Somewhere between “I’ll sort the tax stuff later” and an unexpected brown envelope from HMRC, thousands of UK company directors learn the same lesson: director tax doesn’t wait for you to feel ready. It just arrives — quarterly, annually, sometimes without warning — and it expects you to deal with it properly.

If you’ve recently become a director, or you’ve been one for years but keep a slightly uneasy relationship with your obligations (no judgement — most of us do), this is for you. Director tax sits at an odd crossroads. You’re taxed partly like an employee, partly like a shareholder, and partly like someone running a small state-within-a-state called a limited company. Get the balance wrong and HMRC notices. Get it right and you’ll genuinely pay less than you think, legally, every single year.

Firms like Ask Accountants UK Ltd, based on Merton High Street in south-west London, spend a good chunk of their working lives untangling exactly this — director tax queries, HMRC letters, the lot. So rather than another generic checklist, let’s actually work through how director tax functions in practice, where people slip up, and what “compliant” really looks like day to day.

What Counts as Director Tax, Anyway?

Here’s the thing nobody explains clearly enough: there’s no single tax called “director tax.” It’s a bundle. A director’s income can come from several channels at once, and HMRC taxes each one differently.

- Salary through PAYE, like any employee

- Dividends, which sit in a separate, usually more favourable tax bracket

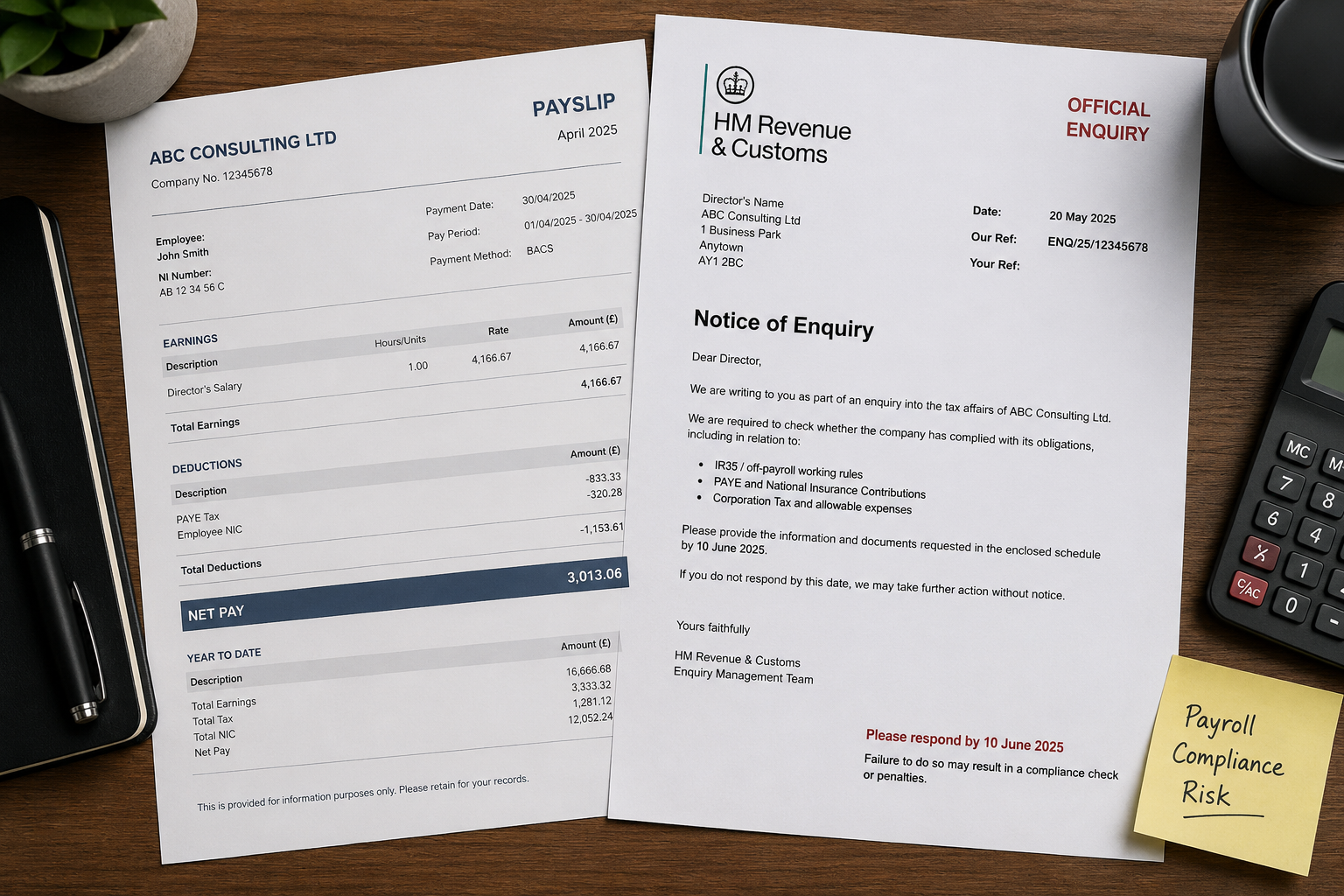

- Benefits in kind (company car, private medical, that gym membership you expensed) — you report these via a P11D

- Directors’ loans, which HMRC watches closely if they go unpaid

- Pension contributions, which can shrink your taxable profits if you structure them well

Miss any one of these categories in your planning and you end up either overpaying (common) or underreporting (risky). Director tax compliance really just means reporting every one of these strands correctly, on time, to the right HMRC department.

Why Directors Get Caught Out More Than Employees

An employer automatically deducts an ordinary employee’s tax, and the employee rarely thinks about it again. Directors don’t get that luxury. You’re both the person earning the money and, in a sense, the person who has to make sure HMRC taxes it properly — because you often control the company that pays you.

That dual role is precisely where director tax problems tend to start. A friendly-sounding director’s loan that you never quite get around to repaying. Declaring dividends without the paperwork to back them up (illegal dividends are a real, and surprisingly common, mess). Or simply forgetting that once you cross certain income thresholds, your personal allowance quietly shrinks.

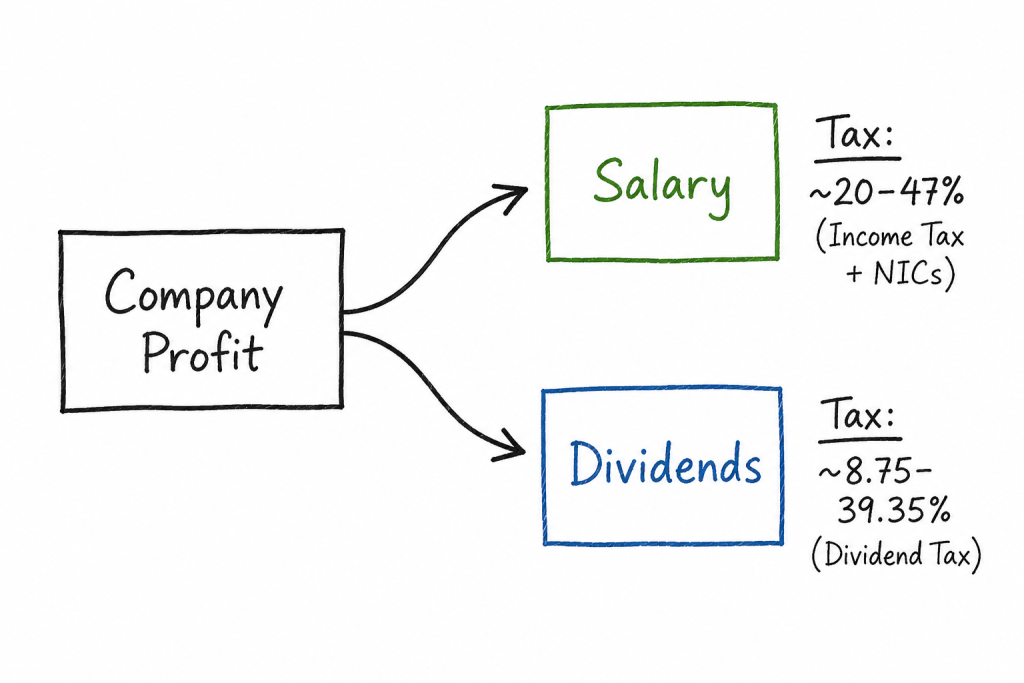

Salary vs Dividends: The Decision Most Directors Get Half-Right

This is the classic one. Most owner-directors pay themselves a modest salary — often set near the National Insurance threshold — and take the rest as dividends. Why? Because dividends aren’t subject to National Insurance, and the tax rates on dividend income sit below equivalent salary rates.

It sounds simple. It isn’t quite. Get the split wrong and you can trigger:

- Unnecessary National Insurance contributions

- Loss of statutory benefits (maternity pay, certain pension credits) tied to salary level

- Dividend tax bills that arrive at self-assessment time and catch people off guard

| Income Type | Taxed Via | Subject to NI? | Typical Director Approach |

|---|---|---|---|

| Salary (PAYE) | Payroll | Yes, above threshold | Set near NI/personal allowance threshold |

| Dividends | Self-assessment | No | Top up income after salary, within profit limits |

| Benefits in kind | P11D | Class 1A NI (employer) | Often overlooked, reported annually |

| Director’s loan | Company tax return (S455) | No (but can attract S455 charge) | Repay within 9 months of year-end where possible |

There’s no universal “correct” split — it depends on your company’s profits, your personal circumstances, and what you’re trying to achieve (maximising take-home pay isn’t always the only goal; pension planning and mortgage applications matter too). This is genuinely one of the areas where sitting down with someone offering personal tax planning advice pays for itself several times over.

The Directors’ Loan Account Nobody Reads the Small Print On

Directors’ loan accounts (DLAs) deserve their own bruised paragraph. In principle, borrowing from your own company sounds harmless — it’s your company, after all. In practice, HMRC enforces fairly rigid rules here, and it regularly catches directors out.

If you don’t repay a loan within nine months of the company’s year-end, the company faces a Section 455 tax charge — currently 33.75% of the outstanding balance — until you repay it. There’s also the “bed and breakfasting” rule, designed specifically to stop directors repaying a loan just before year-end and re-borrowing it days later. HMRC has seen that trick before. Many times.

Quick reality check: if your director’s loan account regularly sits overdrawn for months at a time, that’s not a cash-flow quirk — HMRC treats it as a pattern worth investigating.

National Insurance, Dividends, and the Bits That Change Every Year

One frustrating truth about director tax: the numbers move annually. Dividend allowances have shrunk considerably over the past few years, personal allowances taper away above £100,000, and the Chancellor adjusts NI thresholds in the Budget more often than most directors would like. Relying on last year’s figures is a quietly common way to file an incorrect return.

Directors earning above £100,000 also lose £1 of personal allowance for every £2 earned over that threshold — creating an effective marginal tax rate north of 60% in that band. It surprises almost everyone the first time they see it on paper.

Corporation Tax and Director Tax Aren’t the Same Conversation (But They’re Related)

It’s worth separating two things that people constantly mix up: corporation tax is what the company pays on its profits; director tax is what you personally pay on what you extract from the company. They interact — you can only legally pay dividends from post-tax profits, for instance — but you report and calculate them completely separately, on the company tax return and your self-assessment return respectively.

Confusing the two is one of the more common (and forgivable) errors new directors make. It’s also why a decent bookkeeping service matters more for directors than for most sole traders — you need to track the two tax positions in parallel, not bolt them together at year-end in a panic.

When HMRC Comes Knocking

Director tax attracts a disproportionate amount of HMRC attention, partly because directors have more discretion over how they extract income, and partly because errors here tend to run larger in value than a typical PAYE mistake. If you’re navigating one currently, it’s worth understanding what actually happens during a tax investigation before assuming the worst — the process follows a fairly defined shape, and knowing the stages helps enormously.

Directors under enquiry often benefit from reviewing the general tax investigation process early, and from getting proper tax investigation support rather than responding to HMRC letters alone. It’s one of those situations where writing a first response under stress at 11pm can shape how the whole enquiry unfolds.

A Rough (Deliberately Imperfect) Compliance Timeline

Not every director’s calendar looks identical — company year-ends vary — but most obligations cluster around a few predictable points.

| Obligation | Roughly When | Notes | |—|—| | Self-assessment payment on account | 31 January & 31 July | Based on prior year’s tax bill | | Self-assessment return deadline | 31 January (online) | | | P11D submission | 6 July following tax year | For benefits in kind | | Corporation tax payment | 9 months + 1 day after year-end | Company, not personal | | Confirmation statement | Annually, Companies House | Not a tax filing but easy to forget alongside it | | Dividend paperwork | Each time declared | Board minutes + voucher |

Practical Habits That Keep Directors Out of Trouble

A handful of habits separate directors who sail through their tax affairs from those who dread every January:

- Keep dividend paperwork current. A board minute and dividend voucher for every declaration, even in a one-person company. HMRC has successfully reclassified undocumented “dividends” as salary before.

- Reconcile the director’s loan account monthly, not once a year in a panic.

- Separate personal and business banking completely. Obvious, yet still the single most common source of confusion during any HMRC review.

- Review your salary/dividend split annually — thresholds shift, and last year’s optimal split may not be this year’s.

- Use cloud accounting software so your figures are current rather than reconstructed from memory in December.

Ask Accountants UK Ltd handles a fair amount of this day-to-day — accounts and tax, cloud accounting, company secretarial filings, that sort of groundwork — precisely because directors rarely have the spare hours to track every threshold change themselves. It’s not really about outsourcing anxiety; it’s about not having six spreadsheets open at 11pm before a deadline.

Frequently Asked Questions About Director Tax

Do I pay tax differently as a director compared to a regular employee? Yes. HMRC taxes your salary via PAYE just like an employee’s, but directors often also receive dividends, benefits in kind, and sometimes loans — each under different rules.

What happens if I don’t repay a director’s loan in time? The company becomes liable for a Section 455 charge (33.75% of the outstanding balance) until you repay it, and you must disclose the amount on the company tax return.

Is it better to take a salary or dividends as a director? It depends on your company’s profits and personal circumstances, but most owner-directors use a modest salary plus dividends to reduce overall National Insurance exposure. There’s no single right answer for everyone.

Can HMRC investigate director tax specifically? Yes — HMRC investigates directors more frequently than average PAYE employees, because of the discretion directors have over how they extract income from the company.

Do I need an accountant for director tax, or can I manage it myself? It’s legally possible to manage it yourself, but given how many moving parts director tax involves — PAYE, dividends, P11Ds, loan accounts, corporation tax interaction — most directors find professional tax compliance support pays for itself in avoided errors alone.

If any of this feels closer to your situation than you’d like — an overdrawn loan account, dividends you never quite paperworked properly, or a nagging feeling nobody’s reviewed your salary/dividend split in years — it’s worth getting someone to look at it before HMRC does. Call Ask Accountants UK Ltd on 020 8543 1991, or visit them at 178 Merton High St, London SW19 1AY, for a proper look at your director tax position rather than a guess dressed up as one.