You Need It |

|---|---|---|

| IHT401 | Domicile outside the UK | Deceased not domiciled in the UK |

| IHT402 | Claim to transfer unused nil-rate band | Surviving spouse/civil partner claiming unused NRB from deceased spouse |

| IHT403 | Gifts and other transfers of value | Gifts made in last 7 years (or trusts) |

| IHT404 | Jointly owned assets | Property or accounts held jointly |

| IHT405 | Houses, land, buildings | Deceased owned property |

| IHT406 | Bank and building society accounts | Financial accounts held in sole name |

| IHT407 | Household and personal goods | Contents of home, vehicles, valuables |

| IHT408 | Household and personal goods donated to charity | Contents given to charity rather than sold |

| IHT409 | Pensions | Deceased had pension(s) |

| IHT410 | Life assurance and annuities | Life insurance policies in existence |

| IHT411 | Listed stocks and shares | Shares quoted on stock exchange |

| IHT412 | Unlisted stocks, shares and investments | Shares in private companies |

| IHT413 | Business and partnership interests | Business Property Relief claims |

| IHT416 | Debts owed to the estate | Money owed to deceased |

| IHT418 | Assets held in trust | Deceased had benefit of a trust |

| IHT421 | Probate summary | Always — sent to Probate Registry |

The IHT 400 Notes explain which schedules apply based on your estate’s composition. Not every estate needs all of them — but most estates need more than one. Forgetting a schedule is one of the most common reasons HMRC returns submissions for correction, adding weeks (sometimes months) to the probate timeline.

The Residence Nil-Rate Band: An Extra Allowance That Many Miss

Introduced in 2017 and still frequently overlooked, the Residence Nil-Rate Band (RNRB) allows an additional allowance — up to £175,000 — when a residence passes to direct descendants. Combined with the standard nil-rate band, a married couple could potentially pass up to £1 million to their children free of inheritance tax.

The IHT 400 Notes cover the RNRB in detail, including the tapered withdrawal that applies to estates worth more than £2 million. It tapers away at £1 for every £2 above the threshold — so for a £2.35 million estate, the full RNRB is gone.

To claim it, you need to complete the IHT435 form. The notes explain what qualifies as a “residence” (broadly, a property the deceased lived in at some point), what counts as a “direct descendant” (children, grandchildren, stepchildren, adopted children — but notably not nieces or nephews), and what happens if the property was downsized or sold before death.

This is an area where IHT tax planning done during the deceased’s lifetime can make the biggest difference. After death, the options narrow considerably.

Debts and Liabilities: Reducing the Taxable Estate

The IHT400 and accompanying notes include sections for deducting liabilities from the estate value. Mortgages, credit card balances, loans, and outstanding bills at the date of death can all reduce the taxable estate.

A few things the IHT 400 Notes are firm about:

- The debt must have been legally enforceable at the date of death.

- Loans from family members can only be deducted if there’s genuine evidence of the arrangement — an IOU written on a napkin is not going to cut it.

- Debts that were later written off or forgiven can’t simply be included to reduce the estate artificially.

Funeral expenses are also deductible — reasonable ones. The notes don’t put a figure on “reasonable,” but HMRC has been known to query very extravagant arrangements.

Calculating the Tax: What the Summary Sections Are Doing

The final sections of the IHT400 bring together all the estate values, deduct liabilities and reliefs, apply the nil-rate band (and RNRB if applicable), and calculate the tax due.

The IHT 400 Notes walk through this arithmetic carefully. One thing that catches people: tax is due on the amount above the nil-rate band, at 40%. So an estate of £500,000 with a single nil-rate band of £325,000 attracts tax on £175,000 — which is £70,000.

If an unused nil-rate band from a deceased spouse is being claimed (via form IHT402), the available threshold could be up to £650,000. Claiming this can make the difference between a substantial tax bill and none at all.

| Scenario | Estate Value | Available NRB | Taxable Amount | IHT Due (40%) |

|---|---|---|---|---|

| Single, no spouse | £500,000 | £325,000 | £175,000 | £70,000 |

| Married (spouse NRB transferred) | £700,000 | £650,000 | £50,000 | £20,000 |

| Married + RNRB (property to children) | £950,000 | £1,000,000 | £0 | £0 |

| High-value estate (no reliefs) | £1,500,000 | £325,000 | £1,175,000 | £470,000 |

Note: figures above use 2024/25 nil-rate band of £325,000 and RNRB of £175,000 per person. Always verify current figures with HMRC or a qualified adviser.

Payment and the “When Is IHT Due?” Question

The IHT 400 Notes are clear on this, even if it’s a fact that causes genuine distress for many families: inheritance tax is due six months after the end of the month of death. Not after probate. Not after the estate is wound up. Six months from death.

This creates a practical problem. Probate hasn’t been granted yet, so the estate’s assets can’t be legally accessed. But the tax still needs paying. How do families manage it?

Options include:

- Direct payment from the deceased’s bank account (banks will often facilitate this before probate for tax purposes)

- Payment by instalments on certain assets like property and business interests

- Borrowing (some families take short-term loans to cover the liability)

The instalment option is particularly relevant when the estate includes illiquid assets — property that can’t be sold quickly. The IHT 400 Notes explain which assets qualify for payment by instalments and how interest accrues on unpaid tax.

Common Mistakes the IHT 400 Notes Are Quietly Warning You About

Reading between the lines of the notes, certain warnings recur:

Undervalued assets. HMRC has its own valuation resources and cross-references estate values against market data. Suspiciously low property valuations attract scrutiny. Get proper professional valuations.

Missing supplementary forms. Submitting the IHT400 without required schedules sends it straight back. Check the list. Check it again.

Incorrectly calculated nil-rate band. Particularly when transferring from a deceased spouse, the calculation can go wrong — especially if the first spouse to die made chargeable transfers themselves.

Failing to disclose gifts. Executors sometimes don’t know about gifts the deceased made. The notes advise checking bank statements, asking family members, and documenting the investigation process. HMRC can and does compare information from multiple sources.

Trust assets not included. If the deceased had a benefit from a trust — receiving income from it, for example — that interest may need to be included in the estate. This is one of the more technically involved areas of the notes.

💡 Worth knowing: The IHT400 must be submitted to HMRC before you can apply for the Grant of Probate. HMRC will issue a receipt or “IHT421” clearance that the Probate Registry requires. The timeline matters — delays in submitting can delay everything downstream. More on this at Do I need to complete IHT400 before applying for probate?

Can You Submit the IHT400 Online?

As of 2025, the IHT400 cannot be submitted fully online. It must be printed, signed, and posted to HMRC’s Inheritance Tax unit in Nottingham. The supplementary schedules go with it. This surprises people in an era when almost everything tax-related has gone digital.

HMRC has been developing digital options, but the paper process remains current practice. The full picture on this is at Can you submit IHT400 online?

When to Stop Reading Guidance and Start Talking to Someone

The IHT 400 Notes are excellent — thorough, considered, and genuinely helpful. But they’re written for a general audience, which means they handle the common scenarios well and the complex ones… less so.

Estates involving trusts, business interests, agricultural land, overseas assets, significant gift histories, or recent changes in domicile often need professional guidance that goes beyond what the notes can provide. Getting it wrong costs time, money, and sometimes more tax than necessary.

The team at Ask Accountant (based at 178 Merton High St, London SW19 1AY) works with executors and families navigating inheritance tax returns — from straightforward estates to those with layers of complexity. Their inheritance tax advisory work covers not just completing the IHT400 correctly, but making sure every legitimate relief and exemption has been identified. If you’d rather have a conversation than spend another hour in the HMRC notes, call them on +44(0)20 8543 1991.

Frequently Asked Questions About the IHT 400 Notes

What are the IHT 400 Notes? The IHT 400 Notes are HMRC’s official guidance document for completing the IHT400 inheritance tax return. They explain each section of the form, define what must be included, and clarify how to apply reliefs and exemptions correctly.

Do I need to read the IHT 400 Notes before completing the form? Yes — genuinely. The IHT400 form alone doesn’t explain the context behind many of its questions. The notes are where you find out what HMRC actually expects, what evidence is required, and what common errors to avoid.

How long do the IHT 400 Notes take to work through? The guidance runs to around 50 pages in its current version. For a straightforward estate, a careful reading takes a few hours. For complex estates with multiple asset types and reliefs, factor in considerably longer — plus time to gather the evidence and valuations the form requires.

Where can I get the IHT 400 Notes? They’re available as a PDF download directly from the HMRC website. Always download the current version, as guidance is updated periodically.

What happens if I make a mistake on the IHT400? Errors can be corrected, but the process varies depending on whether the mistake is discovered before or after HMRC has processed the return. Post-submission corrections require a formal amendment.

Can a lay executor complete the IHT400 without professional help? For simple estates with straightforward assets, yes — provided the executor reads the IHT 400 Notes carefully and follows them conscientiously. For anything involving trusts, businesses, significant gifts, or overseas assets, professional guidance is strongly advisable.

Is the IHT 400 different from the IHT205? The IHT205 (now replaced by the IHT Estate Report for deaths from January 2022) was a shorter form for smaller, simpler estates below certain thresholds.